ChatGPT has more paying subscribers than Twitter Blue as of March 1st 2023.

The information reported that it obtained an internal document, on Feb 6, 2023, from Twitter, which put the total number of Twitter Blue ($8/ months) subscribers at 180,000. [1]

The business of apps reported that as of Feb 2023, ChatGPT had 100 Million users. [2]

With 667M visits in Dec 2022, 893M visits in Jan 2023, OpenAI moved to over 1 Billion visits in Feb. [3]

Not surprisingly the audience skews heavily US (20%), young (61% are under 35) and mostly male (61%) of the 100M.

Among the top 5 people profiles, 1/ students, 2/ teachers, 3/ marketers, 4/ content writers, 5/ software programmers make up over 52% of the users.

So to find out who’s paying for ChatGPT we need to triage information from multiple sources since OpenAI has not shared the number of paid users. ChatGPT Plus ($20 / month) was introduced on Feb 1, 2023. [4]

According to a survey of developers on Feb 6th, nearly 7% of them were willing to pay for ChatGPT [5]. Multiple surveys reveal the number of paying subscribers it far less than 1%.

Doing the math with number of people by role and the conversion rate, I estimate the number of paying users to be 215K, which is more than Twitter Blue subscribers.

Software version control is a very important element of the lifecycle of development. Developers share the latest version of code they are working on in a repository that helps all team members be on the same page.

Gitlab $GTLB filed to go public today and the S1 provides their overview, strategy and growth plans with financial background, which I will breakdown. This is an important software category so I am keen to seek a position in the fast growing company.

$GTLB helps multiple developers work on the same code without stepping on each others code or hindering the other’s progress. Each developer works on their own “branch” or copy of the main code and after making changes will “commit” changes via a “merge request”.

$GTLB Gitlab is an online hosted platform built on open source Git to help organizations manage their code repositories and the entire software development lifecycle.

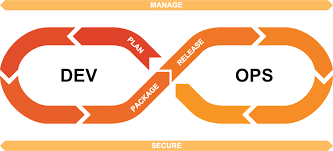

$GTLB now has a complete platform for DevOps (Developer + Operations) which helps companies deliver software faster, securely and with fewer bugs. This helps them have an archive of previous changes and versions.

$GTLB The complete lifecycle of Devops spans project planning, or Plan, to source code management, or Create, to continuous integration, or Verify, to static and dynamic application security testing, or Secure.

$GTLB allows packaging artifacts, or Package to continuous delivery and deployment, or Release, to configuring infrastructure for optimal deployment, or Configure, to monitoring it for incidents, or Monitor.

Finally $GTLB helps to protect the production deployment, or Protect, and managing the whole cycle with value stream analytics, or Manage.

$GTLB was founded in 2014, a few years after the founders started their open source project, by Sytse “Sid” Sijbrandij (CEO), Dmitriy Zaporozhets and Valery Sizov.

In 2015 $GTLB raised series A funding from Khosla ventures and has raised over $400M to date. Gitlab was last valued at $6B in a private market transaction in Jan 2021.

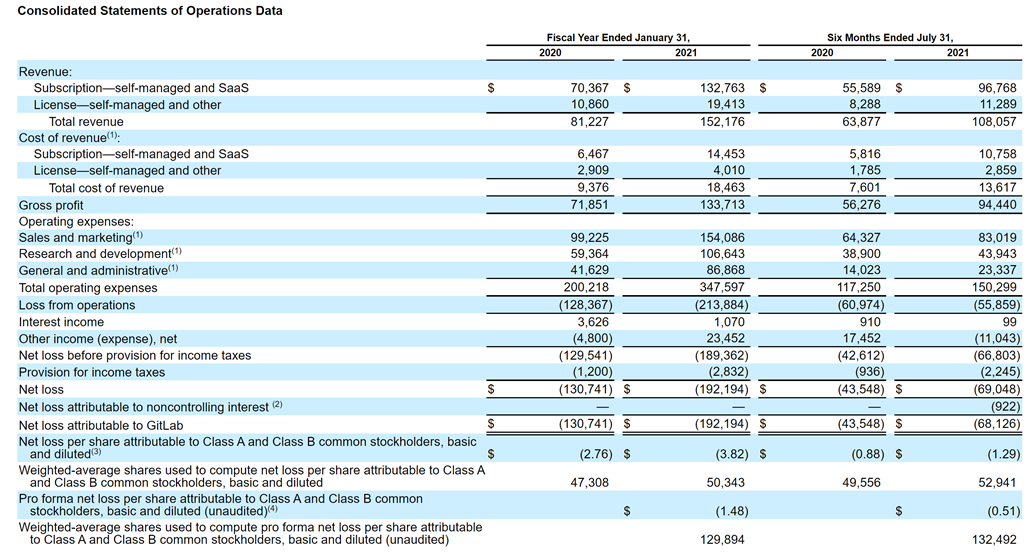

$GTLB Revenues in CY Q2 rose by 69% to $58.1M ($230M annualized), with losses at $40M. The company has over 1345 “fully remote” employees in 65 countries. They have a net retention rate of 152% – which is among the best in the industry.

