Over the last 15 years working with startups and entrepreneurs, I have finally figured out where I can add the most value and have the most fun as well.

I call that the “napkin stage” of the startup.

Napkin Stage Startup

There are 3 most important reasons why I love the stage:

1. There are no bad ideas and no bad markets. They are all based on experiences and personal opinions. Which means I learn a lot of new things. I love learning about markets, sales growth and building scalable marketing channels, but after a while it gets to be more of the same.

2. If the idea is simple enough that you can express it on a napkin, instead of using a PowerPoint slide or need a complete prototype for someone to get it, then I get excited about the possibilities.

3. Entrepreneurs are most excited when they dont have to deal with hiring problems, marketing challenges, customer churn, etc. So, I get to work with them when there’s sunshine and roses all around. They have nothing but optimism at this stage.

There are challenges as well.

1. 90% of the ideas never “take off”. The market is too small, the customers dont need the product or the value is very limited.

2. The idea maze leads to a lot of churn, and many back of the napkin ideas really are a big waste of time.

3. Teams pivot constantly, are never settled and sometimes will change their mind to pursue a “job” if the idea is not appealing enough

I believe there are 5 most important things I bring to the table at this stage:

1. Customer development and validation. Getting early customer validation by talking to 10+ people and understanding the “real problem” excites me a lot. I have a decent enough network to ensure that I can call on 10 folks and get to understand any market in technology enough to understand if there are opportunities.

2. Market research and knowledge. Understanding, analyzing and projecting market needs is something I have enough experience with, and have done it for long that I really enjoy both the top-down and bottom’s up analysis of the markets and segmenting the customers.

3. Helping build your team, or finding a cofounder. Over the last 15 years, I have helped 19 startup founders find early (#1 or #2) employees, and about 11 founders find their cofounder. I love putting people together who I think might work well together and complement each other’s skills.

4. Build an early prototype, mockups or alpha version of the product. That’s the true use of the napkin these days anyway. I enjoy this the most. Reducing complexity and figuring out “Enough” to get by for a MVP is the most enjoyable experience in my mind.

5. Coaching the entrepreneur on structure of the company, financing landscape and whether they need to raise VC funding or make it a lifestyle business instead (which I actually have no problem with at all).

So, I am thinking about how I can help, add value and enjoy the ride with the “earliest” of early stages of a company – The Napkin Stage.

Over the last 10 years there has been a dramatic growth in accelerators. While incubators such as ideaLab (Bill Gross, Los Angeles, 1990’s) had existed during the previous bubble, the absolute number of new age accelerators has gone from zero to over 300 in the US alone and from 0 to over 1000 worldwide. At the same time while, the number of early stage (less than $2 Million and company < 2 years old) deals have gone up significantly as well.

