Double Verify $DV is a software company that ensures brand safety an detects digital advertising fraud for brands. DV was founded in 2008 by Alex Liverant and Oren Netzer in New York.

The company has about 650 employees and was acquired in 2017 by Providence Equity Partners.

Double Verify Ad Tech IPO on April 22, 2021

$DV provides online media verification and campaign effectiveness solutions for brand marketers, agencies, advertising networks, demand-side platforms, exchanges, and digital publishers looking to ensure quality advertising environments, campaign transparency, and performance.

DV is a unified service and analytics platform for Ad optimization

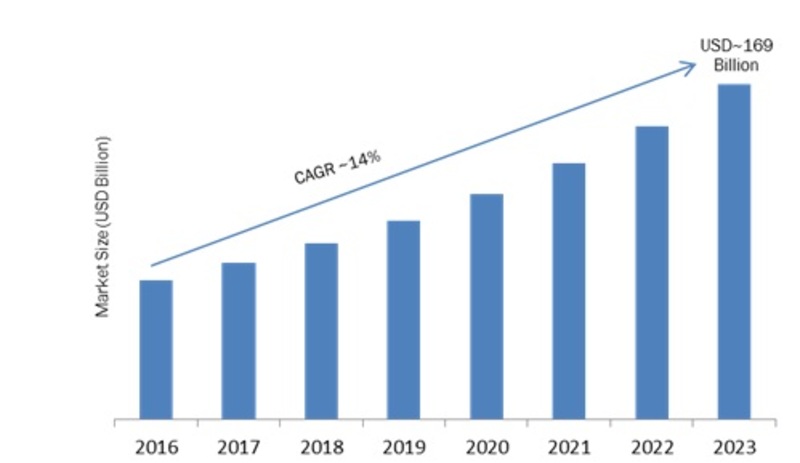

The marketing analytics software market was an estimated $2.7 billion in 2019 and is expected to reach $8 billion by 2027.

Advertising Marketing Analytics Market

$DV technology platform provides advertisers with data and analytics that can be used to optimize the quality and return on digital ad investments.

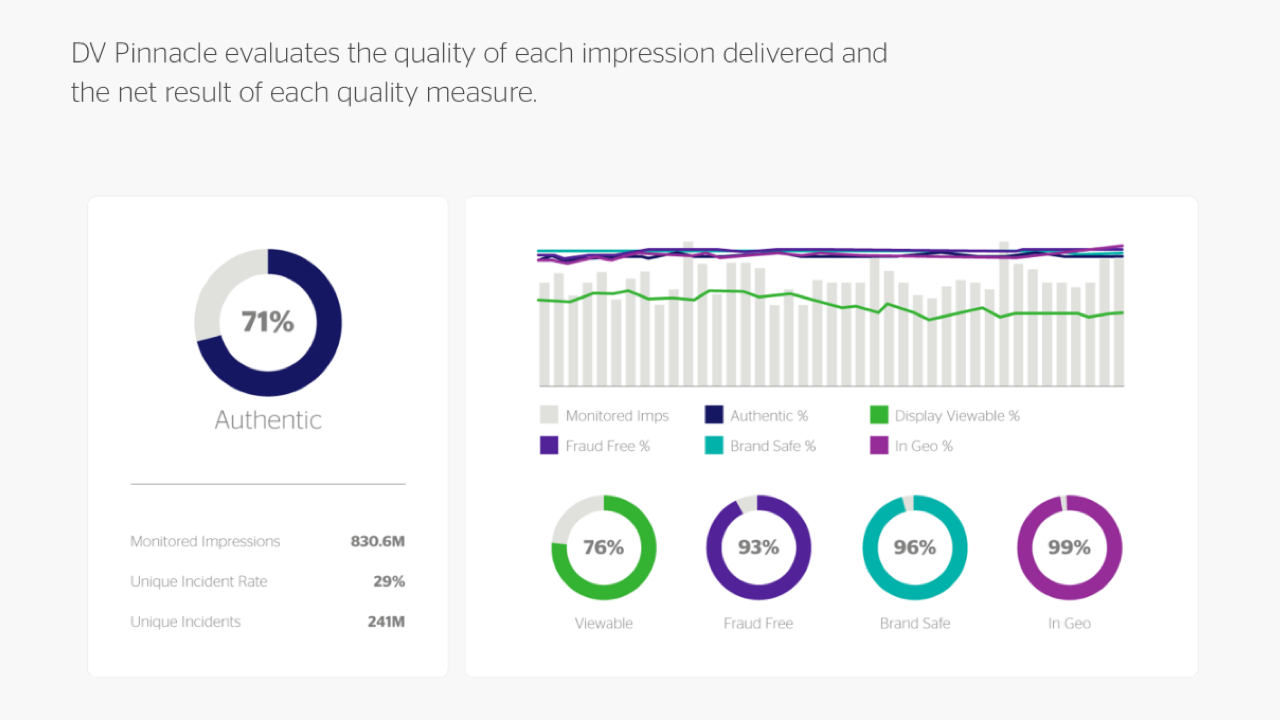

DV Pinnacle

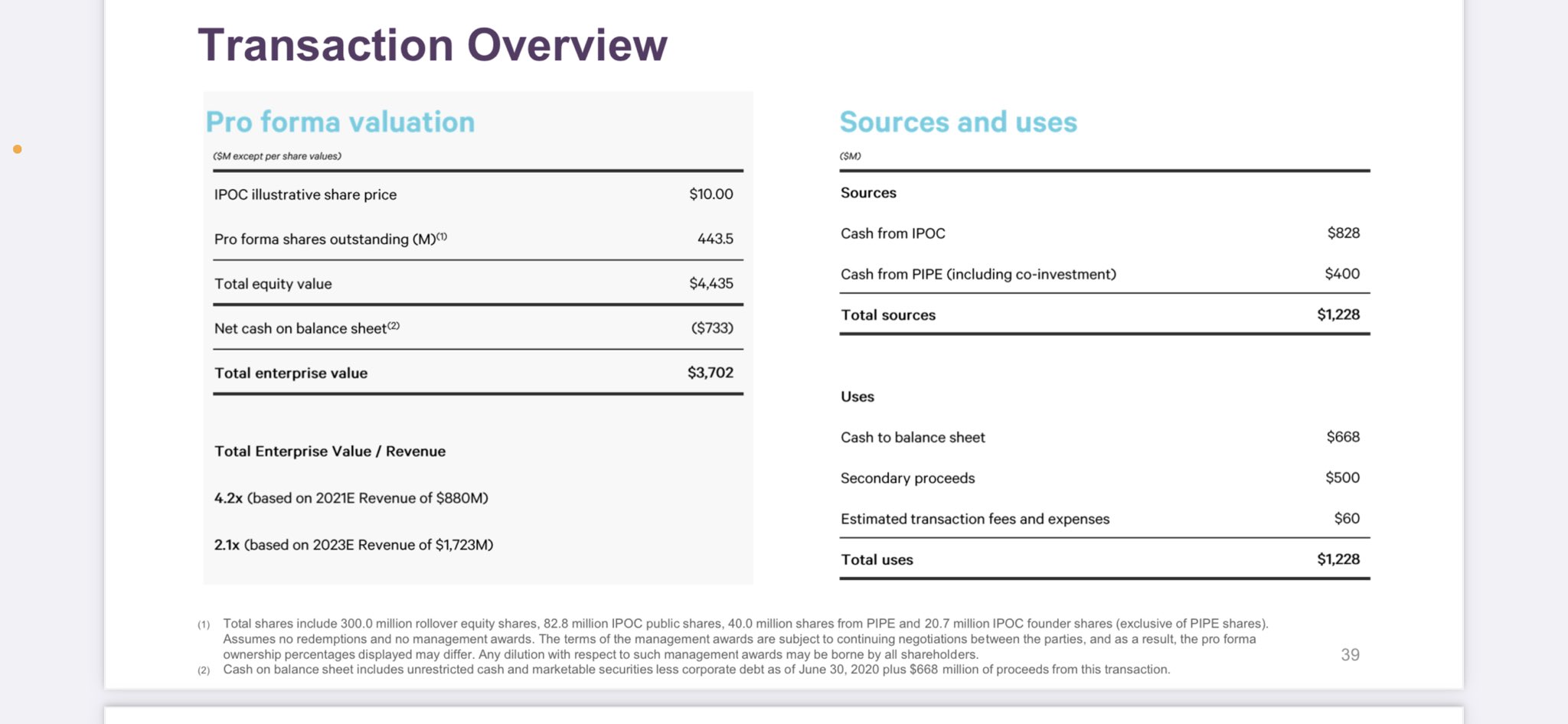

$DV is raising $330M at the IPO, selling about 13 million shares on Thursday, April 22nd, 2021 for between $24 – $27 per share, implying a Market Cap of $4B – $4.5B, with 170M shares outstanding.

$DV CEO Mark Zargoski

$DV has grown well through the pandemic, growing 34% to $244M in revenue from $183M in 2019. Is has 30% EBIDTA margins and recorded $79M in 2020. It grew from $104M in 2018 (+74% YoY).

DV Revenue Growth

$DV generates revenue in three ways:

$DV (1) Advertiser – Direct (44% of rev) Advertisers can purchase services to measure the quality and performance of ads

$DV (2) Via Demand Side or Advertiser – Programmatic (48% of rev) – Advertisers can purchase its services through programmatic platforms

$DV (3) Via Supply Side (9% of rev) – Supply Side Platforms use data analytics to validate the quality of their ad inventory and provide data to their customers.

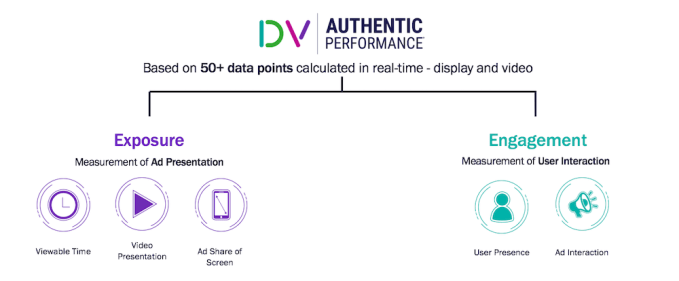

DV Exposure and Engagement

$DV raised funding from investors including Blumberg Capitaland IVP.

Providence Equity Partners acquired a majority stake in DoubleVerify in 2017, and the company most recently raised a $350 million private equity round led by Tiger Global Management in October 2020.

The company counts more than 1,000 advertisers and partners on its platform.

DV partnerships

$DV competes with companies like Improvely, Integral Ad Science and Forensiq in the analytics and ad fraud detection space.

$DV IPO pricing range implies approx. 8.5x to 10.0x on 22E revenue and 27.0x to 31.0x ‘22E EBITDA.

$DV has partnerships with $TTD (Trade Desk), $GOOG (Google), $AMZN (Amazon), $ROKU (Roku) and $FB (Facebook), $SNAP (Snap), $TWTR (Twitter) and $PINS (Pinterest).

$DV and $SNAP

I am going to pass on this opportunity for now, but keep it on my radar for a few more months. Other companies to track include $MGNI (Magnite), $PUBM (Pubmatic) and $KBNT (Kubient) in the same space.