$GTLB gross margins are a very healthy 88% (industry leading) and 52% operating margins, which are terrific as well. They have over 3600 customers and over 2600 contributors to their open source projects. 383 customers spend over $100K annually.

From a few friends who use $GTLB in the valley they are a very sticky application. Once a customer decides to implement Gitlab they rarely leave.

$GTLB competes with $TEAM Atlassian (BitBucket) and $MSFT (GitHub) and many other source code repository solutions. The market opportunity for the DevOps Platform is approximately $40 billion according to Gartner, which makes this a large TAM.

My analysis: I like $GTLB a lot and will be interested in a position, but I suspect given market conditions the company will be public at $10B to $15B valuation, which implies a 43X to 65X NTM revenue multiple for a company growing at 69%. If I am able to get in under $9B valuation, which I doubt, then I could consider sizing up to 2% of my portfolio.

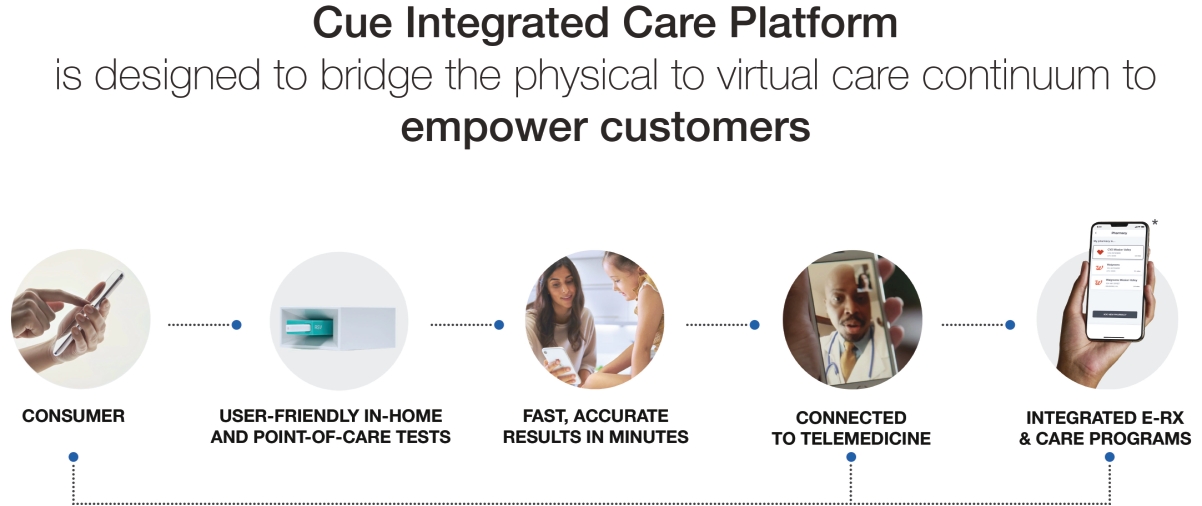

$HLTH is a fascinating company and I am going to take a very different approach to this IPO overview. Cue Health manufactures a rapid healthcare diagnostics product. It is similar to home glucose meters or pregnancy kits.

Cue $HLTH intends to sell its devices direct to consumer. It is currently sold to healthcare professionals. It currently provides a rapid (25 minutes) Covid 19 test, which is FDA approved.

$HLTH – In 2009 after the SARS virus, Ayub Khattak (UCLA 2010) and Clint Sever, co founders of Cue decided to build a device that detects the virus at “home” instead of going to a diagnostics lab to test for the virus.

$HLTH founders

After multiple iterations and funding from incubators, accelerators and other institutions, they launched a version of their diagnostic device in 2015. Sold for $150 (pre order) or $300, it detected vitamin D deficiencies, testosterone levels and influenza. Each test can be administered with a cartridge (sold for $2 – $10 each). The device itself is handheld.

Users provide a nasal swap, or drop of blood or saliva, depending on the test. Results arrive in minutes, displayed on an iPhone or Android smartphone using the Bluetooth.

If this reminds you of Theranos (yeah, I had flashbacks too), the similarities end quickly. Since March 2020 the company got $481M in funding from the Department of Health and Human services (HHS) to ramp up production of its Covid19 diagnostic test.

$HLTH claims efficacy close to other (95%+) detection. The test is administered to patients by using a proprietary nasal swab (“Cue Sample Wand”); the swab is inserted into a small medical device (“Cue Cartridge Reader”) that analyzes it with a high degree of accuracy.

Cue Health has received funding from Johnson & Johnson (NYSE: JNJ)

$HLTH The U.S. government plans to buy about 6 million of the test swabs from CUE plus around 30,000 analytic devices to perform the patient sample testing analysis.

Cue $HLTH has received funding from Johnson & Johnson $JNJ and many others as well. (Disclosure: a colleague & acquaintance Ashish X is on the board of $HLTH and I have no position in the company).

In Dec 2020, $HLTH raised $235M at over $2B in valuation. It mentioned at that time that the Department of Defense, the NBA (National Basketball Association) were all customers.

With over 100 patents and over 1000 employees, the molecular diagnostics company has benefitted from the Covid19 test and ramped up revenue significantly.

$HLTH although the only test available now is Covid19, the company plans to launch (Late 2022) other tests as well.

$HLTH near term pipeline is strong and some of the other diagnostic tests are expected in 2021 as well.