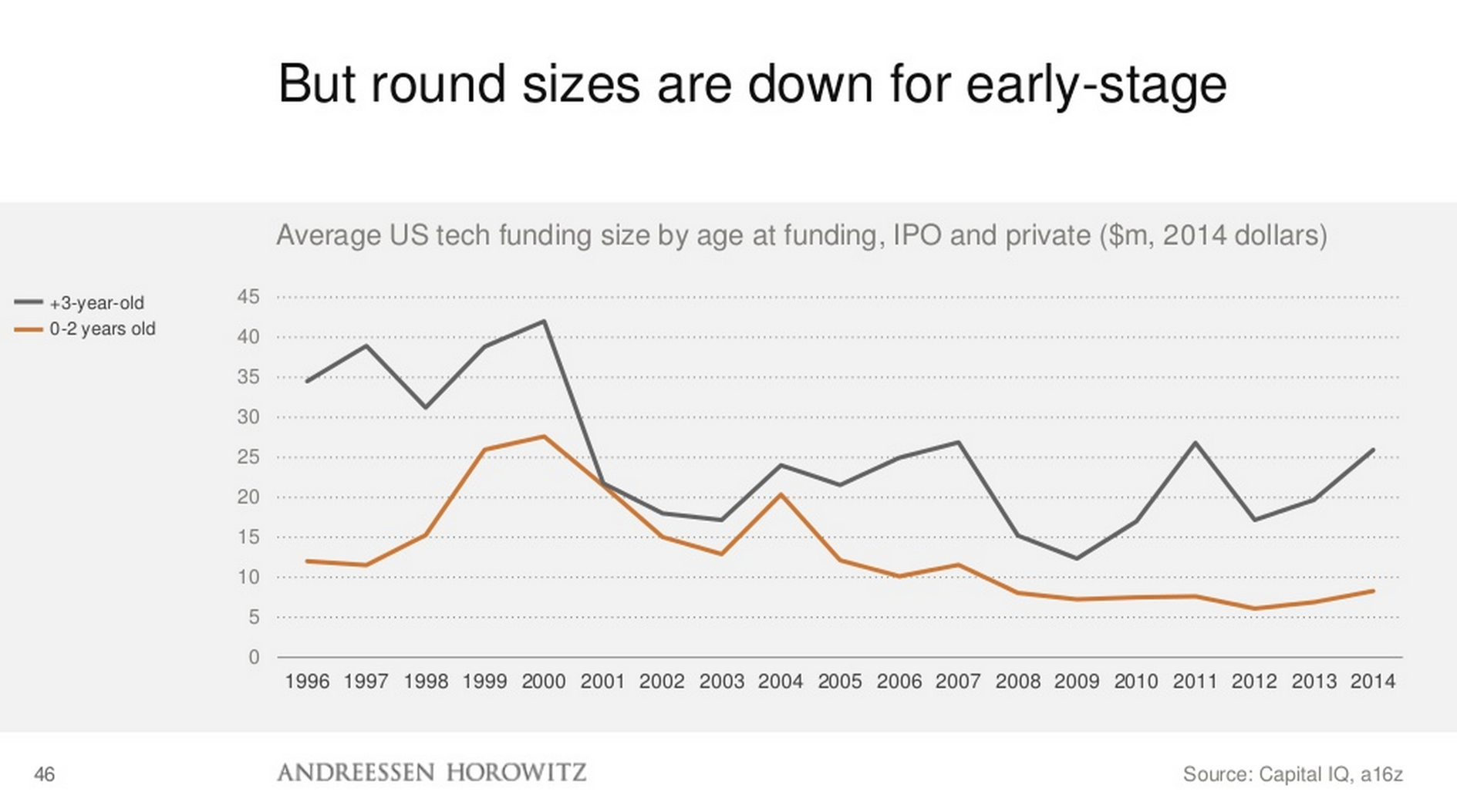

Growth in Seed Round Financing

The chart above from Benedict Evans shows the growth in seed rounds, which indicates that the number of early rounds have increased relative to $3-6 Million rounds.

At the same time, the average amount of money invested in early stage rounds is going down. That makes sense since it is cheaper to build an early stage company and “try to find a product market fit”

Size of Early Stage Rounds

There are 2 charts missing from this deck. First, how many of these early stage deals are going through accelerators and what is the size of the deal for companies going through accelerators versus those that are not.

Fortunately, thanks to folks like CB Insights and Mattermark, we do have access to that data. I will upload the charts in a few hours / tomorrow since I am running late to my meeting this morning.

1. Accelerator funded companies make up 13% of the total number of seed funded companies, and have been steadily rising. Obviously from zero in 2005 to 13% of total seed funded deals in 2015.

2. Accelerator funded companies raise 20% more in the seed round than non-accelerator companies.

Finally anecdotal data from Microsoft accelerator companies over the last few years alone, I can infer that accelerator companies have 25% better survival rate than those that did not go to an accelerator after the first 2 years.

How did we get this information?

We got over 250 applicants in the first cohort (Sep 2012), 450+ in the second (Mar 2013), over 600 in the third (Aug 2013) and over 1000 in the fourth (Feb 2014) in India alone. Of these, we picked 10 in the first, 12 in the second, 13 and 15 in the third and fourth cohorts.

We then tracked the remaining companies. Of them 5, 3, 11 and 13 got into other accelerator programs such as GSF, Tlabs and Kyron.

Of the remaining startups, 31%, 14%, 22% and 12% have shutdown. That compares to 20%, 10%, 22% and 0% so far.

So, if you are part of an accelerator program, you are likely to get more money, survive for longer and likely to get funding versus not.

Those are the biggest reasons to join an accelerator.