Alight a HR, payroll, health outsourcing company, which was a part of AON was sold to Blackstone in 2017 for $4.3B. It was recording $2.0B in revenue in 2017 and today has grown to $2.6B – growing 30% over 3 years and 6% in 2020.

Today Foley Trasimene Acquisition Corp ($WPF) announced a SPAC merger to take the company public with a valuation of $7.3B

WPF Foley Trasimene Stock performance

I am going to pass on investing in this company. While the valuation is attractive (2.8X 2020 Revenue), and they have many F1000 customers as clients, the slow growth, combined with a largely low margin outsourcing business that has grown via acquisitions and still delivered little incremental value to justify the growth in EV/Rev from 2.15 in 2017 to 2.81 in 2020.

$SQSP Website-hosting service Squarespace Inc. has decided to pursue a direct listing this year (likely in June 2021).

Squarespace direct listing in 2021

Founder and Chief Executive Officer Anthony Casalena, founded Squarespace in 2004 in Baltimore, Maryland. He will continue to control the company through his 76 per cent ownership of the company’s Class B shares, which carry 10 votes each compared with one each for the Class A shares that will be listed.

Squarespace Founder and CEO Anthony Casalena

$SQSP Squarespace revenues grew 28% to $$621M in 2020 with net income of 30M, compared with $58M net income on revenue of US$485M in 2019.

$SQSP revenues have grown dramatically

$SQSP: 94% of the revenues are subscriptions and 70% are annual recurring. It has 3.7M subscribers with an ARPU (Average Revenue Per User) of $187.

They have 84% Gross Margins which grew from 81% a year ago.

Squarespace was valued at $10 billion in a March 2021 funding round, when it raised $300M. It has raised $1B to date since its first round in 2010.

Class A common stock for financial reporting purposes as a weighted-average $63.70 per share for shares granted prior to March 11, 2021.

$SQSP Squarespace competes with publicly traded rivals Wix.com Ltd ($WIX), and GoDaddy Inc., ($GDDY) among others.

Its e-commerce business had 2020 revenue of US$143 million, a 78 per cent increase over the previous year.

Squarespace fastest growing market is Commerce

$SQSP: One of Squarespace’s fastest-growing segments is Commerce, tools that help merchants design an online store to sell physical and digital goods & services. Commerce competes with Shopify ($SHOP) & Big Commerce ($BIGC).

Squarespace has a history of cash generation, including operating cash flow of $102.3 million in 2019 and $150.0 million in 2020. The company’s cash flow data explains why Squarespace is not pursuing a traditional IPO. As Squarespace can self-fund, it does not need to sell shares in its public debut.

Squarespace charges a higher monthly subscription fee for websites that use Commerce, but doesn’t take a cut of the transaction. It does, however, partner with payment processors and receives some of the revenue that Squarespace merchants generate.

Squarespace Commerce launched in 2013, GMV is still growing at 90% YoY – it hit $3.9B in 2020.

Squarespace acquired Tock for more than US$400M in March, which provides technology for online reservations, takeout and other services.

It’s backed by investors including General Atlantic, Index Ventures and Accel.

Valuation: At 28% Growth from 2020, the EV of about $10B and $621M in revenue implies a 16X LTM and at expected 25% growth in 2021 (rough estimates), they will be at $775M in revenue and 12X NTM.

Their valuation will put them in the middle of the pack for valuations among their SaaS peers and at a discount to most others growing at 25-30% if they list at $10B Market Capitalization.

Given that they are profitable, and $30M in net income, the EV/Net income is rich at 333 LTM.

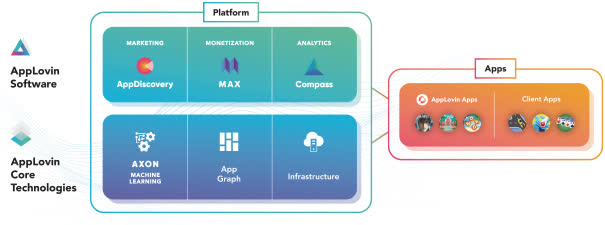

Applovin (NYSE: APP), operates both as: (1) a mobile advertising platform; and (2) a mobile video games publisher

AppLovin is a 2 pronged approach on mobile games and advertising

Background

AppLovin was founded in 2012 by Adam Foroughi, John Krystynak, and Andrew Karam in Palo Alto, California. It counts more than 410M daily active users on its platform, while its apps consist of more than 200 free-to-play mobile games, including Word Connect, Slap Kings and Bingo Story.

In July 2018, AppLovin launched a gaming arm, Lion Studios, and acquired ad bidding company, Max. In February 2021, it agreed to buy Adjust to further expand its technology platform. Adjust makes tools that measure audiences and prevent fraud in mobile advertising.

Market

Applovin appears well-positioned within the fast-growing, $189B mobile app ecosystem, operating at scale in aiding developers to manage, optimize, and analyze their marketing investments to better monetize their apps.

According to IDC, it should grow at a near 11%-CAGR over the next four years, reaching $283B in 2024. The universe of mobile game players exceeds 2B worldwide and includes 1.3M apps.

Mobile Advertising market is $189B in 2020

Industry

The mobile game monetization space is crowded with AdColony, Flurry and InMobi among its closest rivals. There are more than 4.8M mobile apps available on the Apple App Store and Google Play Store.

Mobile advertising ecosystem is very competitive

Product

Applovin’s business model focuses on optimizing the marketing and monetization of apps for both third-party developers and its own mobile games.

Applovin platform and apps

Team

Adam Foroughi is the CEO and co-founder of AppLovin. Herald Chen, is president and chief financial officer.

Andrew Karam, VP of product and co-founder while Katie Jansen, is the chief marketing officer.

Applovin Team

IPO

The AppLovin IPO raised $1.8B, giving it a market capitalization of $28B. Applovin is planning to sell up to 25M shares

Financials

2020 revenue surged by 46% to $1.45B while EBITDA grew 14% to $345M. AppLovin recorded a net loss of more than $125M last year. Cash on hand after IPO should total $2.2B ($1.7B of which is from net IPO proceeds) and there will be $1.7B of debt outstanding.

Valuation

EV/Revenue based on $1.45B in revenue and $28B in Market Cap implies 19X last twelve months and 14 Next twelve months. The stock is down 14% on IPO to $67.

Risks

The ad-tech market is highly competitive and include companies larger than Applovin including $FB and $GOOGL. It is also hard to come up with hit games that consistently engage audiences over time.

Applovin has been growing via acquisitions and integrating them over time will be a challenge. Finally, the dual class stock structure favors the current management team over shareholders.

Recommendation

I already hold $TWTR, $SNAP and $PINS besides $TTD in ad tech, so I am going to pass on $APP for now.

TuSimple (Nasdaq: $TSP), a manufacturer of autonomous semi-trucks will IPO on April 14th. The company plans to sell 33 Million shares for $36 per shares netting $1.8B for the company and valuing it at $8B.

TuSimple targets the $4T trucking market

TuSimple was founded in 2015 by Xiaodi Hou and Mo Chen in San Diego. It has offices in China and the US. It has over 500 employees and has raised over $600M in funding so far.

Market

The global truck freight market is valued at $4 Trillion. In the US, trucking moves approximately 80% of the $1T freight market by revenue, with a 3% compound annual growth rate (CAGR).

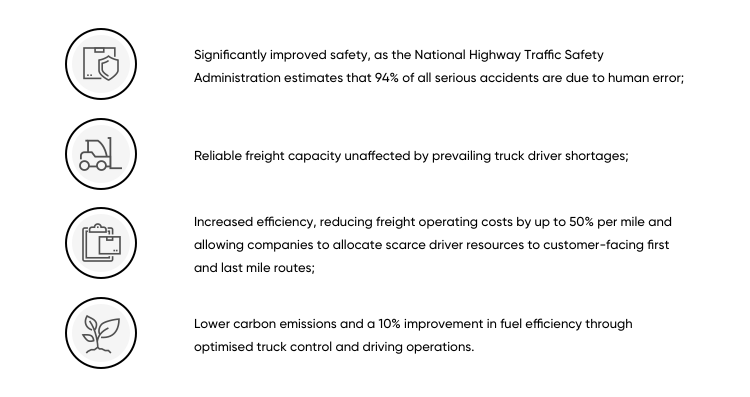

The market challenges include increasing truck accidents, lack of drivers willing to join the profession and move from Internal combustion engine to Electric Vehicles.

Long haul trucking challenges

TuSimple has reservations for about 5700 trucks and is expecting the first trucks on the road for production by 2024. It has partnered with Navistar to produce the trucks for the US market and started taking reservations in the third quarter of 2020.

The company has partnered with Volkswagen’s commercial trucking unit TRATON to expand internationally and build a truck for the European and Chinese markets.

Product

TuSimple believes vertical integration, with proprietary software and hardware manufactured by world class OEMs and components partners as well as roadside assistance and maintenance partnerships, will deliver the most reliable and first-to-market purpose-built L4 autonomous semi-trucks at scale.

The company has over 240 technology patents and over 2.8 million road-tested miles.

The company also plans to offer its TuSimple Capacity, providing Capacity-as-a-Service offerings to logistics markets based on a per mile shipping rate which management believes will be ‘significantly lower than that of human-operated semi-trucks.’

The company’s primary offerings include:

Proprietary L4 autonomous semi trucks

HD digital route mapping

TuSimple Connect cloud operations oversight system

United Parcel Service (UPS) invested in the company in 2019.

Financials

TuSimple’s revenue more than doubled in 2020 to $1.84m from $710,000 in 2019. The company’s net loss has also more than doubled as it has advanced its development, rising to $177.9m in 2020 from $84.9m in 2019 and $45m in 2018, according to the filing.

The company’s cash and cash equivalents increased to $310,815 in 2020, from $63,610 in 2019 and $98,814 in 2018.

Risks

Dual class structure (voting shares controlled by founders) is a risk. Since the company will only launch production vehicles by 2024 there is a lot of execution risk. The market for autonomous trucks is very competitive as well with Navistar, Tesla $TSLA, Volvo and many other trucking companies also investing in autonomous trucks.

Recommendation

Given the number of EV and autonomous companies that went public I will be waiting for 2 years before I jump on this.