Financials: Although 11+ years old, until 2020, $HLTH had no revenue. In 6 months of 2021 they booked $202M in revenue (+ Infinite YoY :). With 57% gross margins, they still managed $32M profit (Whoa) or $0.22 per diluted share. This is profitable company, but huge losses in 2019 (20M) and 2020 ($47M)

$HLTH has over $260M worth of convertible notes, however, so expect more dilution post IPO.

Risks: $HLTH is new, it is a young company which is scaling quickly thanks to the Covid19 – where it faces other competition as well. Although it is a 10 year old company, the production and ramp up has only begun in 2021.

$HLTH has not proven it can actually deliver all those other diagnostic tests as well. If the FDA revokes the EUA (Emergency Use Authorization) for Covid19, expect revenue to drop significantly.

In the near term (18 months) $HLTH is dependent on Covid19. Going by vaccination rates in the US, it seems like a safe bet, that they will continue to do well.

$HLTH depends on the US Department of Defense (DoD) for nearly 83% of revenue. This is another big risk. As part of their obligations to the DoD, they have to deliver 30K Cue readers and 6M Covid test kits. They currently have 100K per day manufacturing capacity in San Diego.

$HLTH has over 50 other diagnostic testing market competitors, many of which are much larger.

Valuation $HLTH has not mentioned its valuation, but it is expected to be between $3B and $4B (expected estimates) or higher. There are no growth metrics expected, but the DoD contract runs for 3 years. Commercial customers are also purchasing bulk Cue kits. At $3B this will be approximately 6X and at $4B 8X EV/Revenue, which is much higher than any other diagnostic competitor.

$HLTH has net income so the valuation metrics for EV/Net income should be 49X EV/Net Income at $3B valuation.

I am certainly going to watch this IPO closely. I am very interested in the $HLTH platform overall and keen to build a position for the long term

$BIRD Allbirds, a shoe company based in San Francisco, founded in 2015 by Joe Zwillinger and Tim Brown. They filed for an IPO and are looking to raise $200 – $300M in funding at $3B-$4B in Valuation.

$BIRD is a global lifestyle (shoes and apparel) brand with a focus on sustainable shoes. In 2016 Time Magazine name their Wool Runner, the “Worlds most comfortable shoe”.

