In the early part of the 20th century, startups were funded largely by wealthy families and individuals. Today, we would call them “angel” investors. Examples include firms such as Pan American World Airways, Eastman Kodak, and Ford Motor Company.

The formation of American Research and Development Corporation (ARD) is often associated with the birth of the venture capital industry as we know it today. Founded in Boston, Massachusets by prominent bankers, academics, and businessmen, ARD raised $3.5 million for a closed-end fund in the fall of 1946, with more than one-half coming from institutional investors.

One of the founders of ARD was General Georges Doriot, then a professor at Harvard Business School. He taught a course called manufacturing that was really “all about starting companies and technology.” A number of his students and disciples went on to be prominent venture capitalists, including Tom Perkins (Kleiner Perkins), Don Valentine (Sequoia), Bill Elfers (Greylock Partners), Arthur Rock and Dick Karmlich (Arthur Rock & Company), and Bill Draper and Pitch Johnson (Draper & Johnson Investment).

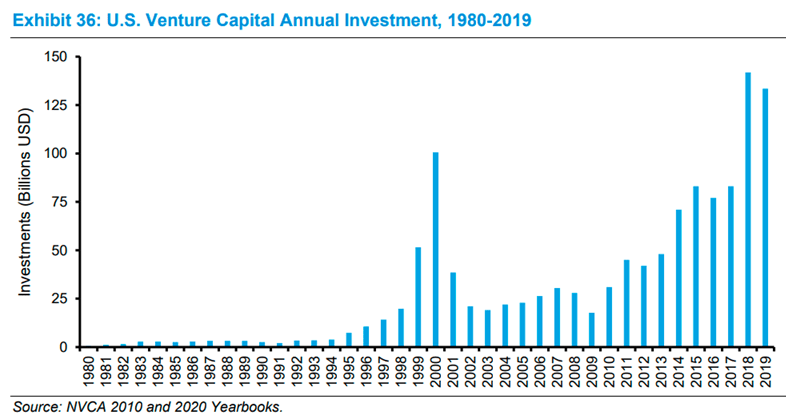

The venture capital industry then went through its greatest period ever starting in the mid-1990s. This was in part fueled by the adoption of the Internet, ushered in by the meteoric rise of Netscape, an Internet browser, following its IPO in August 1995.

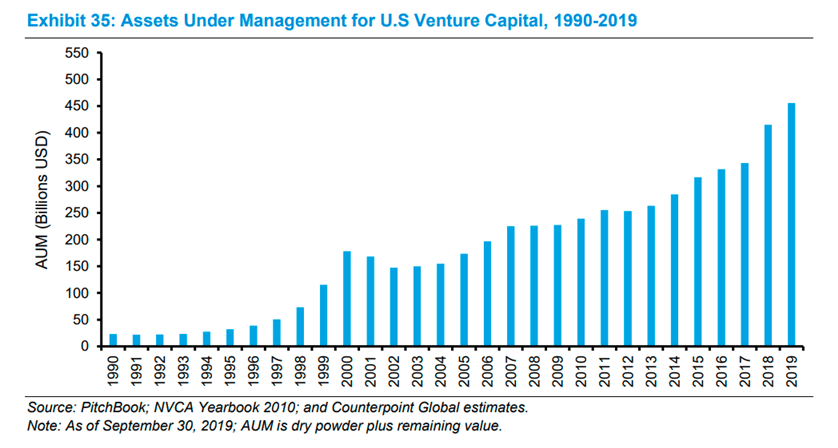

The fee structure for venture capital funds is similar to that of buyouts. The management fee is typically 2 percent of the total amount raised by the fund, and the incentive fee is commonly 20 percent of profits. But venture capital and buyouts differ in their ability to scale. In buyouts, doing large deals is not materially different than small deals. As a result, buyout firms can grow their AUM with less degradation of expected returns than can venture firms.

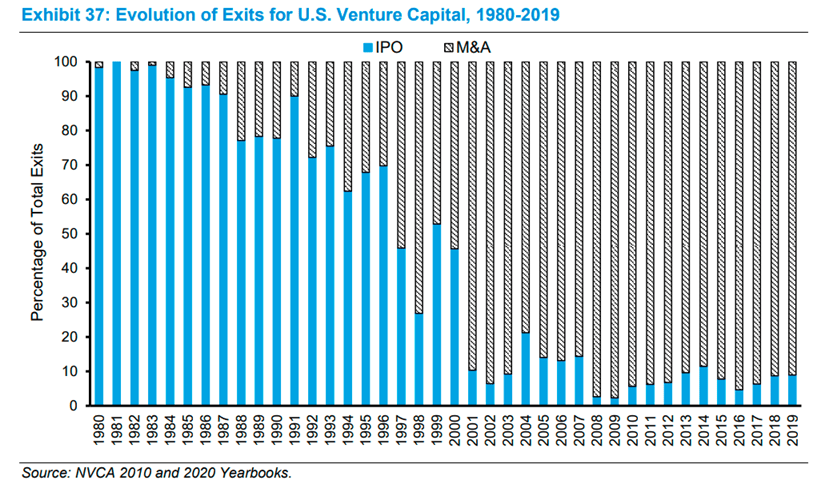

Exits. The return for any fund is a function of the difference between the purchase and subsequent sale of investments. From the beginning of the venture industry through the mid-1990s, an IPO was the most common way to profitably exit a venture investment. In the late 1990s through 2000, both IPOs and a sale of the business were popular. But since 2000, IPOs have declined substantially, and a sale, either to a strategic buyer or a buyout fund, has become the preferred vehicle for exit.