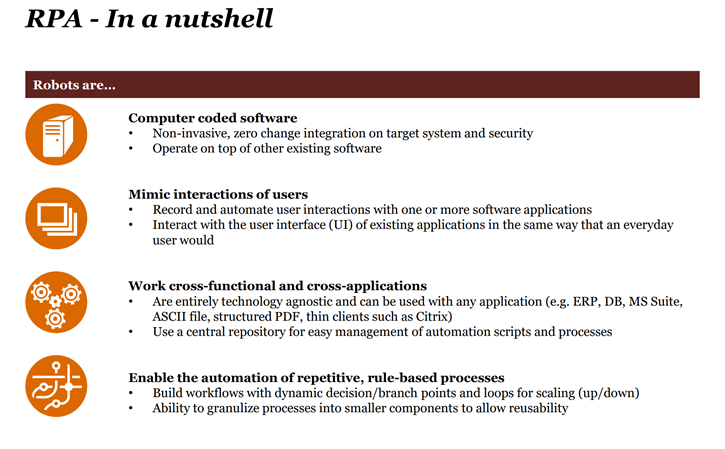

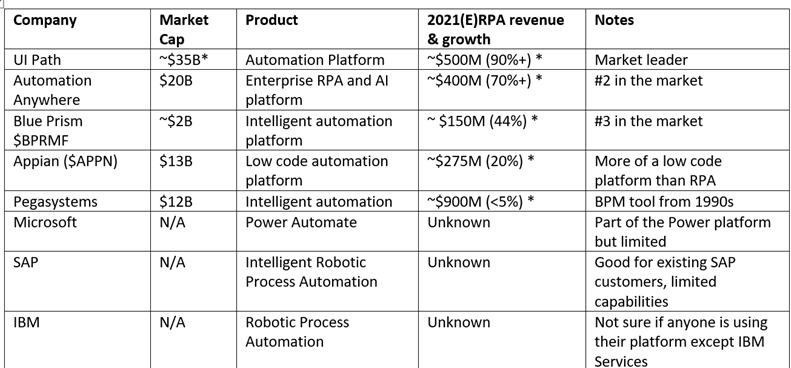

UiPath (NSADAQ $PATH) is a new Software-as-a-Service (Saas) company in the Robotic Process Automation (RPA) Space. The company will IPO on April 21st.

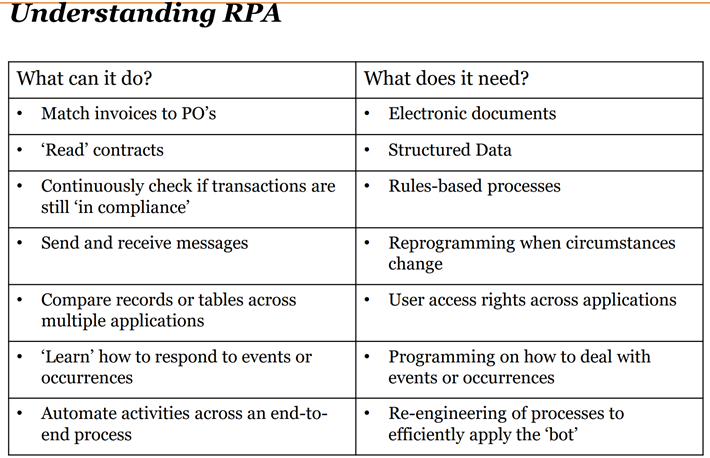

RPA allows users to automate tasks and mimic interactions with other software solutions. For example if a finance accounts payable professional wants to reconcile invoices (obtained via one tool) with payables (via an ERP solution), they can do this at scale with RPA.

RPA allows you to automate rule-based repetitive processes

Use cases for RPA include invoice processing & contract automation

UI Path was founded in 2005 in Romania by Daniel Dines & Marius Trica, and raised seed funding in 2015. The company has about 3000 employees.

Market

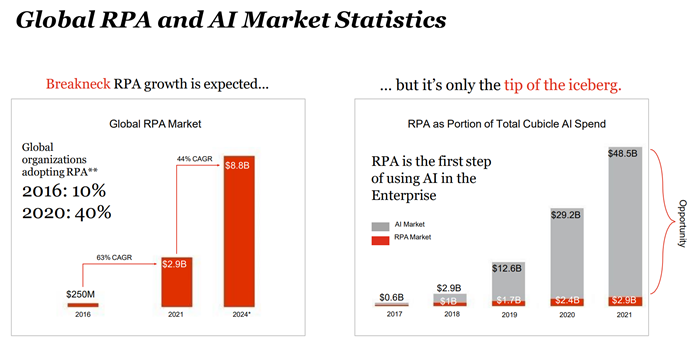

The RPA space is about $2.5B annual and is expected to grow to $8B by 2024 and over $30B by 2030.

RPA market is expected to be $30B by 2030

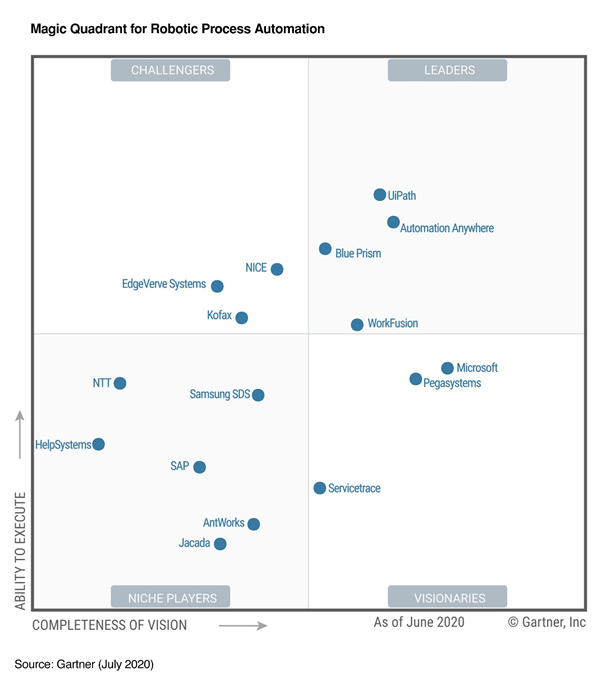

There are multiple competitors in the market including Automation Anywhere, Microsoft, SAP, Blue Prism and others, but UiPath is the leader in terms of revenue and growth.

RPA is a competitive space, but UiPath is a leader

Financials and Operating metrics

UiPath has grown 81% in 2020 to $608 Million in revenue, bigger than Snowflake (SNOW) and smaller than Unity (U). For the SaaS metric “Rule of 40” they are at 85% implying strong fundamentals. Their Gross margins were 90%, 24% non-GAAP margins and 14% Operating margins.

UiPath sells annual subscriptions of licensed software (57% of revenue), support (38% of revenue) and training (5% of revenue).

Their operating metrics are terrific as well with 145% Dollar based net retention rate.

Customers

Over 6500 customers worldwide use UiPath, 63% of Fortune 500 companies including Adobe, Uber, Chevron and Chiptole.

UiPath is a leader in the Gartner Magic Quadrant for RPA

IPO Overview

UiPath plans to sell 21.2 Million shares, between $43 and $50 , implying a market capitazation of $25 Billion to $27B. The company has raised over $2B in private markets so far, and most recently raised $750 M at $35B valuation in Feb 2021.

Valuation

For 2021 UiPath expects to record about $900M to $1.2B (my estimates), growing at over 50% – 90% annually which would imply a 25X Enterprise value to 2021 Revenue multiple. This would land them at the lower end of valuation for comapnies growing at over 50% – including CrowdStrike, ZScaler, Snowflake and CloudFlare.

UiPath trades as a discount to peers with similar growth

Risks

UiPath will have a limited operating history as a public company, and had its top 10 customers account for a lot more than 10% of their revenue – customer concentration is a risk. The founders have a significant control of the company via preferential shares as well.

Recommendation

I am going to acquire shares and average my purchases over the next few quarter. This company could be the next large, fast-growing, high-margin business.

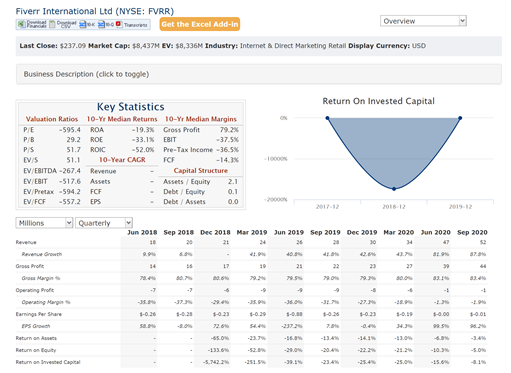

Fiverr (FVRR) is an online marketplace for freelance work. Founded in 2010, based in Israel, the company is currently priced at $240 (Jan 21 2020), with a Market Cap of $8.44B. The company is at an inflection point in terms of growth and revenue, recording $163M (+80% YoY) in Trailing Twelve Months (TTM) revenue. It is expected to grow at excess of 70% over 2021.

Risks include a rich valuation at 51X Next Twelve Months (NTM) revenue, the tail winds from work from home (due to Covid) trailing off – unlikely in my opinion, and a distraction in management bandwidth as the focus shifts to expansion in categories, new geographies and products.

I am going to accumulate shares in $FVRR over the next few months, expecting it to be a core (top 15) holding for 3-5 years.

Fiverr stock has been an excellent performer in 2020 with 900% growth

What is freelance work?

Essentially, a freelance job is one where a person works for themselves, rather than for a company. While freelancers do take on contract work for companies and organizations, they are ultimately self-employed.

Freelancers are responsible for all sorts of things that traditional employees are not, such as setting their work hours, keeping track of time spent on different projects, billing clients, and paying their own employment and business taxes. Freelancers are not considered “employees” by the companies they work for, but rather “contractors.”

How many people freelance?

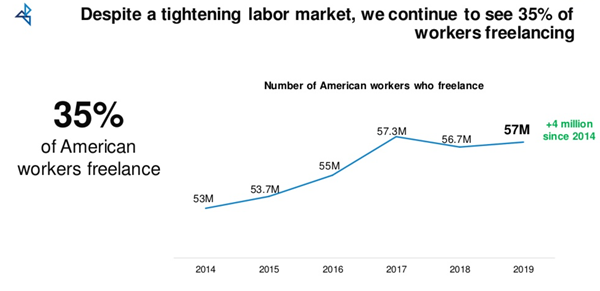

More than 30% of Americans freelance either full-time or part-time

More than one-third of the American workforce freelance amid the Covid-19 pandemic, contributing $1.2 trillion to the U.S. economy.

This was a 22% increase since 2019 and it was fueled in part by an influx of younger, highly skilled professionals seeking flexible alternatives to traditional employment. 59 million Americans performed freelance work in 2020.

Freelancer worker growth continued to go higher even as unemployment was lower

Why are the number of freelancers growing?

Freelancers like the flexibility of time and hours, the ability to earn an income on the side, and the capability to monetize their skill.

Amid a tough job market for recent college graduates, half of the Gen Z workforce (age 18-22) have freelanced in the past year, and of those, more than a third (36%) started since the onset of Covid-19.

The share of independent professionals who earn a living freelancing full-time has increased 8 percentage points to 36% since 2019. 59% of freelancers have participated in skills training in the last six months vs. 36% of non-freelancers.

Benefits of freelancing

There is a burst in demand for people to support customer services as well as ecommerce development, web and mobile design.

75% say they earn the same or more in pay than when they had a traditional employer.

Society’s perception about freelance is also changing. Seventy-one percent of freelancers say perceptions of freelancing as a career are becoming more positive, the survey revealed.

Meanwhile, 67% of full-time freelancers say that freelancing has prepared them to cope with the uncertainty of the coronavirus pandemic better than those in traditional jobs.

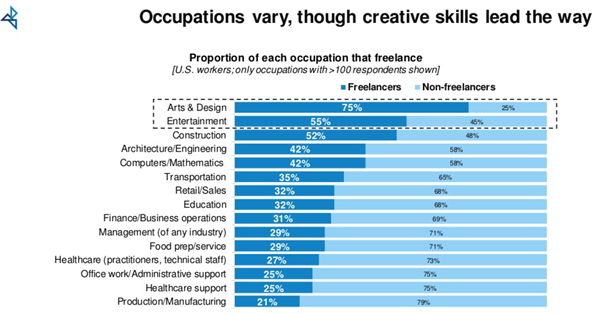

What categories of work are being freelanced?