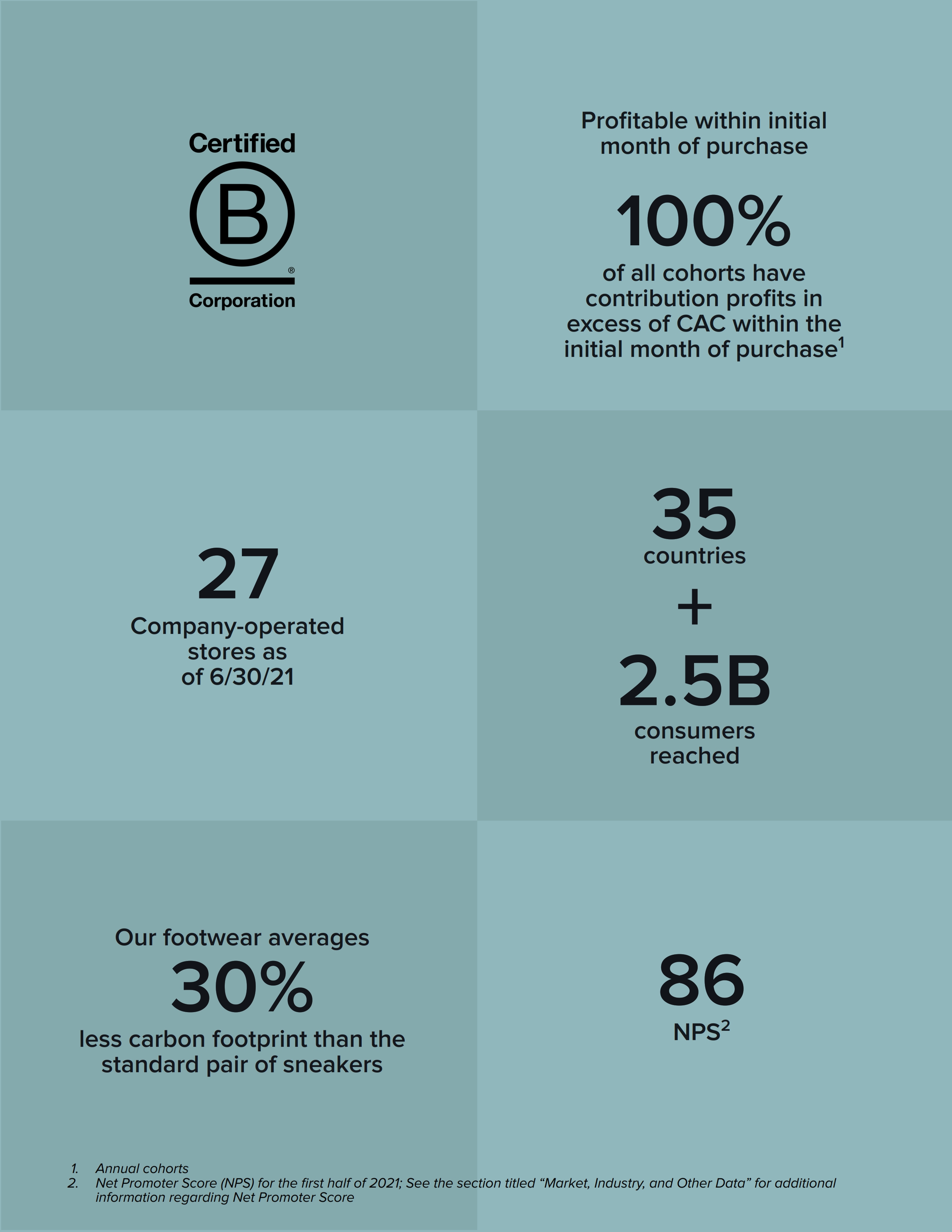

$BIRD online and direct to consumer channels account for 89% of their revenue, while 27 stores account for 11%.

Allbirds founders

Since their founding $BIRD has sold 8 Million pairs of shoes to 4M customers worldwide, of which 3.3M are in the US.

Financial facts: 2020 $BIRD revenue was $219M +31% YoY, at 51.4% gross margins, generating $25M in losses.

Market Opportunity: $BIRD targets the $1.8T footwear and apparel market, ($366B in footwear alone).

$BIRD estimates their shoes cause 30% less carbon footprint than competitors sneakers. Thanks to this, they have a purpose driven brand and customer who are engaged and connected with the products.

Approximately 53% of $BIRD net sales in 2020 came from repeat customers.

$BIRD last raised $100M on Sep 2020 at $1.4B in valuation. Given the current brand hype we can expect $3B – $4B in valuation, which would imply a 15X – 20X EV/Revenue with negative EBITDA.

The biggest risks to $BIRD are counterfeit knockoffs are proliferating the market, the perception that the brand produces expensive products and it is a niche brand appealing to a very limited set of customers.

I am going to watch this from the sidelines. I like $BIRD and it has a cult-like following, but I am going to watch the post Covid and post IPO execution as a public company for 1-2Qs.

If I do see acceleration in revenue and EBITDA I might be interested in $BIRD.

$FRSH I first met Girish Mahtrubootham (Founder & CEO of Freshworks) in 2010 just a month after he started FreshDesk. We met at Infinitea Cafe in Bangalore. He had left Zoho, his previous employer to start his new venture FreshDesk.

Through the years I kept in touch via WhatsApp messages and emails to see the remarkable success story he created. This week $FRSH filed to go public, showing $308M in LTM revenue growing at 49% YoY. IT was last valued at $3.9B in Nov 2019. Expect a $7B – $12B valuation at IPO.

$FRSH makes Software-as-a-Service solutions for businesses to help them with sales, customer service and help desk automation.

The Customer Relationship Management (CRM) market is a $120B worldwide opportunity, with 100s of companies, most notably $CRM (Salesforce), $MSFT (Microsoft Dynamics), $SAP (SAP), $NOW (Service Now), and $ORCL (Oracle) dominating the enterprise segment.

In the Small and Medium business (SMB) segment, there are many other competitors including $ZEN (Zen desk), $HUBS (Hubspot) and many others who compete with $FRSH