There are many assumptions we make about the product or the customer problem, which makes us develop solutions that may be really more complicated than required.

A friend and fellow entrepreneur I met on Friday was showing me a prototype (HML mock up with transitions, with some simple functions implemented) of this SaaS application. He had used a developer on hire at UpWork to develop the initial version. After speaking to and confirming the mockup (wireframes) with 10 different users he was off to develop and deliver the MVP. Overall he had spent about $8000 in design and development and had taken about 13 weeks to develop the MVP. Most of the time was spent back and forth with the design team for the HTML / CSS and the development team for confirming features and transitions.

Cognitive Biases Field Guide

Of the 13 weeks, his development team spent 2 weeks just implementing a sign up process, a user cancellation process, a payment process, a refund process, a login process, a password retrieval process, etc. Which he did not realize was the tax of developing a SaaS solution. Instead he took the 5 step approach to building a SaaS application and followed it religiously.

The critical mistake during customer development that most entrepreneurs make is to lead with the solution or product instead of spending time learning about the current solutions.

When he was showing it to potential customers, he found that most of them liked the product and said they’d use it and pay for it, if they could find value in 2-3 weeks. He was pretty happy given that most users were ready to pay for the product, which he did believe would solve a critical problem for them.

After developing the MVP and letting his users know about the product, he followed up by asking them to start to use the application. The first two days were great, with lots of feedback and improvements that they gave him about the product.

Then for the next 3 days there was radio silence. Even after his prodding and cajoling, most users were not using the application.

Instead of talking to users face to face, he instead decided to spend time with them (3 hours each user), shadowing them to understand why they were not using the application.

Turns out most of the users needed his product, but either A) did not remember it existed or B) were used to using their workaround – largely using a combination of email and cut and paste into Slack.

The biggest barrier to his adoption and usage was their existing process (although inefficient) was something they were used to and so were able to “optimize” it to make it quick and “fast” for their own usage. So much that they felt that using his product (which I can assure you would be vastly superior) would slow them down.

He then pivoted his product (not idea) to implement the one feature they all wanted as a Chrome plugin. Which worked like a charm.

He then had to remove the top 3 features and undo all the user login and management, infrastructure code and other remaining features, just to support the user behavior for their existing process.

The big takeaway for him was that when you have a hammer, everything seems like a nail.

The biggest takeaway for his wife (who is his cofounder) was not over engineer the solution.

The big takeaway for me was the failed customer development process. With all our biases (which all of us have) – we always tend to lead with the solution (“let me show you a demo”), instead of understanding the problem better to focus on delivering the one feature that matters, without all the bells and whistles.

This post is for non developer founders who want to build a SaaS application.

Software as a Service (SaaS) is a relatively small market – at $19 Billion in total revenues, it seems large, but compared to $250 Billion of the overall software market it seems minuscule. It has grown from nothing to this large number in the last 10 years. Similar to the eCommerce market, which seems large but is less than 15% of overall retail, the opportunities will start to be in the niches is my prediction.

The big question is when and how will it grow and where are the opportunities. While there are many specialist firms focusing on SaaS alone, the incumbent software companies (the largest of who are Microsoft, SAP, Oracle, etc.) are also making their own investments to move their businesses from selling licensed software to services.

One of the key opportunities I see is that ability for smaller, niche markets to be targeted using SaaS. Since the deployment model, time to value and cost are so much lower now than 10 years ago, it is easy to build a niche product that can gain rapid fan following among the target customers and *if that customer base* does grow and end up having more budget it can be a lucrative market.

I do get the question often about the steps to build a SaaS business. Even if you dont intend to build a Venture funded business, the economics of SaaS are determined by cost of customer acquisition (CAC) and cost of servicing the customer (developing, operating and maintaining the software).

What I am increasingly starting to see is that most prototypes are either built by a developer founder, or outsourced (by a non technical founder) to “prove that the market exists“.

1. The first step I’d recommend before you start development, is to sign up 15-20 beta customers. Target people you know well who will stick through your crappy alpha, beta and version 1, so you can convince them that the value does exist when you iterate quickly.

For early beta customers, there are many techniques you can use including: a) setting up a launch page and promoting that launch page on social media b) setting up a launch page and buying Google adwords to drive signups and following up with signups via email c) blogging about the topic to share what you know about that market d) interviewing influential users before you launch or e) setup an email newsletter of great content for that industry and have many potential users subscribe to that newsletter.