Freelance jobs most in demand today are in computers (Graphic design, Web development) /mathematics (data analysis), and in finance (accounting) /business operations (social media marketing, administration).

Design, Media (video production) are most likely candidates for online freelancing

Even before Covid-19, 26% of freelancers worked entirely remote and 46% worked remotely more than half the time. Freelancers doing skilled services earn a median rate of $28 an hour.

The computer related skills that are the most freelanced jobs

How big is the market? Who does freelancing?

Freelancing income exceeds $1 trillion, almost 5% of the United States’ GDP.

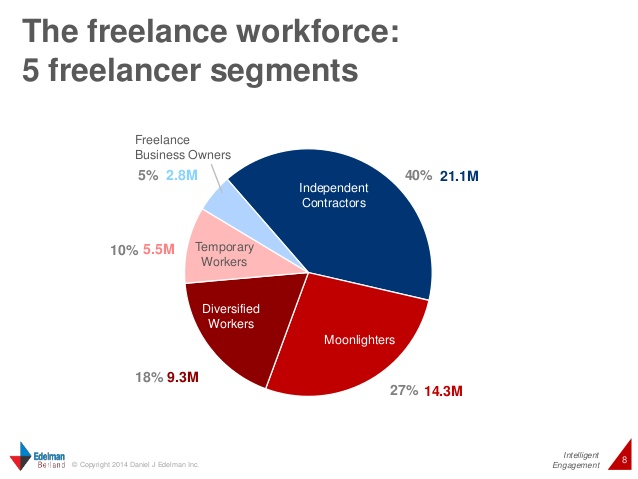

Most freelancers are indepdent contractors

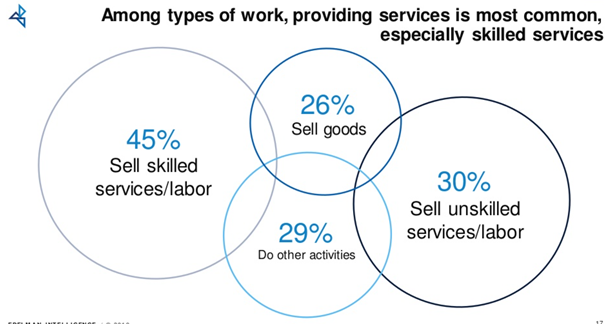

Freelancers offer skilled services

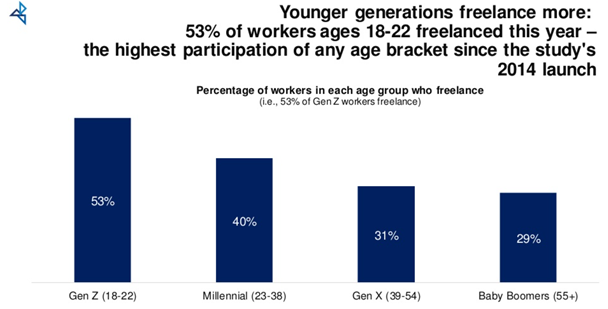

Every generation had more than 1 in 4 workers who freelanced in the past year. The ascent of freelancing is clear in generational results:

29% of Baby Boomer workers (ages 55+) freelanced,

31% of Gen X workers freelanced (ages 39-54),

40% of Millennial workers (ages 23-38) freelanced and

53% of Gen Z workers (ages 18-22) freelance

Younger generation folks are more likely to freelance

What are the market dynamics?

Of the 57 Million freelancers, over 5 million are already finding work purely online via platforms such as Fiverr, Upwork, Freelancer and over 20 other websites. Specialized marketplace such as TopTal (Top talent) for developers and Behance for designers also exist.

Most freelancers find that small & micro business tend to use freelancers more than large business. In this kind of marketplace there are a lot more sellers (supply) and harder for them to find buyers (aggregate demand).

For long services feel into 2 major formats – a) Time and Materials (quoted) or b) Fixed Bid.

In a Time and Materials project the risk is on the buyer to define scope, and the seller gets paid a fixed fee per hour.

In Fixed Bid projects the risk is on the seller to narrow the scope and the seller gets paid a fixed fee for the project.

Since both these formats introduce risk, there is a need to “productize” services. A fixed deliverable at a fixed price.

That was Fiverr’s insight that led them to start the company.

Who is Fiverr?

Fiverr was founded by Micha Kaufman and Shai Wininger in Israel and was launched in February 2010. The founders came up with the concept of a marketplace that would provide a two-sided platform for people to buy and sell a variety of digital services typically offered by freelance contractors.

Fiverr Founders

Services offered on the site include writing, translation, graphic design, video editing and programming. Fiverr’s services start at US$5 and can go up to thousands of dollars with gig extras. Each service offered is called a “gig”.

Freelancers – merchants, entrepreneurs, contractors in more than 200 countries use Fiverr to sell their skills, and talent. They can offer “Gigs”, ranging from web design, logo creation and market research, to personal greetings and video animation. Customers can then buy these jobs for services they need rendered. Fiverr helps sellers collect payments, promote their services, manage orders, exchange files and communicate with buyers.

In an interview with NFX, Shai said the $5 price point was a gimmick.

“It also created a single price point so that we didn’t have to deal with multiple price points based on quality. We knew that over time we were going to extend that, but it was all about simplicity and removing that friction and inefficiency using software. That was it.“

Founder of Fiverr

Over the next few years they raised over $150M from blue chip Silicon Valley investors such as Accel and Bessemer Ventures. Fiverr went public in 2019.

Who are the competitors?

The freelance market is very fragmented, diverse and competitive. Over 50 marketplaces exist such as Upwork, Freelancer.com, Insolvo.com, FlexJobs.com, SolidGigs.co, TopTal.com, PeoplePerHour.com and Guru.com.

There are no official market share numbers, but since the market is very large ($1.3 Trillion global), one can safely assume that Fiverr has low market share ($160 Million in 2020 revenue) and the penetration is negligible. That means the opportunity to grow is tremendous.

Fiverr has over 7 million users.

Upwork has over 17 million users.

Freelancer has over 31 million users.

What products does Fiverr offer?

The main Fiverr platform has multiple capabilities.

A catalog infrastructure to support over 250 categories of services from voice over to logo design.

A proprietary liquidity management system, putting 9 years of transaction and behavioral data to use, allowing us to match buyers and sellers at the gig level in a personalized fashion.

A comprehensive set of rating and reputation, scoring, and leveling systems to improve the quality of gigs and sellers on the platform.

Features and tools to provide value to our buyers and sellers in areas such as payments, communication, collaboration, and automation

Fiverr products and services

Fiverr Studios: Allows freelancers to collaborate and offer combined services for a project

Fiverr Discover: a beautiful destination site showcasing designs sellers made for our buyers through the platform. Customers use this site to look for inspiration for their projects on hand.

Learn: allows freelancers to keep upgrading their skills

ClearVoice: A specialized capability for hiring voice over artists

And.co: An acquisition of a company providing tools and automation capabilities (back office) for freelancers.

Fiverr Logo Maker, bringing the power of artificial intelligence to Fiverr’s best creative talent. Allows graphic designers on the platform to monetize their existing designs, deliver their work faster, and serve more customers.

Fiverr’s Choice: A chosen set of freelancers for each type of gig. This is very useful for high value buyers to narrow their selection.

Promoted listings. They have been testing the product internally for a while, and we are planning to launch the beta version in April 2021. This will be the first time they give sellers a tool to proactively promote themselves on our platform.

How is Fiverr different than competitors? What is their moat?

The most important thing to remember is the insight “Productized Services”.

In this market, buyers find it takes too long (this is from personal experience) to vet suppliers, look at bids, then start the work.

If the work can be broken up into products that can each be purchased as a SKU that makes the purchasing process frictionless.

As opposed to competitors who list “freelancers”, Fiverr changes the game and lists “products” which you can purchase – with a defined outcome. These translate to Gigs for freelancers.

This makes it easy to compare 2 products instead of 2 freelancers who you might not know anything about.

That creates the Fiverr flywheel.

Productized services at the start of the flywheel

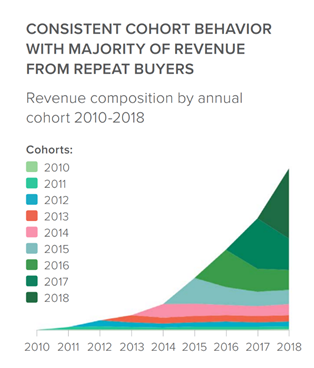

That flywheel results in consistent growth in buyer and seller cohorts.

Revenue by annual cohort of buyers

The revenue stickiness among sellers creates a strong moat.

While sellers sell on multiple platforms, they can scale “faster” on Fiverr over UpWork, where they have to bid for each project.

Here is an example from a seller:

The major difference between popular freelance marketplaces like Upwork and Fiverr is the process of working with clients.

Working with clients on Upwork means constantly pitching for new jobs. So new work doesn’t happen in the background without your input — you have to be proactively on the hunt for new work when you want it.

Fiverr is a completely different story.

With Fiverr, you essentially productize your service via Gigs.

Each Gig describes a specific deliverable you will provide in exchange for a set price, starting with the words, “I will…”

But the best part about Fiverr is that because of the way Gigs are set up, clients are empowered to make purchases without even talking to you.

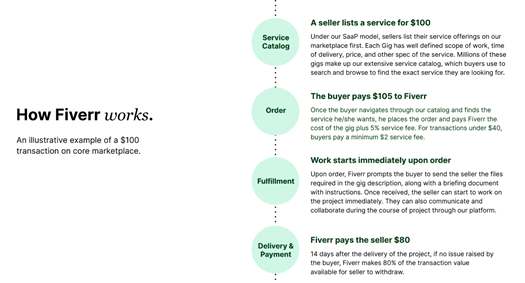

How does Fiverr make money?

Sellers pay a 20% transaction fee and buyers a 5% fee

Both sellers (20%) and buyers (5%) pay Fiverr a commission for transacting on the platform.

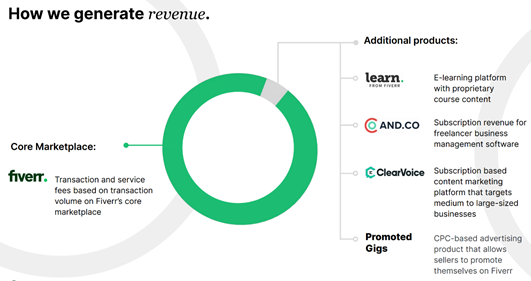

Core marketplace revenues made up over 90% of revenue

How do the financials look?

Fiverr has produced phenomenal results post going public

In one word – tremendous. That’s the main reason the stock price is up 900% in 2020. Growth is accelerating, and I dont believe this is going to slow anytime soon.

