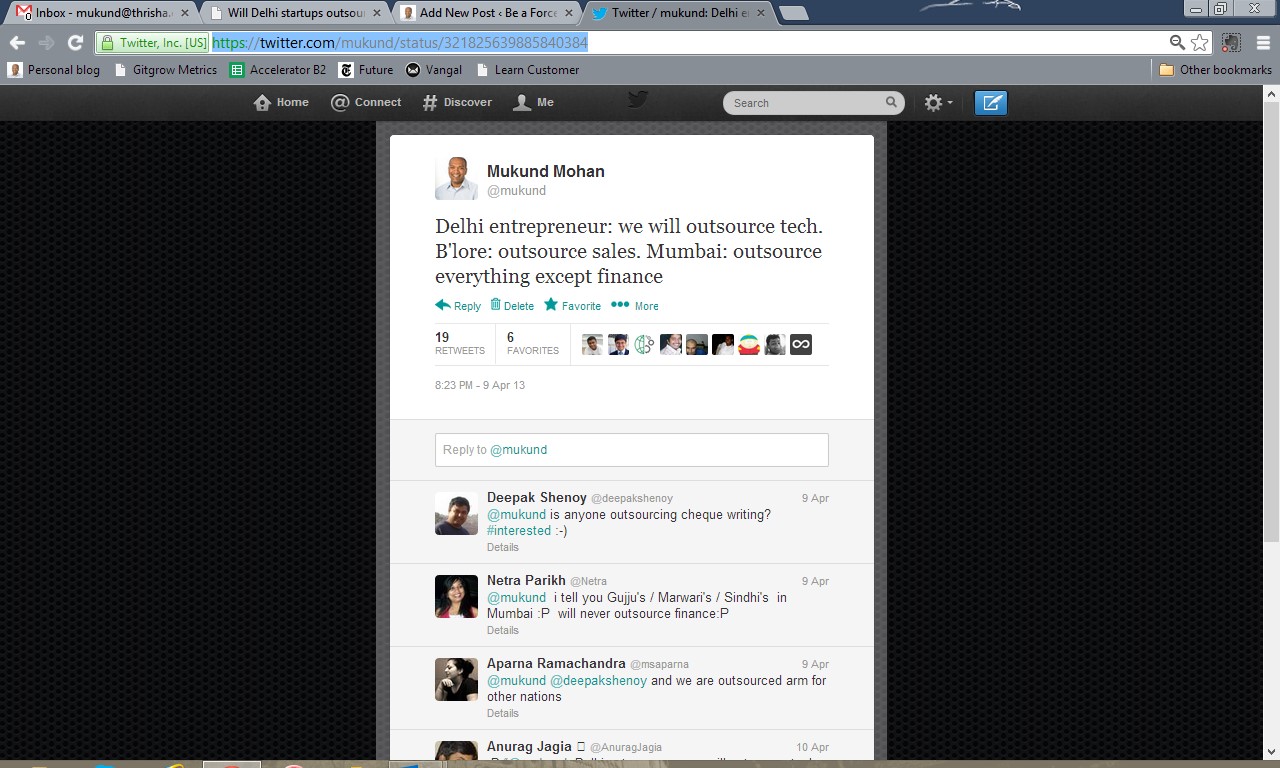

I put a half serious tweet last week based on several conversations I have had with entrepreneurs in Delhi, Mumbai, Pune, Bangalore and Chennai. I have been to Hyderabad as well, but the numbers are low.

I have limited data, since I am not in Delhi often. My observations are based on looking at 51+ applications from Batch 1 and about 60+ applications from batch 2 of our accelerator from NCR.

Besides that I have interacted in 5 events in the last 6 months at Delhi – Think Next at Saif, Reverse Pitch at 91 spring board, one VCCircle event, one at Leela with people matters and an event of Media companies and startups at Le Meridian. In all at these events I met a cross section of about 120+ companies and founders.

The following are my observations, so use a grain of salt.

1. I met fewer than 5% of developers and technical architects in these events and fewer than 2% of founders from our applications at NCR. The deep technical people dont come to these events or apply to our accelerator. We prefer meeting and dealing with developers, technical folks than generalists such as domain experts, marketing or sales founders. In contrast to those numbers, developers make up 14% of Bangalore applications and Pune a close 10%.

2. Delhi founders dismiss strong technology plays as “engineers building solutions in search of a problem”. This statement is my interpretation of a “show of hands poll” that I did in 2 events.

3. In our internal database of 402 technology and software companies we track at Microsoft based in Delhi, our own biased, internal ranking of “technical” expertise at these companies, our average rating is at 2.9 on a scale of 5. Bangalore and Chennai top at 3.7 and 3.5, followed by Pune at 3.3. I cant share more details about the ratings yet, but will do so as we get more comfortable with sharing this data and not getting people flaming us for that.

While we are certainly not dismissing Delhi as a non-technology startup hub, we certainly dont see deep fundamental technology startups in storage, cloud infrastructure or networking from Delhi. Bangalore or Pune are likely better bets for those. This data was reconfirmed to me by both SAP and Intel who have startup engagement programs in those cities.