2. The next step is to create an activity model and user flows.

User flow Diagram

This step is to ensure that you can know exactly what are the top 3 features you need to implement first which will make your product “must have” to solve the problem for your users.

In fact if you can identify the top feature (just one) that people will come back and use everyday, you should be good to go to the next step. Validate the top feature with your beta customer list, so you are building what they will use.

3. The next step is to create a mockup using wireframes. These are typically good to show the screens your user will go through and the experience as well. I would get a lot of feedback on the list of steps and screens before I build the prototype.

Iphone Wireframe

Typically in your first pass stick to under 7 screens would be my suggestion. That’s enough for a 45 second to 1 min “demo” and should give your users a feel for what the app will do. If they ask you for “one” feature that matters more to them than the ones you have, dont mock it up yet, but put it on your list until you have enough users interested.

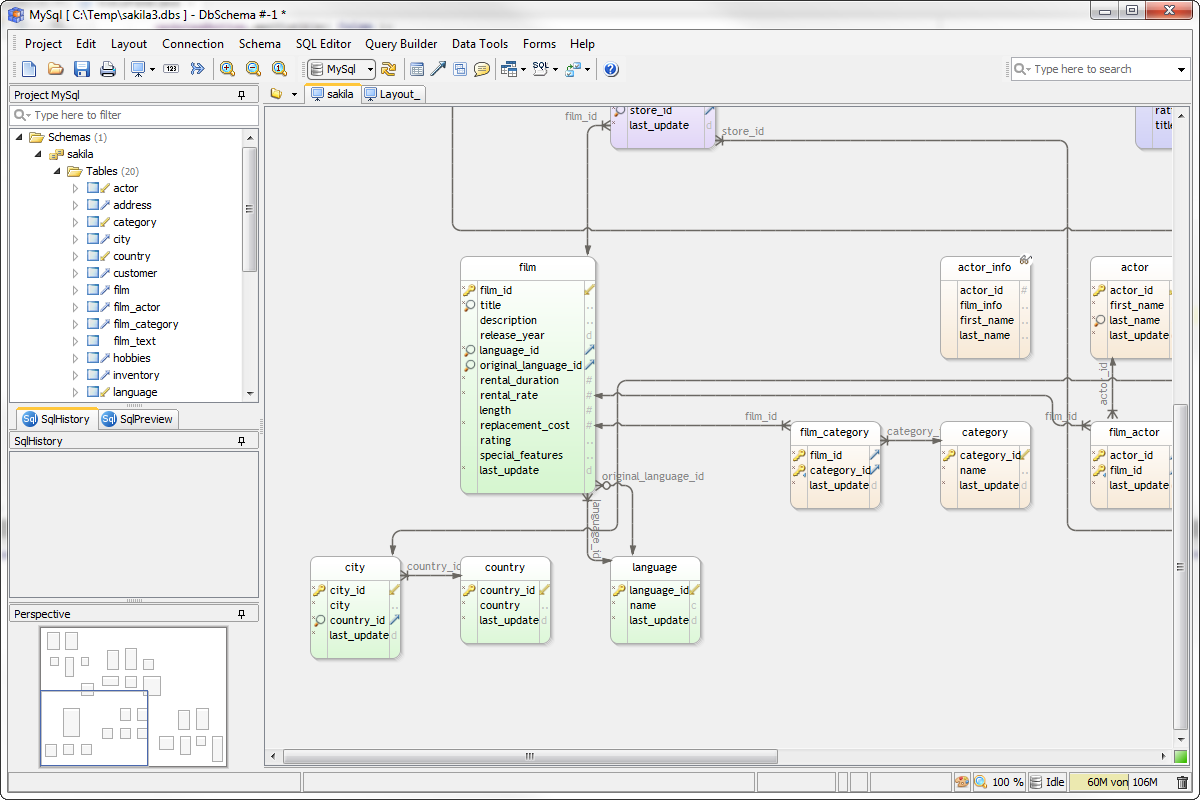

4. Design your database schema. A database schema is good to share with your developers entities that exist in your application and what their relationship are. I tend to use DB Schema or just Freemind to show to fields without the datatypes.

