My searching and researching habits have dramatically changed over the last few months because of ChatGPT and also to some degree Google Bard.

The big advantage of these platforms is that they answer the question.

The problem before is obvious – when you have to search the answer to something you have to visit 2-3 pages and read “a lot of junk” before you formulate the answer to the question. Especially when the answer is factual.

Clickbait sucks. This image was generated by AI – the nose is weird

This is especially true with click-bait articles – such as “You will never know how many Instagram users Facebook has?”.

After reading 4 paragraphs of nonsense, totally unrelated to the question, the writer then gives you the number in word form.

Now, I rarely use the Google search bar on Chrome to text my Google search. ChatGPT and Google Bard are 2 tabs always open.

While specialized tools for each job are important, most people have a Swiss army knife with them. That’s for 80% of the job for most people.

ChatGPT is the Swiss Army Knife

Last week over 100 Generative tools were released – from resume builders to Bloomberg Finance GPT.

List from Generative AI page on LinkedIn

While most people I believe will still use ChatGPT, each role (engineers will still subscribe to CoPilot from GitHub, and marketers will likely subscribe to ChatSpot from HubSpot) will have their special tools.

I liken this to the similar explosion of eCommerce and B2B sites in 1997 – 2000.

Amazon would help you buy everything, but collectors loved eBay, and overstock still exists as does Zappos for shoes and Zulily for fashion.

Frequently Asked Questions

Why can’t Google do better than ChatGPT? They have better resources, lots of talent and money.

Google can do better, will do it and is already doing this. The same can be said about when Google first came and Microsoft had more money, resources and talent but still got upended by Google in search. ChatGPT has distribution quickly (over 100 Million users). While another AI chatbot is a click away, so is Google search. Still, billions of people use Google over Bing because it is better.

2. Do you need more than one chatbot? Is there room for Bard and ChatGPT?

Most people will use one or two chatbots (or more) depending on their need. Most people like to have a second opinion, especially when it comes to non factual questions. Meaning, when questions are subjective in nature, you need to get another opinion.

Many datasets (such as LinkedIn or Facebook) will not share their data with either Google or OpenAI. They might roll out their own chatbot. The folks that need it will use them.

When Netflix first came, most people did not think they needed more than one streaming service. Now we have 10+ in the US alone with over 10 Million users and the average user has 3 accounts or more.

Twitter Blue is a premium subscription service from Twitter that offers a few features and benefits. Some of the key features of Twitter Blue include:

The ability to undo a tweet that you just sent.

Customization of themes and colors for your Twitter experience.

Access to exclusive content from your favorite creators.

A “reader mode” that makes it easier to read long tweets.

A “collections” feature that lets you save tweets into folders.

Twitter Blue is currently available in a limited number of countries, but it is expected to roll out to more countries in the future. The service costs $84 per year, or $8 per month if you subscribe on the web, and $11 per month (if you subscribe on Apple or Android Store).

Created with stable diffusion

Twitter Blue is not essential for everyone. If you are not a heavy Twitter user, or if you do not think you will use the premium features, then you might be better off saving your money.

Previously Twitter had (legacy) verified accounts which had a blue check mark (for celebrities, governments, etc.), which they are now sunsetting.

Which has many of these journalists & celebrities balk at paying $8 a month for the service – which seems lame, because on average they spend more on their coffee in a day than that. I presume it is a “principle” of it.

Twitter does have wide distribution, so I am curious to see if these folks will continue to use it as much.

Already I have seen many (over 10) reporters claim Twitter is dead or dying since Elon Musk took over, claiming that engagement is down for them.

Created with stable diffusion

On the other hand, many entrepreneurs who I have spoken to in the last 3 months, have gone from 10 to over 1000’s of users.

What’s happening is that Twitter (like everything else) is changing. The old guard no longer has the content or voice that resonates with the Twitter crowd any more.

Second, as the platform has become more egalitarian under Musk, the old guard resents the fact that everyone else “does not know who they are”.

I actually like the play to pay model a lot. While it has some downsides, which is you can impersonate someone else by just paying $8 per month, the upside of meritocracy in content is appealing.

Ultimately, whether or not to subscribe to Twitter Blue is a personal decision. If you think you will use the premium features and benefits, then it might be worth the money. However, if you are not sure, or if you do not think you will use the features, then you might be better off saving your money.

