Another weekly feature I want to start is an analysis of a new market, so I can understand trends and learn about opportunities.

The hardware market for servers is a fairly large market overall. These are expensive high end systems that have a 7-10 year life-cycles and tend to be shelved and end-of-life-ed after that.

According to IDC and Gartner over $50 Billion dollars is spent on server hardware each year. That constitutes about 8-9 million units each year. So, the average unit price of a server is about $5000.

There has been a dramatic shift on both sides of this market – the buyer (service providers and data center owners) and the sellers (OEM’s, ODM’s and Contract Manufacturers).

First the buyers. The biggest tend has been the rise of the cloud. From 70K to 85K buyers and service providers in 2000, there are now only 25K buyers. The rest of the companies have “given up and gone to the cloud”.

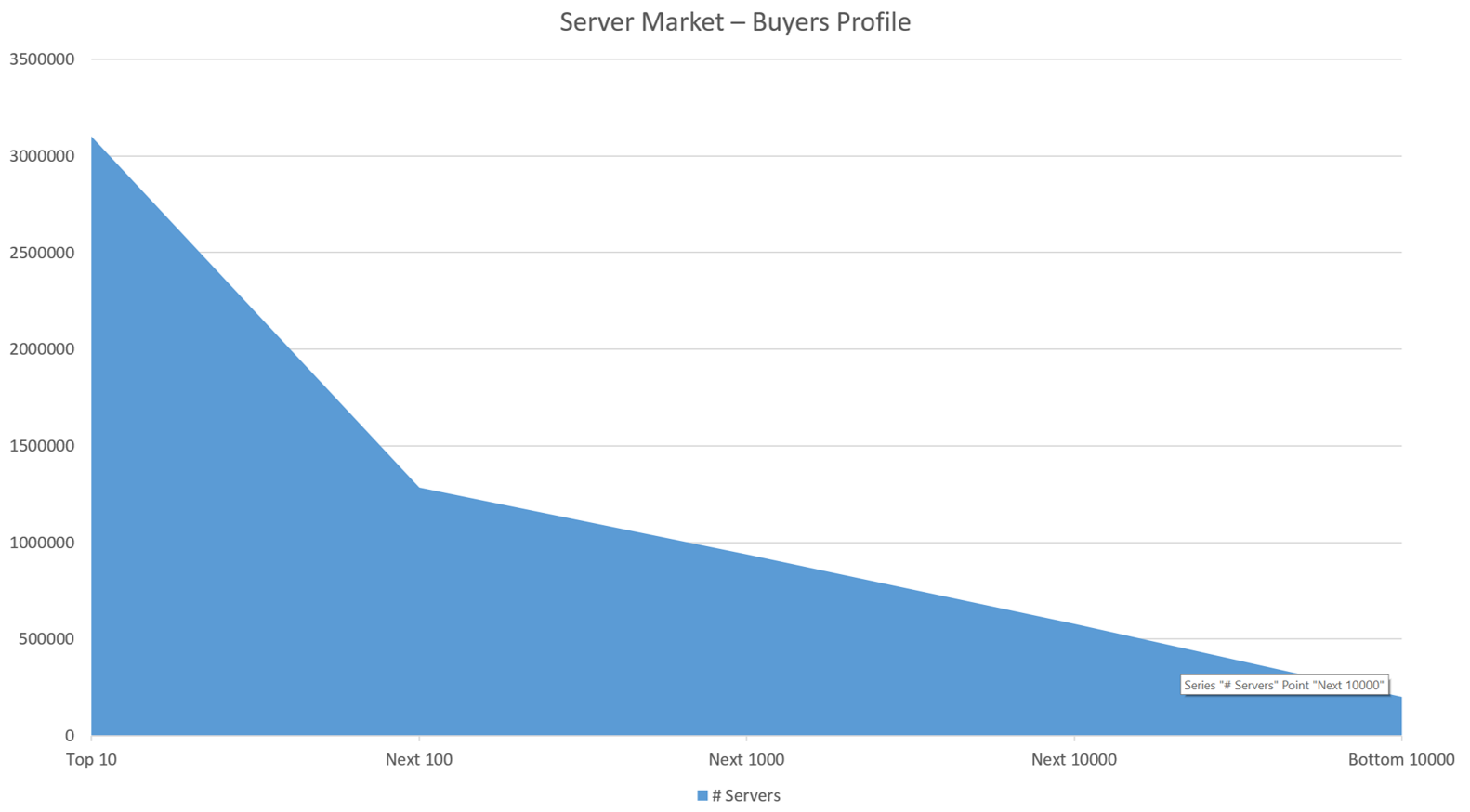

The second trend, related and a resulting effect of the first trend, on the buyer side we have gone from a even spread at the top (long head) to a sharp head (consolidated top buyer profile).

What that means is that in 2000, the top 100 buyers accounted for 25% of the server purchases. Now in 2015, the top 10 buyers are accounting for 25% of the purchases. That indicates consolidation in a significant level. Companies like Google, Facebook, Twitter, Baidu, Tencent, Alibaba, Sina, Microsoft, IBM (with acquisitions) and Amazon (AWS) now account for a quarter of all server purchases annually. The next set of buyers – traditional ISP’s such as AT&T, Verizon, GoDaddy and about 1000 others account for 10% of the market.

Finally buyers are now also purchasing more “commodity” servers with cheap hardware components and systems and going away from expensive OEM servers. While HP,Dell, IBM and Lenovo continue to be the market leaders, more ODM’s such as Quanta, Wistron and Invetec.

What this means is that the major OEM vendors are losing market share to ODM’s and contract manufacturers or Electronics Manufacturing services (EMS) such as Foxconn and others.