DB Schema

5. Understand and select your “stack”. Even if you want to outsource your application development I’d recommend you talk to a few developer friends who can educate you on the stacks they use – what the front end languages and libraries would be, what the back end language would be and the database options. You will be more confident when you talk to your outsourcing company and also be able to help make tradeoffs when you need them.

Yesterday at the #PreMoney conference the most frequently mentioned strategy for deal flow among venture capitalists was the “warm introduction” from an entrepreneur or an earlier stage investor. Since the easiest filter was someone’s capability to both judge you and your idea, most investors were looking for a “previously vetted” opportunity. That did not mean an automatic investment, just a guaranteed meeting with the investor.

I had a chance to ask Micro VC investors where they felt they could add the most value above and beyond the money. Most were of the opinion that fund raising, connections to potential hires and introductions to new customers were the areas that most entrepreneurs asked for help. There were other areas that entrepreneurs asked for help, but the top 3 tended to be the same.

A typical Micro VC fund investor has more likely been an entrepreneur before or has been an investor at a larger fund, so most of them had raised money before from VC’s or LP’s. They should have a decent network of other later stage investors and some of them have angel investor connection as well, so if you are earlier stage, then they could refer you to them instead.

According to CBInsights’s Anand, there are 1400 Venture firms in the world and 1/3rd of them in the bay area, so between 400 and 500. Each VC firm has about an average of 5 people in their team, of who, 3 would be partners. So there are between 1200 and 1500 partner-level investors. Most of the Micro VC investors I know have good relationships with at least 20-30 investors, with who they have likely done deals with or referred companies to. If they have only met another VC firm partner at conferences or events, or over coffee, it is very unlikely they will be able to give you a “warm” introduction.

When you get your pre-seed or seed round underway with a Micro VC fund or angel group, one of the key questions that will come up is who will be the investors at the next stage of the company. If that does not come up, then you should bring that up as a question. If the VC or you believe that their check or the seed round will be the last money you will ever need, then you should rethink your opportunity size.

If your investor knows 30+ partner-level series A investors, they are likely to filter the right investors by 2-3 primary criteria, and introduce you to them, given that they already know that most series A investors invest largely the same amount and look for the same range of milestones.

The primary criteria would be “domain expertise“, “value add” and “recent portfolio investments“. If a series A investor has expertise in SaaS HR, or SaaS marketing, and they can add value in the area your startup needs the most help with, for example, hiring people from other SaaS companies, so they would be a better fit.

Typically, most Micro VC funds I spoke with said they ended up making an average of 10 introductions, with the “hot” companies needing not more than 5 and the “still looking for the perfect metrics” requiring about 15 introductions.

An average of 6 out of every 10 companies that a Micro VC invested in (for the 13 people I spoke with) actually got to series A in less than 18 months without the Micro VC requiring another investment in the company was the average numbers I saw quoted as well.

At the 500 startups LP meeting and dinner last night, I had a chance to meet with Jeff Clavier. He is one of the first Micro VC funds (before they were a thing in valley). Their latest fund (Softech IV) is a $85 million fund. Jeff and I have known each other for years now, since 2005, when I first met him at a TIE conference and he’s still the same very approachable, friendly and simple guy – surprising given that he’s French – (sorry, Jeff, could not resist taking a dig).

A Micro VC fund has a much smaller team, is the first thing you notice. While larger funds like A16Z have over 100 people and even a a large fund such as Menlo might have over 20-30 people, a $50-$100 million fund, cannot afford more than 5-7 folks. Typically there might be 2-3 partners, and 2-3 associates or Vice presidents.

Which means you are pressed for time. Jeff, mentioned that he’d ideally like his time spent in thirds.

1/3rd of his time spent on sourcing new deals and working to build a pipeline of opportunities, by meeting new entrepreneurs and trying to help them even if he wont invest.

1/3rd of his time portfolio management, which includes spending time helping them with execution and operations, thinking about fund raising and helping make key connections and finally helping open doors to potential hires or prospective customers.

Finally a third of his time is spent managing the team, investor communications and networking with other investors at events, judging startup hackathons, and learning about new areas to invest in.