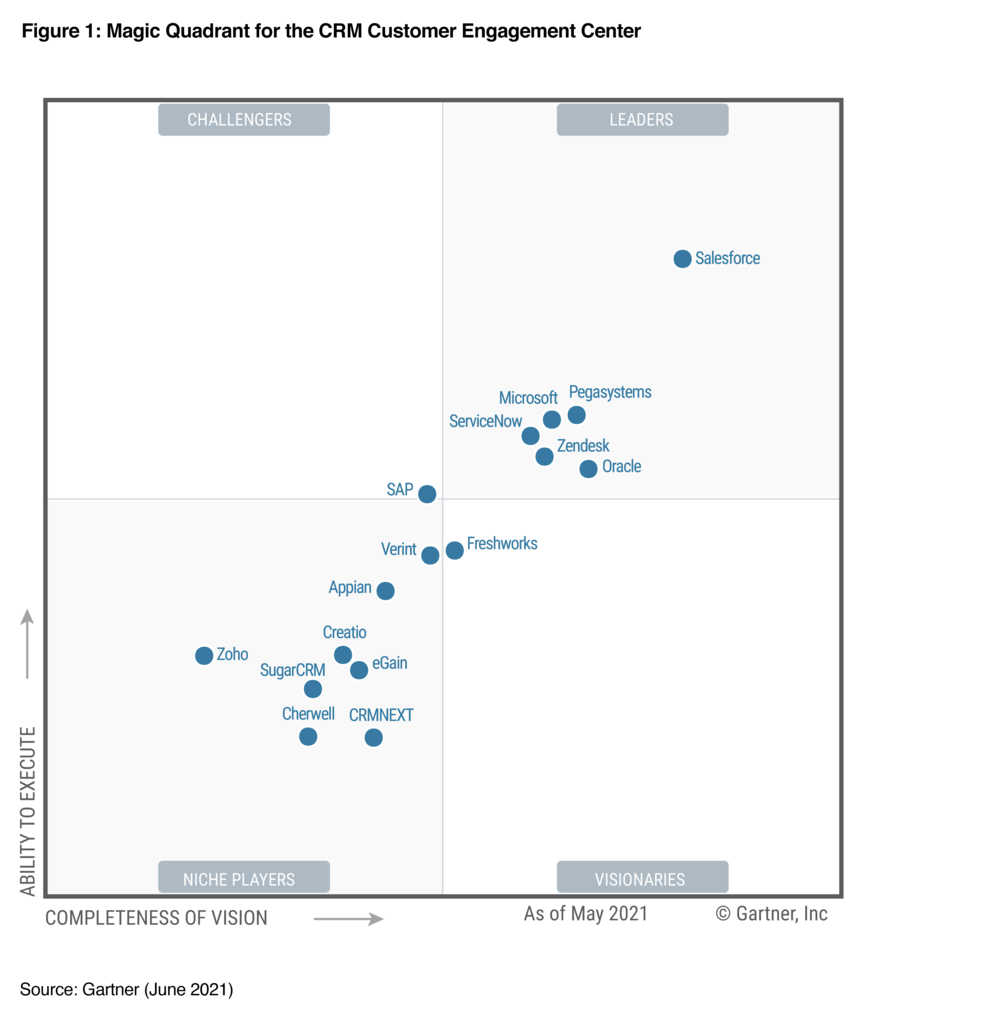

In the Gartner magic quadrant from May 2021, $FRSH Freshworks is named as a Visionary, with the large companies occupying the “Leader” category.

$FRSH has 52K customers worldwide, and in 2020 reported $250M in revenue and $57M in losses. With 80% Gross margins, sustained growth over 10 years and a global presence, this stock should do well given good market conditions.

$FRSH operational metrics: DBNER (Dollar Based Net Expansion Rate) is 118% and while CAC and LTV metrics are not shared, the cost of sales and marketing is 45% of revenue. Over 11K customers spend more than $5K per year on their software.

The company is spending significantly in marketing to attract customers. Churn among customers certain industries which were affected by Covid was higher is what the company shared.

Dollar based net expansion by cohort

$FRSH company culture is explained using the acronym CHAT – Craftsmanship, Happy work environment, Agility with accountability and True friend of the customer. In addition they use the word Kudumba (family) which binds the team together.

$FRSH Competitors: $HUBS is growing at 30% YoY with $808M in 2020 revenue and is valued at $30B, while $ZEN is growing at 25% YoY with $1B in 2020 revenue, valued at $15B. At $7B in valuation, the company will be valued at 22X NTM EV/Revenue and will be in the mid point of valuation for SaaS companies at 50% growth. At $12B in valuation, it will be valued at 38X EV/NTM, making it among the top 5 richest valued companies in the SaaS space.

$FRSH largest shareholders currently are Tiger Global (26%), Accel India (25%) and Accel USA – Sameer Gandhi (25%). While founder Girish owns 7.8%.

I am going to buy $FRSH shares at IPO depending on the price and hold for a long period. I personally know Girish well, and few others members of his team as well are close friends. I expect them to continue to execute well.