In 2018 I joined an eCommerce company as the CTO. The company had fired its founder and replaced him with a new CEO.

The company has about 250 people, but just before the founder was fired, they had about 400. So they lost over 35% of their staff.

Over the next three years revenue went up and stabilized after a tumultuous period of ups and downs. The company went from 250 to about 90 people during that period.

Revenue was up after 3 years. Website was better performing, conversions were up and staff morale was better. But, the number of employees was down 75% from the peak.

That is when I realized that although well meaning and intended, most companies overhire during their “growth phase”.

The rise of filler jobs

The problem is “filler jobs”. Instead of automating processes or eliminating features, executives add more people to attempt to “move faster”.

These jobs should have never been there in the first place. Instead, taking a little time to remove under-utilized features that don’t deliver for customers is one approach. Or automating a task using a temporary developer or contractor.

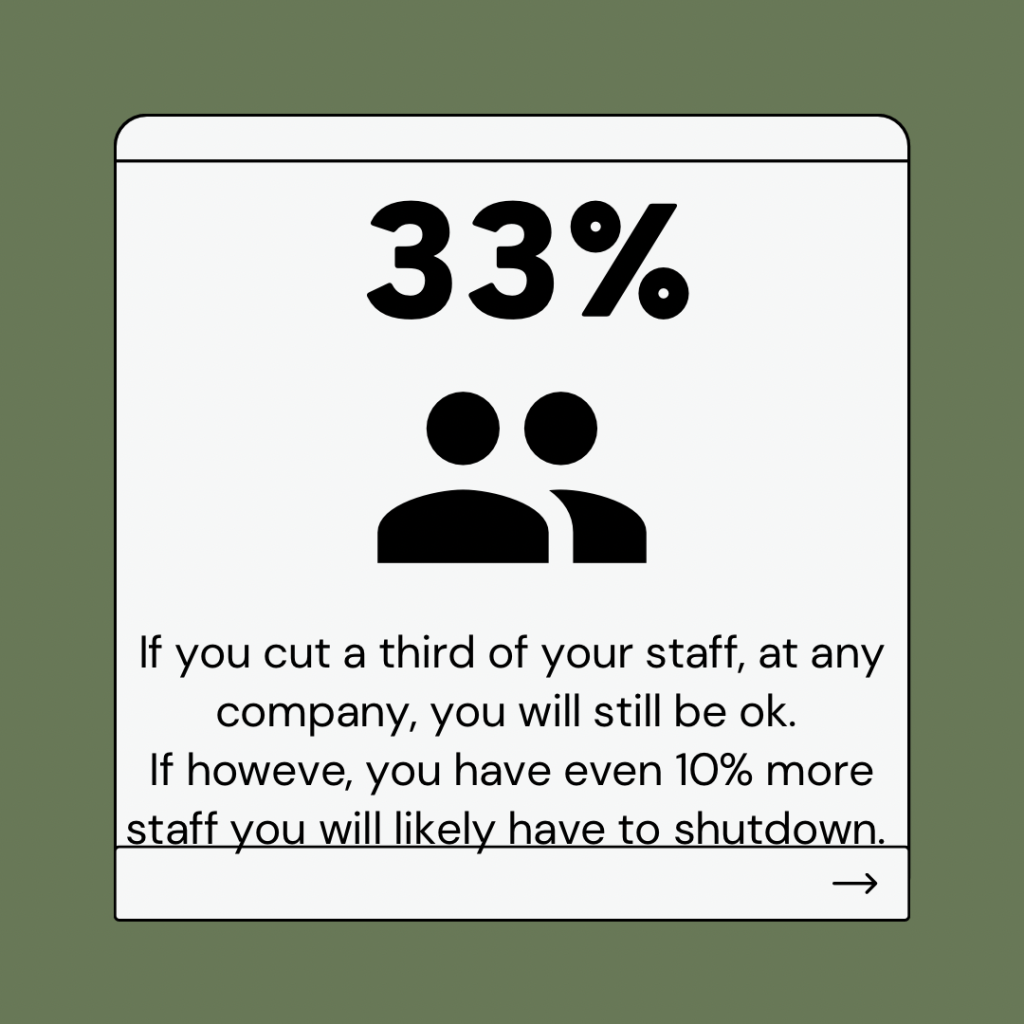

I don’t know the exact number of people companies have in excess, doing “filler jobs”. My estimate is 33%.