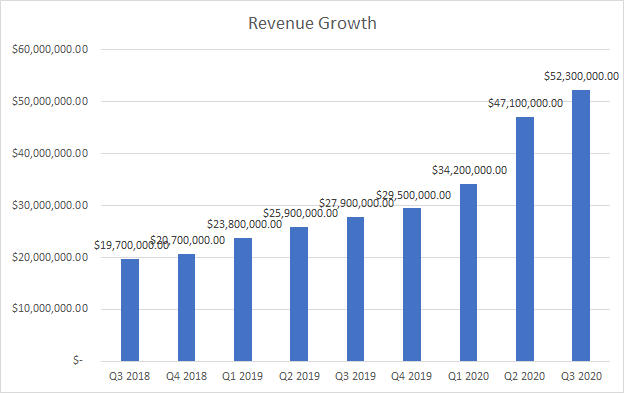

Revenue Growth has been stellar

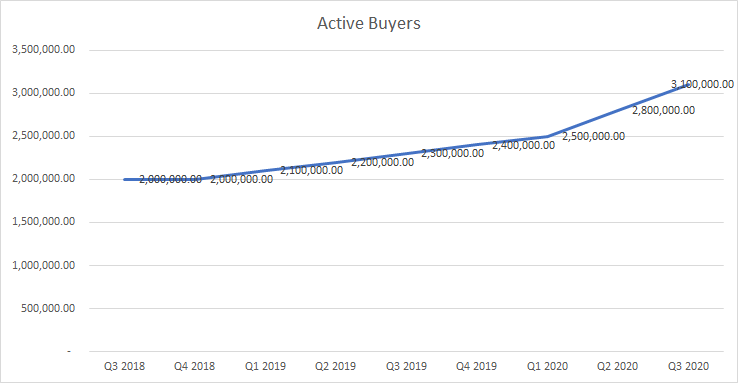

There are over 3 million active buyers and growing.

Buyers drive growth, which has been the cornerstone of the marketplace growth

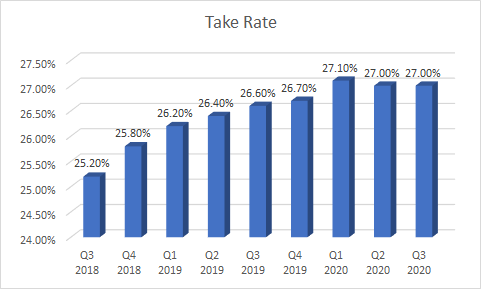

The take rate (commissions) have been growing as well.

Take rate growth

What about their competitor UpWork? Are they are “better value”?

UpWork financials show slower growth

UpWork is the biggest large competitor to Fiverr, but they are not growing as fast (18% vs 80%).

I attribute this to seller efficiency with Fiverr and that comes from productized services. The more Fiverr helps sellers productize their services into SKU the easier it becomes for buyers to buy quickly. It does create lack of differentiation for sellers, however, who now have to rely on more reviews, ratings – which is a good incentive.

How big can this become?

There are 3 future directions that Fiverr can take, which I believe will take them to over $1B – $10 Billion in revenues.

They become the platform for “all” knowledge work – “LinkedIn with transactions“. You want a designer, you can hire one at Fiverr and see their prior work.

They become the complete automation platform for freelancers, helping them grow into small businesses – “Square ($SQ) for freelancers.

They become the “Amazon for services” providing buyers and sellers the ability to catalog, purchase, deliver and buy services.

Really low estimates from major analysts is a setup for Fiverr I believe.

What about valuation? Is this not too rich?

At 51X LTM revenue, this is among the richest < $10 Billion market cap company. There are others such as Shopify and Zoom that are richer, but they have Billions in revenue.

I am paying for growth and betting that they can productize more services.

Among marketplace companies, Fiverr (if they execute to their 2021 plan, which they have consistently done in the last 2 years) is the fastest growing.

#

Ticker

Rev Growth

EV/Rev

EV/EBITDA

1

FVRR

80%

27.8

0

2

CVNA

51%

5.3

0

3

RDFN

49%

5.4

0

4

DKNG

46%

21

0

5

Z

44%

6.3

0

6

UBER

42%

6

0

7

TRIP

41%

4.5

59

8

ABNB

37%

21

0

9

LYFT

36%

4.3

0

10

BKNG

34%

9.6

48

11

SHOP

33%

36

35

12

DMYD

31%

12.53

68

What does the institutional buying look like?

Institutional buying has been strong and over 200 funds own Fiverr. While that is not “tremendous” it is growing.

Institutional buying for Fiverr

What is the one year price target? What about beyond that?

Assuming the 70%+ growth rate this year $FVRR should be at over $275 Million in revenue, which gives it a $14 Billion valuation at current NTM valuation at 50.

I think valuations will contract.

It is hard to predict how much they will contract by, but it can support 30X EV/NTM at which case it will be a $10 Billion Market Cap company or 20% above its current price of $240 or $288 per share by Dec 2021.

Over the next 5 years (2020 – 2025) I can easily see FVRR being at over $1.5 Billion in revenue and growing to over $40 B in Market Cap.

What are the risks?

There are 3 major risks:

Valuation contraction from currently very rich position. If 50X EV/LTM is high (which it is), I can see this being only 10-20X in a down (bear) market. A reasonable valuation is 25X based on other multiples of fast growing companies, but that means a 50% haircut from current stock price.

Fiverr saw tremendous growth during Covid. I am not sure that was supply led since more people worked from home, but demand had to be there for transaction liquidity. I worry that post Covid the buyers will go back to using previous (local) providers instead of online. 90% of the current freelance market is offline.

As Fiverr tries to expand into new categories and markets there is a chance of dilution of the management team bandwidth. This is the #1 cause of issues for most growing companies in my opinion. They tend to bite off more than they can chew.

In 2015 Fiverr settled a lawsuit where Amazon complained it helped sellers on Amazon marketplace get fake reviews from various “sellers” on Fiverr. They have since discontinued that service, but that creates an opportunity for freelancers from various places to productize poor quality and inherently bad services.

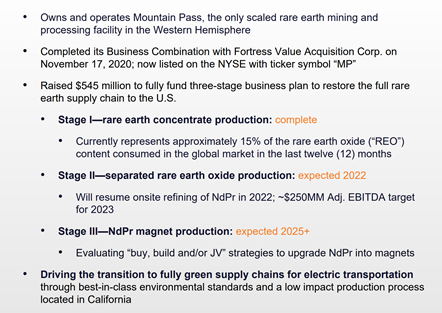

This deep dive is on Rare Earth Elements (REE) with a focus on MP Materials ($MP) a company that recently went public via SPAC. This is fascinating topic to me and I have barely scratched the surface in this subject with this post. I recommend you read many of the references below.

I hold $MP (I currently have some shares I bought at $34). I will add to my position if it drops below $24.3 (if market or the stock corrects) or goes above $40 OR

If the next quarter of earnings from MP shows faster growth than they projected (greater than 75% YoY growth in Q4 2020). Earnings date is Feb 23rd 2021.

Volume on the stock has been building in the new year with supports at $28, $24, $19 and $16 price ranges.

MP Materials stock performance with horizontal lines on indicated support prices <Trading View>

For FY 2021 MP expects $171M in revenue and $82M in adjusted EBITDA. The company was valued at at $1.4B when they went public via SPAC in July 2020 and are valued at over 3X that amount (Jan 2021).

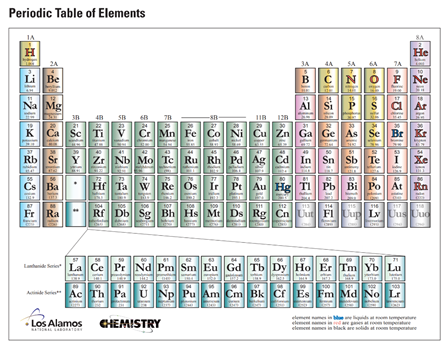

What are rare earth elements (REE)?

The rare-earth elements (REEs) are 15 elements that range in atomic number from 57 (lanthanum) to 71 (lutetium); they are commonly referred to as the “lanthanides.”

Rare Earth Elements (bottom of chart)

Although REEs are not rare in terms of average crustal abundance, concentrated deposits of REEs are limited in number.

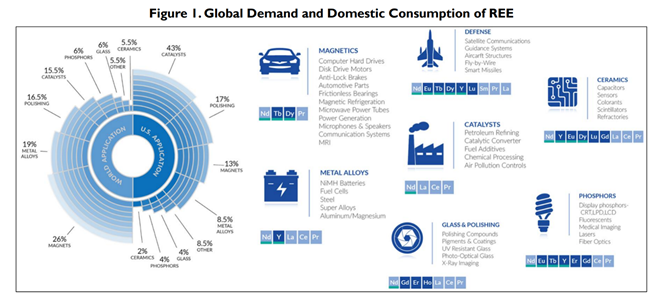

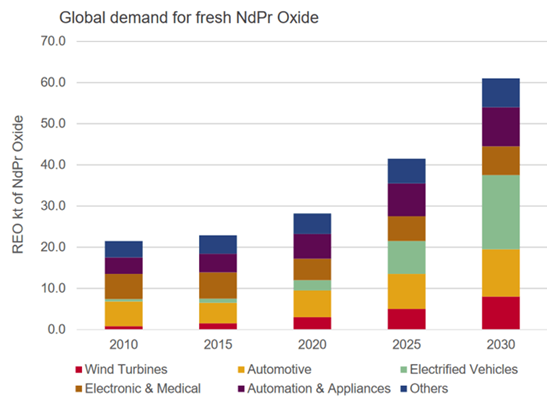

Rare earths are used in the renewable energy technologies such as wind turbines, batteries, catalysts, and electric cars.

Why are REE suddenly in the news?

Rare earth availability is undergoing a temporary decline due mainly to quotas being imposed by the Chinese government on export and action taken against illegal mining operations.

The reduction in availability coupled with increasing demand has led to increased prices for rare earths. Although the prices have come down recently, this situation is likely to be volatile until material becomes available from new sources or formerly closed mines are reopened.

Keep this in mind as you read this piece. Like many commodities such as oil, there is tight, restricted supply and increasing demand.

Although the number of identified deposits in the world is close to a thousand, there are only a handful of actual operating mines.

Prominent currently operating mines are a) Bayan Obo in China, b) Mountain Pass in the US and recently opened c) Mount Weld in Australia.

US , Australia and China – Rare earths are in these countries.

REE are used in multiple applications and technologies

Are all REE the same?

Rare earths are further divided into

a) light rare earth elements (LREE) and

b) heavy rare earth elements (HREE) with the divide falling between the unpaired and paired electrons in the 4f shell.

LREE includes from lanthanum to europium and includes scandium. The HREEs include from gadolinium to lutetium and includes yttrium.

Present technologies for electric vehicles and wind turbines rely heavily on dysprosium (Dy) and neodymium (Nd) for rare-earth magnets.

It is anticipated that recycling and recovery will assist to satisfy the demand for rare earth element, but its contribution is currently low (i.e., less than 1%) and will pose significant challenge in terms of collection, processing and their recovery due low concentration of REE in products.

According to the Unites States Geological Survey (USGS), world resources are enough to meet foreseeable demand but world production falls short of meeting current demand.

Which rare earths matter? How are they obtained?