Each of the 3 partners at Softech VC does 5 deals a year, so they do 15 deals in the 3 years of investing in the fund. To do 5 deals a year, they end up meeting about 250-300 entrepreneurs he said, and roughly 2 times that many introductions are made to him from others.

Digging deeper, the first 1/3 of the time sourcing new deals begins largely by getting warm introductions, which were built by the years of working with other investors, and helping other entrepreneurs who have been the best source of his deals.

The 2nd third of his time is disproportionately taken up by warm email introductions and strategy discussions with his existing portfolio on fund raising. Typically Jeff stays on the board for 2 years, ensures that they company has a very good series A investor and then hands the board seat to them, keeping in touch with the entrepreneurs if they need his help. Which, according to him makes it all the more important to ensure that you think about later stage investors

Finally, the last third of time time is for “everything else” – which includes fund communication, meeting with new potential Limited partners, attending startup events, connecting with other entrepreneurs, discussions with potential M&A targets for teams and mentoring his own team, to discuss opportunities.

The first thing that strikes you is that this is a full time job. Many who claim that the the life of a General partner is mostly golfing, 2 hour lunches, 3 hour dinners, attending events, spouting knowledge about unknown markets and “networking”, dont appreciate the amount of time that it takes to source, manage and attract high quality partners who can help you connect with great entrepreneurs.

Second, unless you spend time (and lots of it) building good relationships with good potential downstream (assume that a series A investor is downstream from a seed investor) Venture capitalists, then you will have a hard time helping your companies raise more money and feel confident that your invested dollars are in safe hands with folks looking for the best interests of the company.

Tomorrow, I will touch on a topic that he and I talked about – how many “warm introductions” to potential investors, does it take to get a funding round done for an early stage startup.

Over the last 3 days I had a chance to meet with 12 Micro VC funds with 1 or 2 general partners and less than $50 Million in capital raised.

Most of these funds were of 2013 or later vintage and many were less than a year old.

Seed funds and Micro VC’s are looking like startups themselves and that’s a good thing.

They are adopting lean methodology (1 or 2 partners alone, not a big staff, no admins, doing all scouting themselves), hustling to get their initial customers (investors and entrepreneurs), shipping an alpha version ($1 to $5 Million first fund with only friends and family), building tractionand community (Blogging, networking, making investments) and then raising their seed round – a larger fund within a year for $5 – $25 Million) and looking for a way to differentiate their offering (focused investment thesis).

The new valley startup is the early stage seed investment firm.

There are over 250 Micro VC funds or super angels according to CB Insights. Most have under $50 million in investment dollars. In fact based on my cursory analysis, most are entrepreneurs who have decided to “spread their risk” among multiple startups than do one startup alone.

What are the steps to be a seed investment fund manager?

Raise capital from high net worth individuals or be rich yourself to start investing. Over 90% of these investors are entrepreneurs themselves. Except for 3 of the 12 I met, most did not have a “big exit” or success under their belt. Your first fund might even be less than $1 Million (alpha prototype version). Then your follow on funds can be $5 and then onwards from there.

Pick a niche or focus area and start to become an expert at it. There are Micro VC funds focused just on helping entrepreneurs who have a H1B visa, another set of folks just targeting startups in kitchen tech within food technology.

Setup a fund manager (legal, finance), banking and website.

Build relationships with other prominent investors or early stage angels who are doing deals to help you get “cut into deals”.

Invest and help the entrepreneurs as much as you can.

Most of these seed investors are entrepreneurs themselves, so they are scrappy, hustle oriented and founders themselves, so they tend to keep their costs low, focus on a few investments and from the entrepreneurs I have spoken to so far, help the entrepreneur at the early stage, a lot more than your traditional VC firm with partners on the board.

In some cases the investor can be a part of your team, as an extended sales, BD or marketing expert, pattern matching from their other investments and helping you learn from other’s mistakes.

A decade ago or more, raising funds was pretty difficult, so if you were a VC fund, raising capital was the biggest challenge you faced. If you raised capital, then deploying that capital and getting good deal flow was relatively easy. Now, though given that there are so many Micro VC funds, even getting good quality deal flow is a challenge.

Most of the Micro VC funds tell me that their network of folks they have worked with before, entrepreneurs, other investors and angels are their best source of deals, and service providers (such as lawyers, accountants, etc.) do offer some deals, but not as high quality. They also are consistent in their thinking that “cold” inquiries are the “most irrelevant” source of companies to invest in.