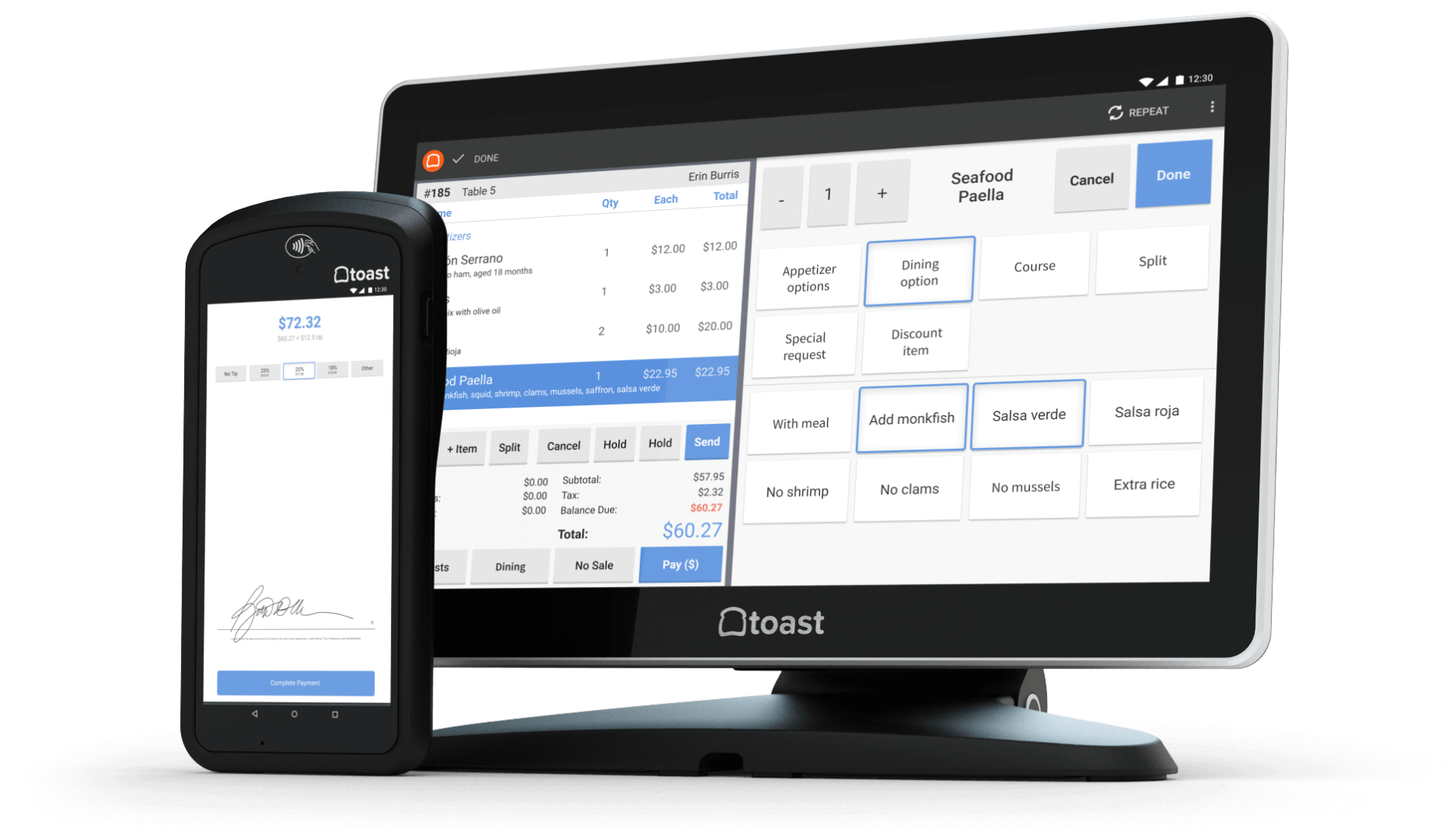

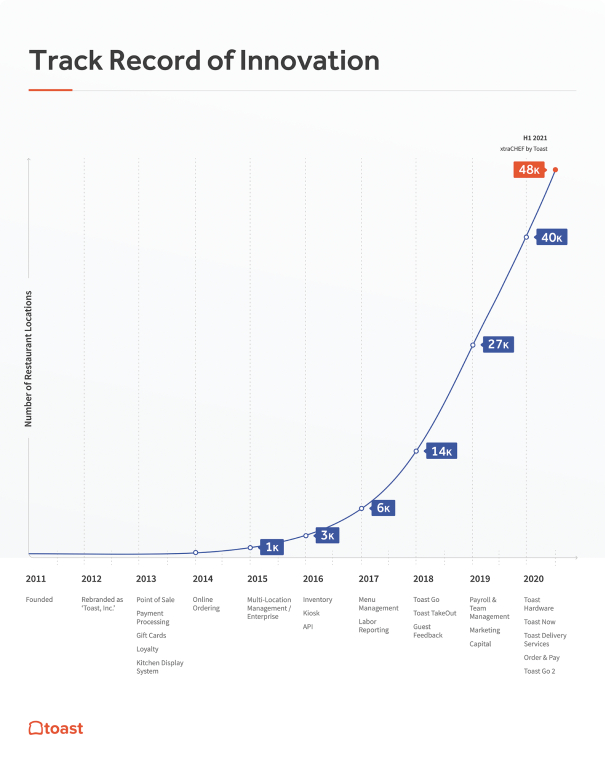

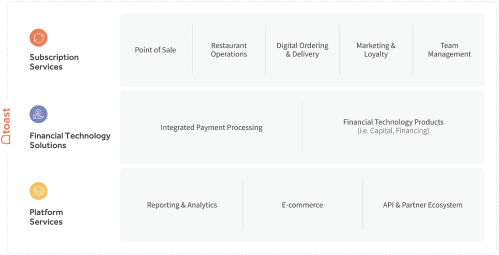

$TOST Toast a Boston based technology company providing payments and software for restaurants (competes with $OLO) filed to go public this week.

$TOST Toast provide Point of Sale (POS) offerings and software to restaurants. It was founded in 2011 by Aman Narang, Jon Grimm, and Steve Fredette.

$TOST sells restaurant payment-processing hardware, including tablets and handheld devices, as well as cloud-based software to manage orders, payroll, and marketing.

According to Statista there are over 660K (860K according to $TOST) restaurants in the US alone, of which 48K (7% market share). The average restaurant makes about $125K per year, and spends 4% – 11% of revenues on Toast.

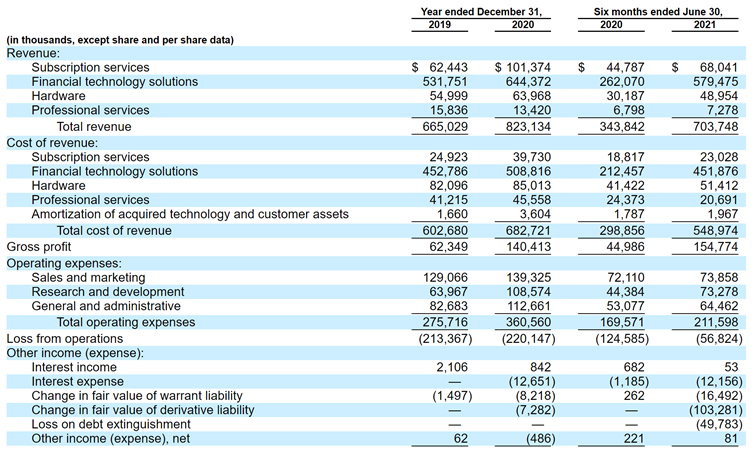

$TOST claims a $15B addressable market of which it currently does about $1.2B in revenue NTM (next twelve months). $TOST processes $38B in payments (Gross Sales via its platform) as of June 2021.