Rare earth containing minerals (or ores) are usually dominated by either HREEs or LREEs.

Minerals containing predominantly yttrium and the HREEs include gadolinite, xenotime, samarskite, euxenite, fergusonite, yttrotantalite, yttrotungstite, yttrialite.

Minerals containing predominantly LREEs include bastnasite, monazite, allanite, loparite, ancylite, parasite, lanthanite, chevinite, cerite, stillwellite, britholite, fluocerite and cerianite.

However, commercially operating mines around the world mainly extract bastnasite, monazite and xenotime ores.

So, you need to mine the ore and then “obtain” rare earth elements by extracting them via multiple processes.

For a typical open pit, mine, the approach is similar to other mining operations which involve

a) removal of overburden,

b) mining,

c) milling,

d) crushingandgrinding,

e) separation or concentration

The mining process is pretty complicated to get from ore to REE

Why is this a big issue?

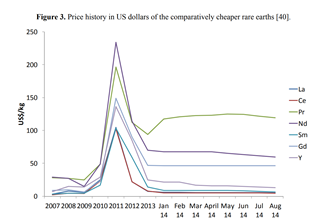

Between 2010 and 2012 the Chinese government put strict export quotas on their rare earth minerals and semi processed rare earth products. That caused a huge spike in prices as you can see below.

Prices shot up when China imposed restrictions on exports

The quotas reduced the output by nearly 60% compared to the 2008. These quotas created a gap between demand and supply and large increases in the prices of the rare earths.

At this point, the Chinese have around 55% of all known rare earth deposits and control 95% of world supply through integrated mining, refining and supply chains.

Australia, China and US have enough distribution (and Malaysia) of REE deposits

So why now in 2021? And what is the connection to Electric Vehicles?

The REE are used in multiple applications but most acutely in batteries for EVs

Rare earth magnets (Nd, Pr, Sm and Dy) are particularly needed for alternative energies.

These will find widespread application in wind turbines, the auto industry (electric and hybrid cars) and defense industry (i.e., missile guidance systems).

Rare earth containing (Er) glasses are important for fiber optical amplifiers required in high-speed optical communication networks as well.

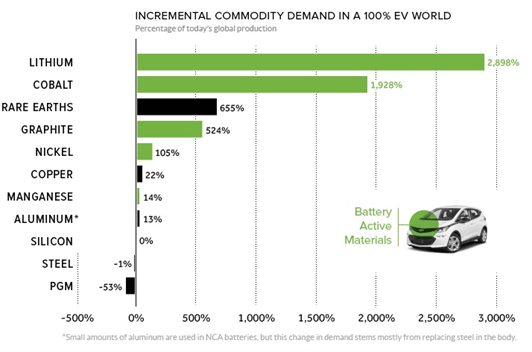

Since there has been a boom in Electric vehicles, the need for REE in EV (batteries) is significant.

EV batteries need a lot of HREE

The rare earth’s sector in the US got a significant boost as Senator Ted Cruz lodged a bill with the US Senate to support the US rare earths industry. MP Materials has spent significant money building a lobbying arm to support their cause.

At this time, about 80%+ of rare earths come from China.

China’s major rare earth mine is Baiyun Obo, located in Inner Mongolia. It is the world’s largest known REE deposit. Reserves are estimated at more than 40 million tons of REE minerals grading at 3-5.4% REE (70% of world’s known REE reserves).

High prices also caused manufacturers to do three things:

1) seek ways to reduce the amount of rare earth elements needed to produce each of their products;

2) seek alternative materials to use in place of rare earth elements;

3) develop alternative products that do not require rare earth elements

Those may still happen for EV batteries, but right now REE are the best option.

This seems like a mining problem. Where is the opportunity for growth?

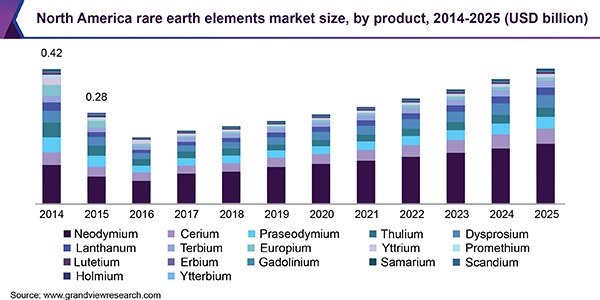

The global rare earth elements market size was valued at US $2.80 billion in 2018 and is estimated to witness a CAGR of 10.4% from 2019 to 2025. It will be a $5.2 Billion market by 2025.

This market is growing and is being driven by EV batteries

Cerium, neodymium, lanthanum, praseodymium, yttrium, and dysprosium are the most commonly used rare earth elements. The market is driven by the increasing demand for these products in the manufacturing of magnets & catalysts for the automotive industry.

Cerium is widely used as a catalyst in catalytic converters of motor vehicles while neodymium & praseodymium are used in the production of batteries for electric vehicles.

As per the International Energy Agency, the global stock of electric cars was over 5 million in 2018 with more than a 63% increase from 2017. According to JP Morgan there will be 8-10 Million EVs by 2025.

Rising demand for electric vehicles to reduce CO2 emissions is expected to propel the use of permanent magnets in the production of batteries. Neodymium and praseodymium based rare earth permanent magnets are majorly used in the manufacturing of batteries.

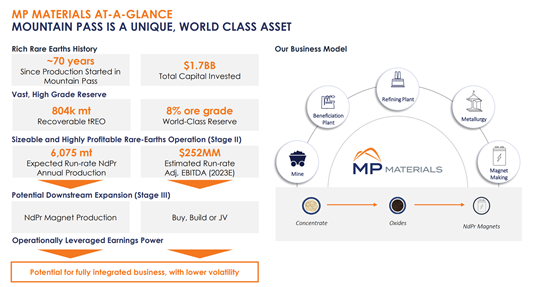

Who is MP Materials?

MP Materials was founded in 2017 and they went public via SPAC (announced July 2020) at a valuation of $1.5 Billion (currently valued at nearly $5 Billion).

MP Materials Mining Operations

Mountain Pass in CA had a mining operation that was forced to shut in 2002 in part because it was squeezed out by China’s low prices. In 2015, its owner went bankrupt. MP Materials acquired the mine, and slowly restarted operations.

MP Materials currently has to send much of its rare earth concentrates (ores) to China for processing because it doesn’t have the capacity to do so itself. The company hopes to process and refine its own rare earths by 2022, so as to keep the entire supply chain on US soil.

Why MP Materials?

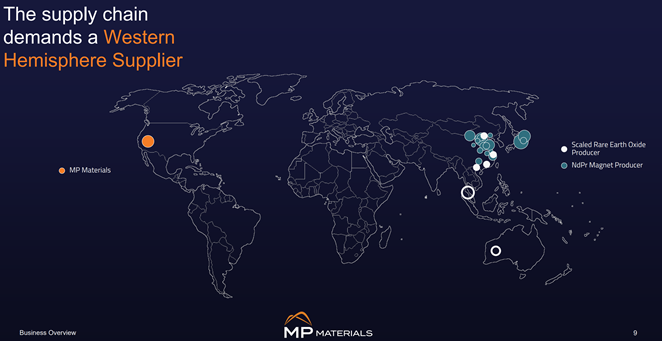

MP Materials owns and operates Mountain Pass, the only rare earth mining and processing site in North America.

MP Materials extracts 50,000 tons of rare earth concentrate each year but still relies on China to process the materials. However, MP Materials plans to have its own Heavy Rare Earth separation facility and has been awarded partial US Defense funding for such a facility at their Mountain Pass Mine in California. This is a big moat. They dont give these out to every company.

MP Materials say they will kick-start their own processing operation by the end of 2020 and produce about 5,000 tonnes of two popular types of rare earths annually: Neodymium (Nd) and Praseodymium (Pr).

What is the moat for MP materials?

MP is the only existing domestic (US) extractor of REEs. Their Mountain Pass mine is indeed the sole American rare earths source currently in operation.

MP has been operating it since 2017, and produces a rare earth concentrate product that amounts to in excess of 36,000 tons of rare earth oxide equivalent per year (approximately 15% of world rare earth market demand).

The company currently has some 200 employees working at the Mountain Pass mine.

They are the 2nd largest producer outside China and profitable.

MP has good moats and the cash inflow will make their moat stronger

Who is the competition?

In China there are several competitors, but outside China, Texas Mineral Resources and Lynas (Australia) are the only other competitors.

$TMRC (Texas Mineral Resources Corp).

TMRC’s flagship Round Top Project is in Hudspeth County, Texas. The project is dominated by rhyolite ore enriched in rare earth elements (REEs), especially heavy rare earths (HREEs), as well as several other critical elements including lithium. It is reported that the Project “offers a 130-year supply of the critical minerals.”

TMRC has a development agreement with USA Rare Earth LLC (“USA Rare Earth”) whereby the partner will earn up to 70% interest in the Round Top project once its $10 million investment leads to a Bankable Feasibility Study. Thereafter, USA Rare Earth can earn an additional 10% interest with a $3 million cash payment to TMRC.

$LYSCF (Lynas) Australia

Lynas is NOT a US rare earths miner; however, it recently won partial funding from the US defense for a heavy rare earths processing plant in Texas USA. Further funding along with their project partner (Blue Line Corp.) looks very likely. Lynas plans to ship rare earths from its mine in Western Australia for final processing at the Texas facility.

China based competitors for MP

What are the risks?

The biggest risk is China controls 80%+ of all production which dictates prices. They can (like they did before) reduce prices to such a low level that MP becomes unprofitable and can go bankrupt – similar to their predecessor.

The second risk is that this is a capital intensive business. Although MP is profitable now, and have enough cash (They got $545M from the proceeds of the SPAC) to get them to processing the ore, they depend on China for a few more years to manage the processing. They may even depend on them for longer after that.

The third risk is MP has a Chinese investor who owns over 10% of the company. Shenghe Resources Holdings owns about 10%, which makes them vulnerable to certain defense contracts.

How do the financials look?

The projections are strong, and growth forecasts are excellent – if they execute and if prices for REE remain stable. China has incentive to keep prices stable, I believe, but we are in uncharted territory.

If you think OPEC the oil cartel is bad, this is worse since one country controls prices.

They estimate to have $415M in revenue by 2023, and if that is the case, they will have a significant part of a large market and are expected to grow at 50%+ CAGR.

The growth quickens in 2022 (70%+) and slows again in 2023 (18%).

What is the 1 year price target?

The valuation is rich now (it was reasonable in July 2020) at 48X LTM (2020, Last Twelve Months) revenue and 29X NTM (2021, Next Twelve Months) revenue.

This is a narrative driven investment, not by the financial metrics.

You have to believe the US & the rest of the world (sans China) has deep interest in seeing MP succeed for a part of their supply chain.

You have to believe that MP will eventually get to processing ore in the US as opposed to sending it to China for processing.

You have to believe that the environmental lobby won’t find a shut down this mining operation.

If you believe all those things, you can see this being not a multiple of revenue but a core part of many EV and innovation portfolios. It could get there as a “picks and shovels” play on EV ETFs.