Most companies have 33% extra staff

I say 33% since you can safely cut a third of your staff if you are over 50 or so people and the business will still run. You may grow the same or more than you did before. You might have a slight dip in morale but that recovers.

As AI starts to proliferate in the workplace I see companies starting to have rolling layoffs. That will become the norm.

The reason is now CEOs realize many jobs are filler jobs. Second, Elon Musk with Twitter has shown that it’s okay to reduce staff and still have a functioning site. Third, AI will force people to leverage technology to do more in their job or be eliminated.

I have a need for a series of blog posts for my new project. I narrowed down 5 options 1/ ChatGPT – paid or free, 2/ Jasper.AI – a specialized content writing platform priced at $49 per month, 3/ Bard – free, 4/ Bing Chat – free and 5/ Using a writer on Fiverr.

Created with Dall-E

I stated with writing only 1 blog post and tried the approach of using the “same prompt” for all the generative AI solutions and mostly the same brief for my Fiverrr gig.

Create a 1500 word blog post on “review of courses on options trading ” using this URL –

TLDR: If you are seriously interested in using these and other solutions, I dont think the game is using one versus another. I used all of them and they each gave me different things to make the blog post better.

The first was Google Bard.

While I was expecting it to be not a great experience, it surprised me with a concise article, with relevant facts and a good summary. It did not, however give me 1500 words. It came closer to 500-600 words.

Next I used ChatGPT.

It did a good job with some generic writing, which I had to tweak, but its content was different from Google Bard. It tended to be more generic writing however, so I had to rewrite quite a bit. I used it more for the framework and for checking the overall structure.

Next was Bing Chat – which refused to write a blog post, saying it was not capable to do so. Instead I had to give a different prompt “Summarize the page for me and give me 3 pages like this, and summarize those too”.

Since Jasper.ai offers a 10,000 word free trial, I tried, that too. Of the lot it is the best for “writers”. But if you want it to generate a lot of content, I am not convinced yet that the $49 per month is worth it. It is very good if content is your job, but for someone like me the “free and good enough” options were way more useful.

Finally I tried giving the brief to “Fiverr“. 1 day later, I am still getting responses and bids.

The good thing about Generative is that its writes for you. It can create content with simple prompts. For example, I created an AI image with the “prompt” – Artificial Intelligence Enabled Chat Conversations in StarryAI.

But for good quality content (as opposed to the base, standard nonsense it usually spits out), you need to coax it with a very descriptive prompt.

Image created with StarryAI

I am not sure why it generated this image. It has nothing to do with my prompt as you can see.

Turns out you have to speak to it in not “human language”, but using a specific set of keywords which is the prompt syntax.

On Night Cafe, I used the same prompt and got this.

Again, I am not sure what this is either – It is not “Artificial Intelligence Enabled Chat Conversations” in my mind.

That’s why “Prompt Engineering” is a thing and companies are paying $350K a year for those jobs.

Substack, the email newsletter subscription business, today announced it will allow its writers and creators to invest in its startup starting at $100 and increments thereof.

Substack is looking to raise $2 Million at a pre money valuation of $585 Million.

They have 2 million paid subscribers, and 35 million subscribers, allowing for $300M to be paid to writers (their goal is writers keep 86% of the money earned from subscriptions).

You do not have to be an accredited investor (have over $1 Million in liquid assets) to invest in the round, and can invest at least $2200 or even start at $1000.

I think the valuation at $585M is rich, relatively speaking but I dont know all the numbers.

Here are some assumptions based on the data provided:

They are probably doing $150M to $200M in overall revenue given they have paid $300M overall to writers and have 2M paid subscribers. At an average of $7 per month per subscriber, it rounds up to $168M LTM (Last Twelve Months).

Their take is 10% or about $15M to $20M, which is their “actual revenue).

The growth rate seems tremendous, which I am assuming is over 100% YoY given 2 years ago they had only 100K paying subscribers.

So $20M in revenue, growing at over 100% YoY and you are paying 25X to 30X in Market Cap to Sales – Very rich, but this is the private market. They still are probably stuck in 2021 valuations.