In Feb 2020, $TOST raised $400M in funding at valuation of $4.9B. It recorded 100% revenue growth in the 1H of 2021 growing to $704M, as losses hit $235M increasing 88% YoY. Most recently in Nov, it allowed secondary sale of its stock by employees at a $8B valuation.

Toast founders

$TOST Toast takeout is the app the company provides to restaurants to help them grow online takeout and delivery options for consumers.

$TOST competes with $SQ Square, $LSPD Lightspeed commerce, and $FSV Fiserv in the payments market for restaurants. $OLO also competes with $TOST but focuses on offering chain restaurants end-to-end solutions instead of only segmenting independent restaurants.\

In April 2020, Toast cut its staff by 50% to 1300 after Covid, but by Nov 2020 it raised market valuation again $8B.

$TOST also lends money to restaurants using Toast Capital (similar to $SQ Loans and Lend).

At $20B valuation, $TOST will be valued very rich at 6.6X NTM gross profit (nearly 3X $SQ) and nearly 13X NTM revenue (not a good measure given low gross margins) for 100% Covid fueled recovery.

Key risks for $TOST are very low gross margins (10% aggregate) and less than 9% gross margins in payment business, very competitive landscape for restaurant software, payments and high churn rate of restaurants (11% of customers go out of business each year) and slower growth going forward from Covid recovery easing out.

I am going to watch $TOST but not take a position yet. S1 filing indicates late September IPO.

$WEBR Outdoor Bar B Q grill maker and 75 year old company Weber filed to go public looking to raise $750M at $5.5B Market Cap.

Weber grills

Weber makes makes 7 types of grills – Charcoal, Gas, Smokers, Pellet, Electric and Tech-enabled grills.

$WEBR has grown dramatically thanks to the pandemic, recording 17% YoY growth to end 2020 (Sep) at $1.5B in revenue with 43% Gross Margins (+78% YoY) and $150M in Net profit

The market for grills is about $5B in 2020, growing at 5% YoY, and is expected tor each $7B by 2025 and $WEBR Weber has over 25% market share.

Competitor Traeger $COOKhas also filed to go public.

$WEBR plans to use proceeds to pay down debt of $220M and for other corporate purposes.

Valuation: While EV/Rev is not a valid metric, it is 2.98 and with EPS of $0.47 the Covid growth rate of 61% might slow causing shares to form a base to grow into the valuation, given the EV/EBITDA will be about 26.

$COOK is valued higher given its 100%+ Growth rate during the pandemic and is at EV/Rev of 4.4 and EV/EBITDA at 32.

The biggest risk to $WEBR is slower growth post the pandemic tail winds. I expect this to be a steady performer, but not a growth stock. At this point I dont plan to take a position, but it will return 10% – 25% annual would be my expectation.

$RSKD Riskified, a software and services company focusing on payments industry, helping eCommerce vendors reduce fraud from online transactions, went public last week at $21 valuing the company at $3.3B.

$RSKD Riskified was founded in 2012 by Eido Gal (CEO and Assaf Feldman (CTO). It has raised over $70 M from General Atlantic, Fidelity Management and others

$RSKD core product is Chargeback Guarantee which automatically approves or blocks online transactions. Riskified’s business model is to collect a percentage-based fee on gross merchandize value (GMV).

$RSKD In the second quarter of 2021, Riskified expects revenue of $54.8-$55.7 million, up 46% from the corresponding quarter of 2020. Gross Margins are in the 53% – 54% range.

$RSKD Gross profit in the second quarter is expected to be $30.1-$33.7 million, up from $20.1 million in the corresponding quarter of 2020, while the operating loss is predicted to be between $900,000 and $5.5 million, narrowing from $7.7 million in the second quarter of 2020.

$RSKD Net loss in the second quarter of 2021 is expected to be $19.4-$24.8 million compared with $7.3 million in the corresponding quarter of 2020.

$RSKD While no public competitors exist, there are 10-15 startups including Forter, ClearSafe, Kount and Sift Science.

The market for fraud prevention is expected to grow from $20B in 2020 to $38B by 2025.

There are 5 products that Fraud detection and prevention vendors offer:

Automated Workflows

Automates the sending of order details, payment fraud checks, blocking of suspicious devices, fulfillment, cancellation of fraudulent orders, and more so merchants can review even a high volume of orders quickly.

Machine Learning

Uses real-time insights that are fed into the machine learning models. Machine learning does faster and more complex calculations across a much wider range of online fraud signals when compared with manual review.

Insights Dashboard

Insight dashboards report synthesize relevant fraud prevention data, display algorithmic conclusions where given, and highlight suspicious activities via a single, easy to use interface. This means there is no need to switch between multiple views to see all relevant information, in turn making it much easier to organize and effectively execute a fraud prevention process.