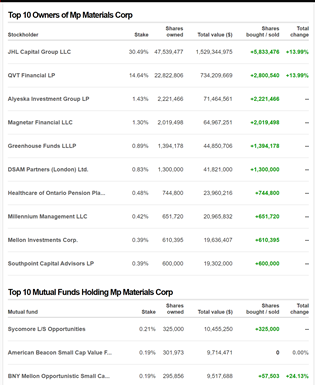

I am not sure what a good price target is, but this stock has been building momentum and has good institutional buying (see below).

I can see the stock going up 100% in 2021 thanks to current traction, but I can also see a deep pullback before it gains momentum.

Should this be a core part of the portfolio for more than just patriotic reasons?

Yes, the growth is tremendous and the moats are significant.

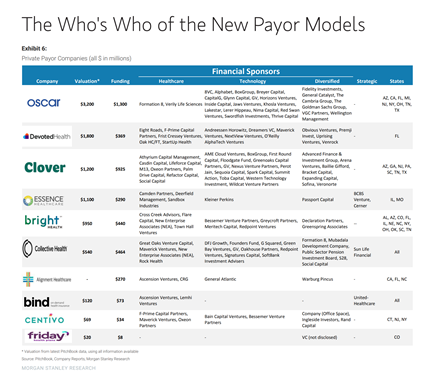

This post is a deep dive on Medicare Advantage plans and a look at one of the companies that recently went public Clover Health ($CLOV) valued at $1.9B (Jan 17 2020). I will try to review the entire Medicare and Medicare Advantage market in particular to see what advantages Clover Health brings to the market relative to competitors. I end with a recommendation on the stock.

What is Medicare?

In the United States, after you turn 65 years of age, you get certain health care benefits from the government. Medicare covers medical and hospital costs. There is no “cap” on what you might pay out of pocket and it tends to be fairly restrictive. Most people don’t pay a monthly premium for Part A (free part of Medicare).

What is Medicare Advantage?

Medicare Advantage Plans are health insurance, sometimes called “Part C” or “MA Plans,” are an “all in one” alternative to Original Medicare.

They are offered by private companies approved by Medicare. If you join a Medicare Advantage Plan, you still have Medicare. These “bundled” plans include Medicare Part A (Hospital Insurance) and Medicare Part B (Medical Insurance), and usually Medicare drug coverage (Part D).

Most Medicare Advantage Plans offer coverage for things Original Medicare does not cover, like some vision, hearing, dental, and fitness programs (like gym memberships or discounts). Plans can also choose to cover even more benefits. For example, some plans may offer coverage for services like transportation to doctor visits, over-the-counter drugs, and services that promote your health and wellness.

Medicare pays a fixed amount for your care each month to the companies offering Medicare Advantage Plans. Typically the insured individual pays a premium monthly for the “extras”.

What are the benefits of Medicare Advantage?

Medicare Advantage plans include an annual out of pocket (OOP) spending limit, critical financial protection against the costs of catastrophic illness or accident.

That is, under Part C plans, there is a limit on how much a beneficiary will have to spend annually. That amount is unlimited in Medicare Parts A and B.

How large is Medicare and Medicare Advantage?

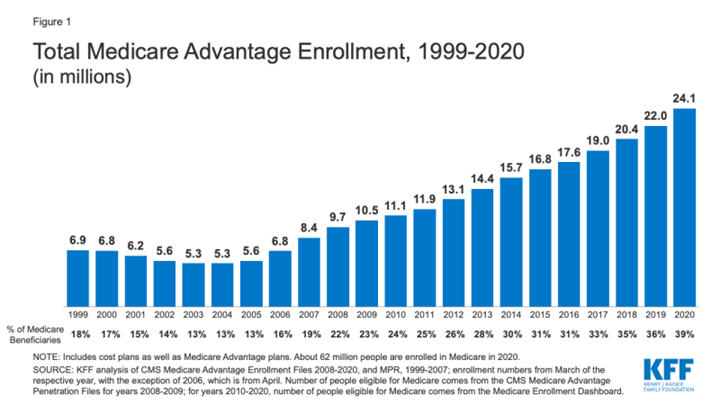

Nearly 40% of Medicare enrollees are in some Medicare Advantage plan

In 2020, nearly four in ten (39%) of all Medicare beneficiaries – 24.1 million people out of 62.0 million Medicare beneficiaries overall – are enrolled in Medicare Advantage plans.

The Congressional Budget Office (CBO) projects that the share of all Medicare beneficiaries enrolled in Medicare Advantage plans will rise to about 51 percent by 2030. This is a growing market.

This market is worth $270 Billion today and is expected to grow to over $500B by 2030.

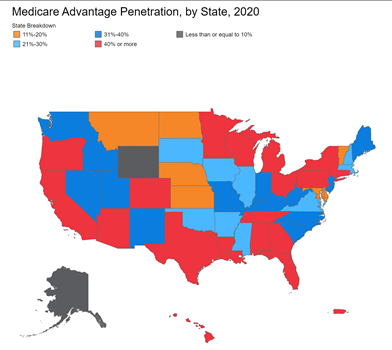

Medicare Advantage is more prevalent in state with higher costs of living

Who are the key players / market operators in this market?

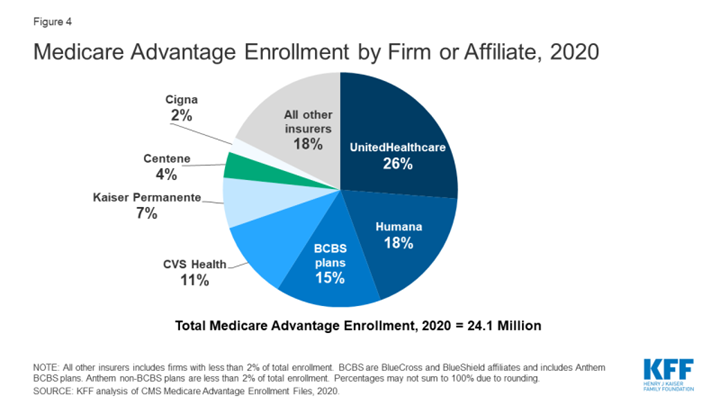

Key insurance companies offering Medicare Advantage plans and their market share

Medicare Advantage is offered by 100s of insurance companies. They get “paid” by the government if an enrollee joins their plan. The enrollee might pay more premiums out of pocket to cover the extras.

The top 2 insurance providers – United Healthcare and Humana own over 40% of the market, while the top 3 (including Blue Cross Blue Shield) own over 50%. CVS acquired Aetna.

Is Medicare Advantage a profitable segment of market for these insurers?

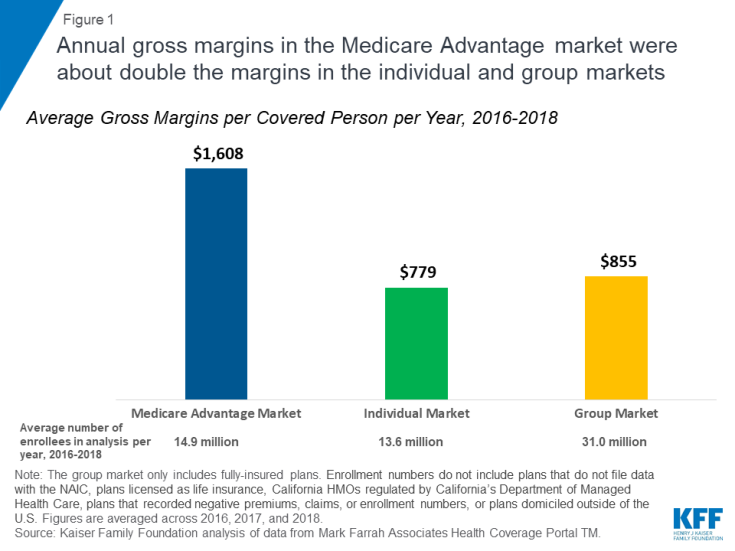

Gross margins for Medicare Advantage plans averaged $1,608 per covered person per year between 2016 and 2018 – about double the average annual gross margins for plans in the individual and group markets. That is reasonably profitable.

In 2019 alone, Health insurance companies made $35B in profit, and the biggest part of that growth came from MA (Medicare Advantage) plan growth.

In the United States, almost 60% of people are covered by Group plans, and only 15% by individual plans, so Medicare is very profitable for insurers.

Medicare Advantage plans are very profitable

If you take into account however the costs, and since older people are more prone to higher healthcare costs, the Group market is as net profitable as Medicare Advantage.

What differentiates one Medicare Plan from another?

For the insured (patient):

No ($0) premium plans with extra coverage than offered by Medicare

More services & flexible provider choices offered by the Insurance company – meaning I can go to any doctor or physician instead of a limited choice

Quick (paper-free or less paperwork) settlement of claims

For the provider (doctor / hospital / clinic)

Less paperwork in submitting claims

Getting claims paid quicker and faster

Getting proactive with patients to reduce visits and increase healthcare provider productivity

What are the big trends that are shaping this market?

The biggest trends that are to be watched closely in the Medicare Advantage market are:

Rapid growth of Medicare advantage as more people move from simple Medicare to Advantage plans – Insurers are trying to differentiate themselves by providing more in-network services

Pay for value (outcomes) instead of fee for services. This aligns interests of provider (doctor) with patient, so instead of the provider making them spend more money on tests and procedures they focus on keeping the patient proactively heathy.

Telemedicine, in-home patient care, remote care, managing costs of prescription drug coverage are all the larger healthcare trend that are relevant for Medicare Advantage as well.

Who is Clover Health? What is their background?

Clover Health was founded in 2012 by Kris Gale (“Gale”) and Vivek Garipalli (“Garipalli”).

Clover Health completed its Series A round of funding in 2015, raising $100 million from investors such as Athyrium Capital Management and First Round.

The Company completed its Series B round of funding later that same year, with its Series C round completed in May 2016.

Clover Health has raised around $295 million in funding, from investors including Nexus Venture Partners, Greenoaks Capital, Arena Ventures, and Sequoia Capital.

Clover Health currently serves a range of customers across counties in New Jersey and Texas, with plans to expand its operations further.

What does Clover Health offer?

Clover Health is a medical insurance and medical services provider. The Company provides a range of health coverage plans to members, which are specifically targeted at consumers aged over 65 years of age who have chronic illnesses or certain disabilities, under the government-funded Medicare Advantage program.

The Company collaborates with a range of healthcare providers – including physicians, clinics, specialist care providers, and eye care providers.

How is Clover Health different?

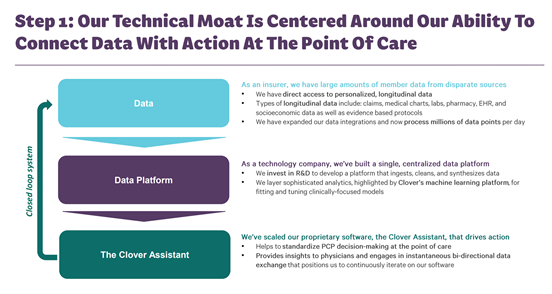

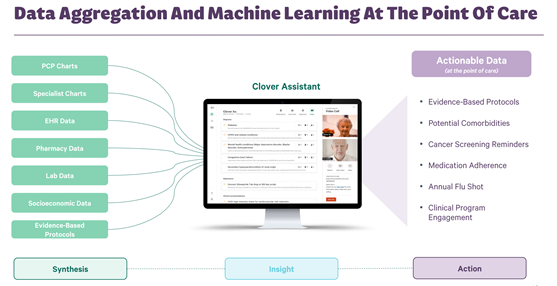

In order to offer better outcomes for patients, the founders realized they need to use data and machine learning for patients, doctors and everyone else in the system. This can help reduce patient visits, make it easier to identify patient problems quicker and reduce cost of healthcare.