To attract quality deal flow beyond referrals, many are adopting strategies to “build their brand” by blogging, podcasting, startup videos, running networking events, extensive PR, building a network of customers and partners for “introductions” to startups. Most though, are till trying to figure out how to get more high quality deals that they should be in.

If you are an entrepreneur looking to raise money from a Micro VC fund, the biggest challenge will be that the follow-on funding from these funds for pro-rata will be largely nonexistent to highly unlikely.

Many funds are so small that they have to spread the risk among enough startups, so they keep very little cash for follow on rounds (or dry powder). Many do claim that they will raise another fund within a year or two just to do follow on rounds, but that remains to be seen.

Newer ipads and iphones will require the 6 digit passcodes. That’s apparently more secure than 4 digit passcodes.

The only reason to go to 6 digits is when your phone gets stolen by someone who can brute force 10,000 codes (with 4 digits). Well, apparently, most people use pretty common passwords, so if you only try 27 known passcodes (such as 1111) then your chances of unlocking the phone are at 67%. That means only a third of the people actually use complicated passcodes that will take more than 15 minutes to crack.

If however, you have 6 digits, then the combinations are a million (versus 10,000+) so, it should take longer and more effort to crack your password.

I doubt that. 90% of people will go with 111111 instead of 1111 is my guess, or 123456 instead of 1234. Now, your stolen phone will take 22 minutes to be unlocked instead of 15. Yay!

I am going to assume that most people will upgrade to the new OS version so about 500 million (534 million to be exact) iOS devices will be upgraded to 6 digit passcodes.

The median salary in the US is about $42,000 and the median iPhone users salary worldwide is higher – $53,000.

End note: I know the value of a stolen iPhone to a user (especially if there is a loss of life tragically in some cases) is much more than $250, but a 6 digit passcode is not going to change that for the better.

In discussions with 5 startup founders last week in the SF bay area, it is clear to me that the “hiring” challenge has gotten acute.

Here are some horror stories:

1. One founder spent time meeting the potential recruit’s at his kids school and swimming class locations so that he could get more time with the candidate. He mentioned he did not actually see his kids, but since the candidate used to come early to the school to pick up his kids, he could spend time with them.

2. Another CEO had his admin pick up and drop a candidates wife (who broke her leg) to the hospital. She was apparently covered by insurance, but not “top of the line” insurance, so the admin they showed them how much they would save if her husband were employed by their startup.

3. A third company has started a “get your spouse trained at work day“, where the significant other would come into work for a day each week (if they were unemployed) and find a way to get trained on a discipline they liked, which might open doors for them to other opportunities.

One of many formulae for hiring great people

I often get the question about “What are the best practices to hire great people” more than any other question in the Bay area.

What I know is that a set of “best practices” wont get you the best candidates. It will get you the rest. Why? To attract the best candidates you need to have a unique combination of meaningful work, great package and an irresistible culture.

The operative word on those 3 is unique. You will need to find uniqueness and differentiation on all 3 parameters.

As VC’s are getting picker and going up the food chain in terms of investing in “only proven startups with a lot of traction”, so are candidates.

It would be the case that a few years ago, you could ask a few employees to actively recommend people who they have worked with before and get a bonus for referring them.

Now, it is not unheard of when the hunter becomes hunted.

One of my good friends was looking to hire a colleague from a previous company, but he ended up joining the friend’s startup instead.

Meaningful work drives a lot of technical folks. Meaningful includes challenging, different and new opportunities. Surprisingly, it is also what a lot of non technical people crave.

A great package in itself with unique benefits is becoming table-stakes even for the best people. Now, the intangible benefits that extend to the candidates family are the thing to covet.

Finally, an irresistible culture that not only encourages success and outcomes but also is quirky to attract a specific segment of candidates is gaining more traction. Who knew that most of the people at a startup I knew were all big fans of Mochi ice cream? I did not. Turns out they only attracted rabid fans of that snack, who were also all great developers in a particular technology.

Hiring good people is always hard. I would focus on attracting a segment of people who are good with a uniquely set of tailored benefits, culture and work that makes it a little more easy to have you be self selected.