Device Fingerprinting

Device fingerprinting is the technique of recording information about the device a shopper uses when placing an order. A wide variety of data points are analyzed, including things like the computer’s operating system, the browser the shopper used during check out, and even the language options installed. The information collected is then used in a risk assessment to identify fraudsters. For example, a shopper claiming to be from a country whose national language is not installed on their computer can indicate the shopper is using a VPN to hide their true location.

Chargeback Guarantee

Chargeback guarantees are a contractual obligation on the part of a fraud prevention solution to cover the cost of any chargebacks incurred by a merchant using their platform. When merchants use a fraud prevention solution that offers one, they never have to pay the cost of a chargeback themselves.

Growth and valuation

$RSKD expects to do $210M – $220M in FCY21 revenues, growing at 51% YoY. At the current price of $26, it is valued at $3.45 Billion giving it roughly 16X P/S for 2021. Given the growth, and comparables at 17-19X SaaS valuations, at 60% margins, $RSKD is fairly valued.

$RSKD Risks include the ability for payment vendors ( $PYPL $SQ and $AFRM among others) to include these “features” or fraud detection with their core product. Second, the slower growth expected post Covid for eCommerce GMV.

$RSKD I think the valuation and numbers are good for an initial starter position under $25 with a risk of falling to $21 (IPO price)

Since many folks ask me about recommendations for email newsletters I read and follow, I thought I’d put together a list. I subscribe to over 300 and get daily updates from 50, of which I skim about 40 and read 20 daily in detail.

Here in no particular order.

Top SubStacks which I like (in no particular order)

$DIDI is going public on June 30th, selling 288M shares at $13 – $14 per share, raising $4.5B at $63B to $68B. $SFTBY (Softbank) $UBER (Uber) and $TCHEY (Tencent) are among the biggest shareholders. $AAPL (Apple) is also an investor.

$DIDI my big fear is revenue recognition is inconsistent, which makes valuations and metrics seem better than they are. That’s the biggest risk.

$DIDI was founded in 2012 by Will Wei Cheng, merged with Kuaidi in 2015 and acquired $UBER China in 2016. It operates in China, Brazil, Mexico and 11 other countries.

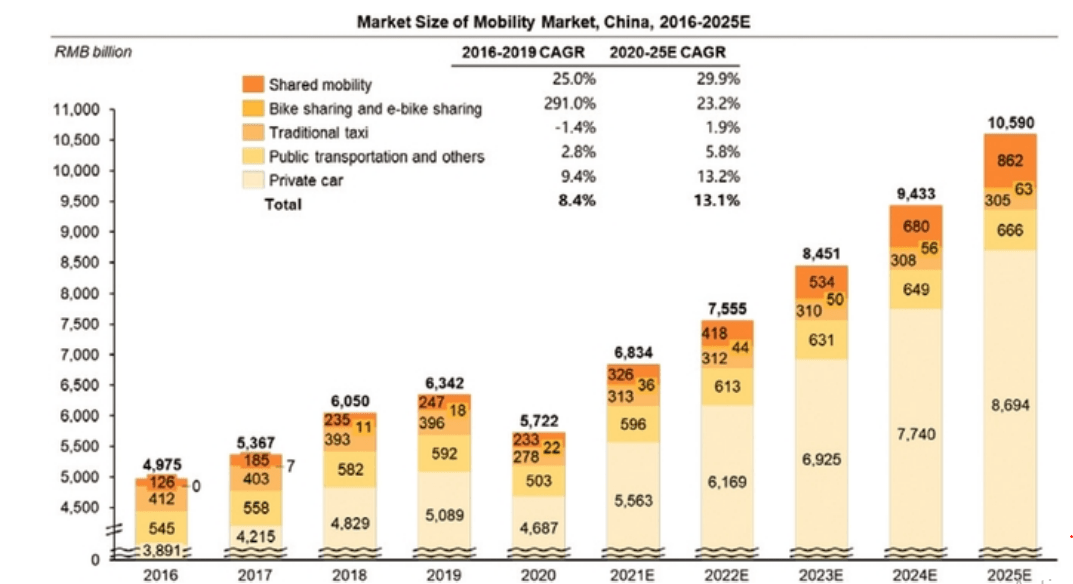

Didi Chuxing $DIDI is the leader in the Chinese shared mobility sector, which is over $300B and growing as a market.

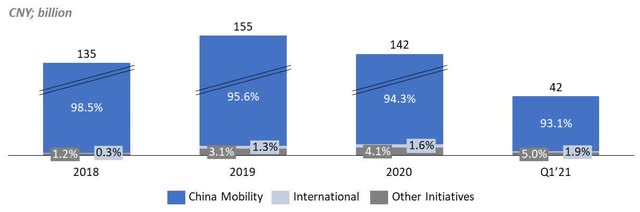

$DIDI revenues were down 8% in 2020 thanks to Covid, but were growing over 20% before. China mobility still accounts for over 90% of revenue.

$DIDI gross margins are in the 10% – 12% range and albeit small, have scale on their side.

At 24X last 12 months gross profit, the valuation for $DIDI is rich, but if growth can go back to over 20% YoY from 2022, this current price of shares might be a good value.