There are a number of drivers behind the trend of fewer exits through IPOs.

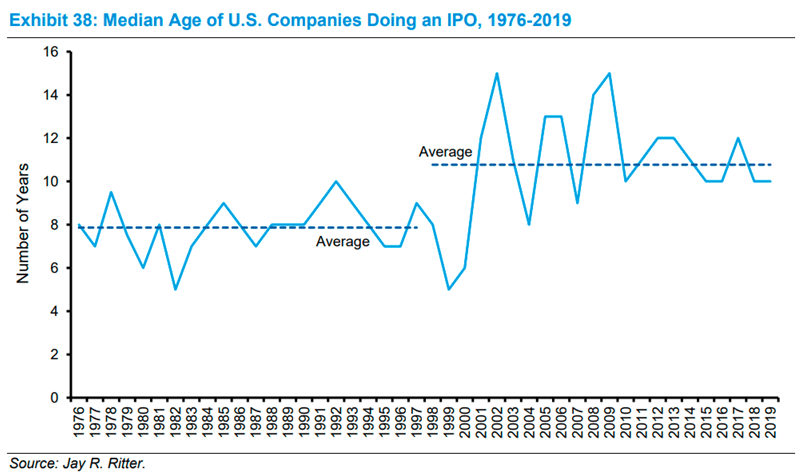

First, because the cost to list has risen in recent decades, only larger and typically older companies are in a position to list. The age of a company doing an IPO has risen as a result.

Second, the motivation to go public has shifted. Young companies today don’t need to raise capital from the public market because they are generally less capital intensive than their predecessors.

Third, even those companies that are in very competitive industries have been able to stay private because there is a huge amount of capital available via late-stage funds.

Finally, there are now ways for employees who are compensated in equity to sell shares. In some cases, funding rounds give employees a chance to cash out.

These drivers have important consequences for investors.

There is now a sizeable population of companies that are very valuable on paper. For example, CB Insights, a platform that tracks market intelligence in the technology industry, counts 225 “unicorns” in the U.S. worth a combined $662 billion as of July 2020.

Another consequence of staying private longer is that more wealth is created in the private market and less in the public market.

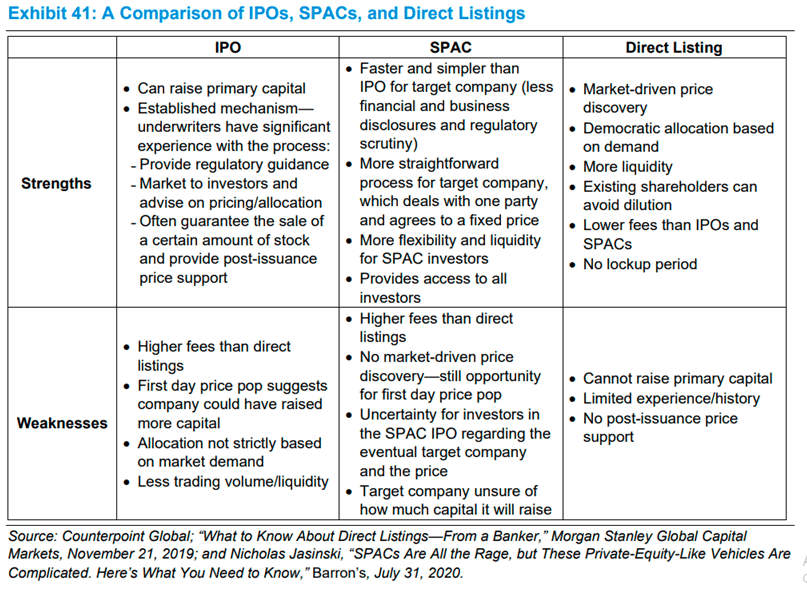

Despite the decline and delay of IPOs, many venture capitalists view an exit into the public market as attractive due to the accountability and transparency associated with being a listed company. At the same time, it has become more common for entrepreneurs and investors to consider a sale to a special purpose acquisition company (SPAC) or a direct listing as alternatives to a traditional IPO.

A SPAC is a company that goes public with the goal of using the offering proceeds to make an acquisition. In an IPO, a SPAC offers a unit that includes a common share at a set price and warrants. SPACs are sometimes referred to as “blank-check” companies and can provide public market investors access to private companies.

With a direct listing, a stock exchange builds an order book, whereby buyers and sellers express their interests in terms of price and volume. The exchanges do this every day for every stock. The opening price reflects the intersection of supply and demand. Buyers include any investor, and sellers include shareholders, such as employees and early-stage investors. Neither buyer nor seller has an obligation to transact.

A final consequence of staying private longer is that the combination of steady flows of capital into venture and later exits means a much larger share of the industry’s total investment is late-stage. For example, in 1980 around 10 percent of investments were late stage. By 2006, roughly 20 percent of dollars went to investments of $50 million or more, and that figure was closer to 60 percent in 2019.

/arc-anglerfish-arc2-prod-mco.s3.amazonaws.com/public/YZPX42HZSZF67PM7NZY4PPA44Q.jpg)