Clover has a data platform to help doctors proactively identify problems

Clover set to build an expert system powered by data and AI to help doctors and providers get answers proactively using Clover Assistant (Used by Doctors).

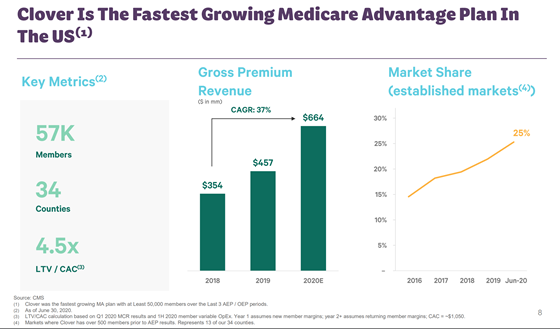

How fast is Clover Health growing?

Fast. Extremely fast. Clover is available in few markets, but it is growing into other markets rapidly.

Dramatic growth

Doesn’t every one say Machine Learning and AI these days?

Yes, every company says that in their IPO and presentation documents. The key is to see if

a) they have enough data,

b) they have expertise to use that data to build ML models,

c) they have problems (questions) to answer that can be scaled,

d) those answers can drive business outcomes, i.e. increase revenues, reduce customer churn, reduce cost of customer acquisition or reduce cost of services.

I believe Clover Health has all the elements to help them leverage data and technology to increase patient outcomes.

So what will that mean going forward?

This should result in Clover doing 3 things:

Increase patients under coverage (thereby increasing revenue)

Taking share from other providers in the market

Reducing cost of providing care and hence improving margins

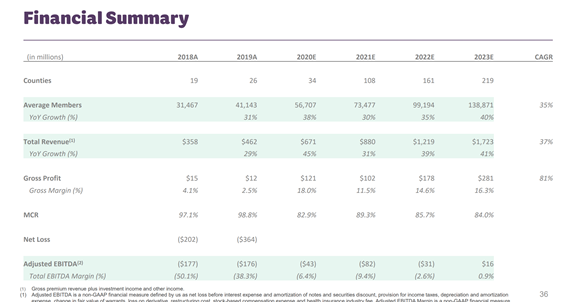

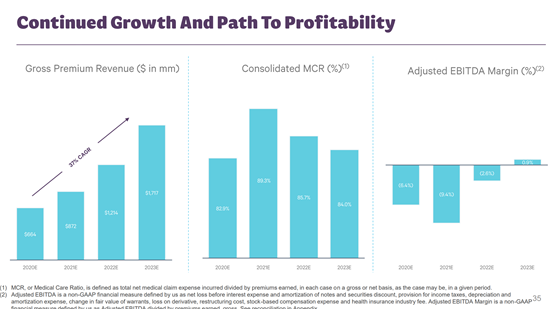

This will mean revenues grow 37% (CAGR) from $664M in 2020 to $1.7B by 2023.

This means EBIDTA margins of 0.9% by 2023 from -6.4% in 2020.

Is this a good stock to own?

Clover is currently priced at $13.24 per share with a Market cap of $5.9B. It has a 52 Week High of $17.45 so 24% off its high. It is richly valued, but the growth is compelling.

I believe the combination of data driven patient outcomes with a doctor provided Clover assistant offering is a differentiator in the market, where most other plans only offer an “insurance” offering.

I cant say that Clover stock price will not go down further from here, but this is an attractive stock to own for the long term in the Healthcare market for 3-5 years.

What are is the 1 year price target?

Assumptions:

2021 Revenue will be > $900 Million (company provided range is $872 M). 2020 Revenue is $671M.

Revenue growth for 2021 is 33%.

Current EV/ Revenue Multiple is 8.9.

I expect continued margin improvement to 20% (currently 18%).

Over 75K Medicare advantage members (company provided range is 73.4K)

Based on these assumptions, and looking at comparable growth ranges (below) and industry multiples I think this can be given a multiple of 8 – 10 EV/Revenue.

For 8X EV/Revenue the stock price at the end of 2021 will be $16.25, with 21% upside.

For 9X EV/Revenue, the stock price at the end of 2021 will be $18.2, with 36% upside

For 10X EV/Revenue, the stock price at the end of 2021 will be 20.3, with an upside of 51%.

Even at these multiples, given the growth it will be valued in between a high growth SaaS company and a poorly valued Healthcare insurance company.

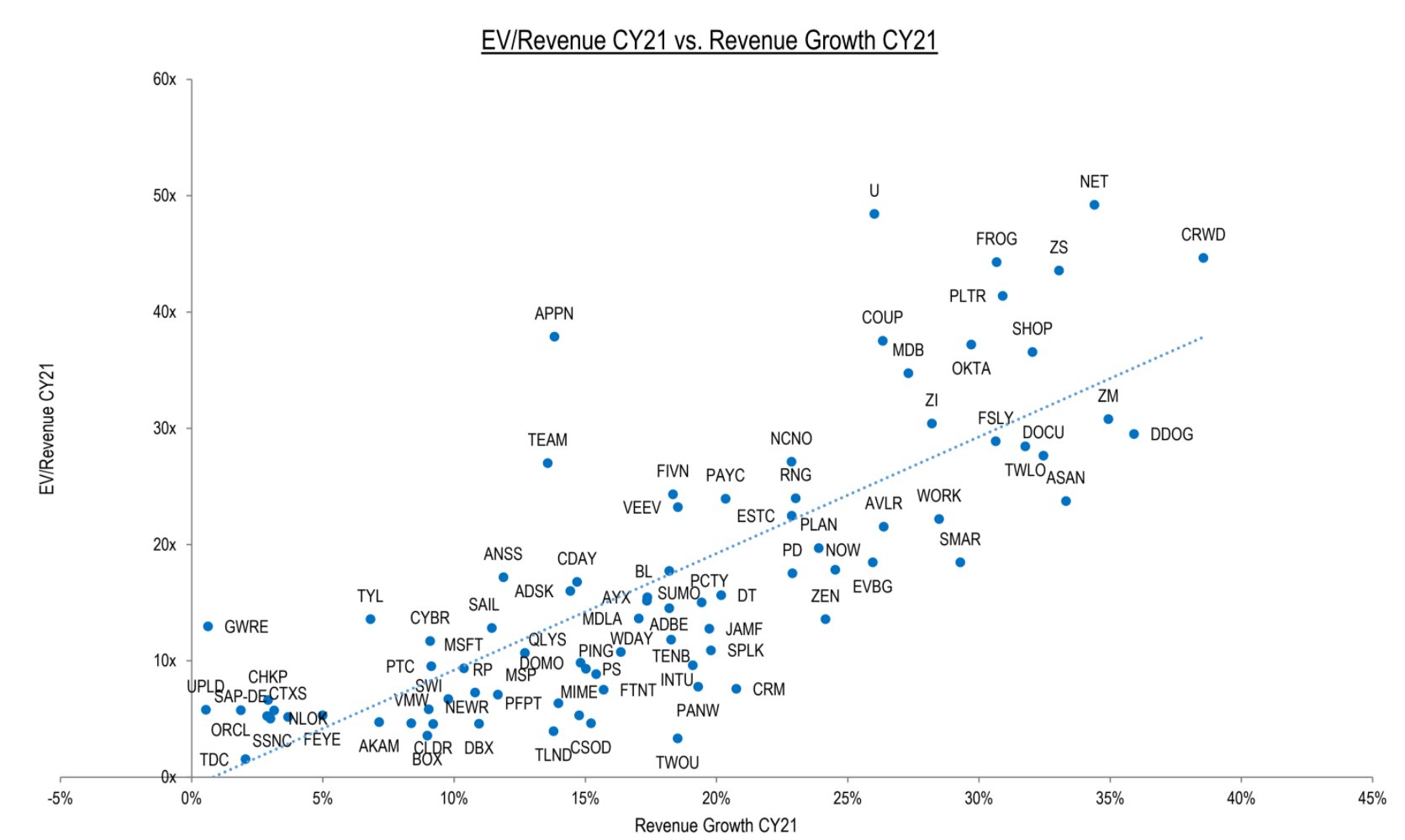

2021 Growth and Revenue multiples of tech companies

2020 Medicare revenue multiples

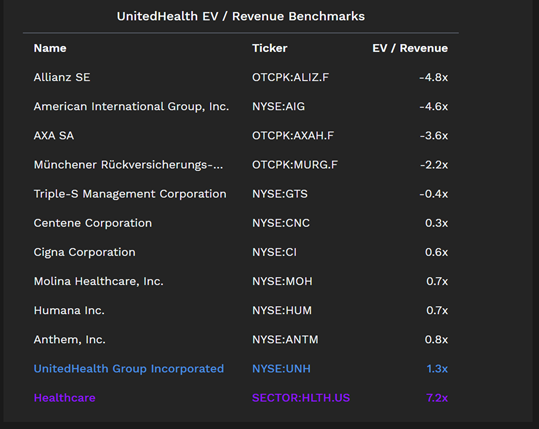

EV to Revenue Multiples for Health Insurance companies

How can Clover Health grow faster?

Clover Health has stated that it can use its technology in a scalable fashion. It will likely acquire many more companies (see targets below) in the space to rapidly increase revenues and number of patients in plan.

What are the risks?

They are a local (regional) provider in 1-2 states and still building out their scale and capabilities

Carepoint a previously owned hospital chain by the founder contributed to most of the initial enrollment (source)

Their growth by acquisition approach is still to be proven. They have not acquired a single company so far.

Most people know AirBnB as the hospitality platform, where you can book rooms and experiences. It is a two sided market place with guests(demand) and hosts(supply).

I have been investing in the company since the IPO (I will keep buying as well) and am expecting to hold it for 10+ years. This is one of my best stock ideas of 2020-2030. Here is some background and research on why I love $ABNB.

AirBnB was founded in 2008 in San Francisco by Brian Chesky, Joe Gebbia and Nathan Blecharczyk.

Revenue totaled $2.5 billion over the first nine months of 2020, down 32% year-over-year.

How and why did they get started?

When the Industrial Designers Society of America (IDSA) conference came to San Francisco in 2007, overwhelming the city’s hotels, Joe emailed Brian with an idea to “make a few bucks.” He thought it would be a crafty way to subsidize their rent.

The team made three product decisions that shaped their future:

Facilitating payments on-platform. Instead of sending guests to PayPal or another website, Airbnb handled payments themselves.

Introducing ratings. Airbnb introduced a reputational system in which hosts and guests rated each other.

Three-click booking. In just three clicks, anyone could book a place to stay.

Chesky and Gebbia created and produced limited edition Cap’n McCain’s and Obama O’s cereals that they sold for $40 a pop. That hack netted the company $30K

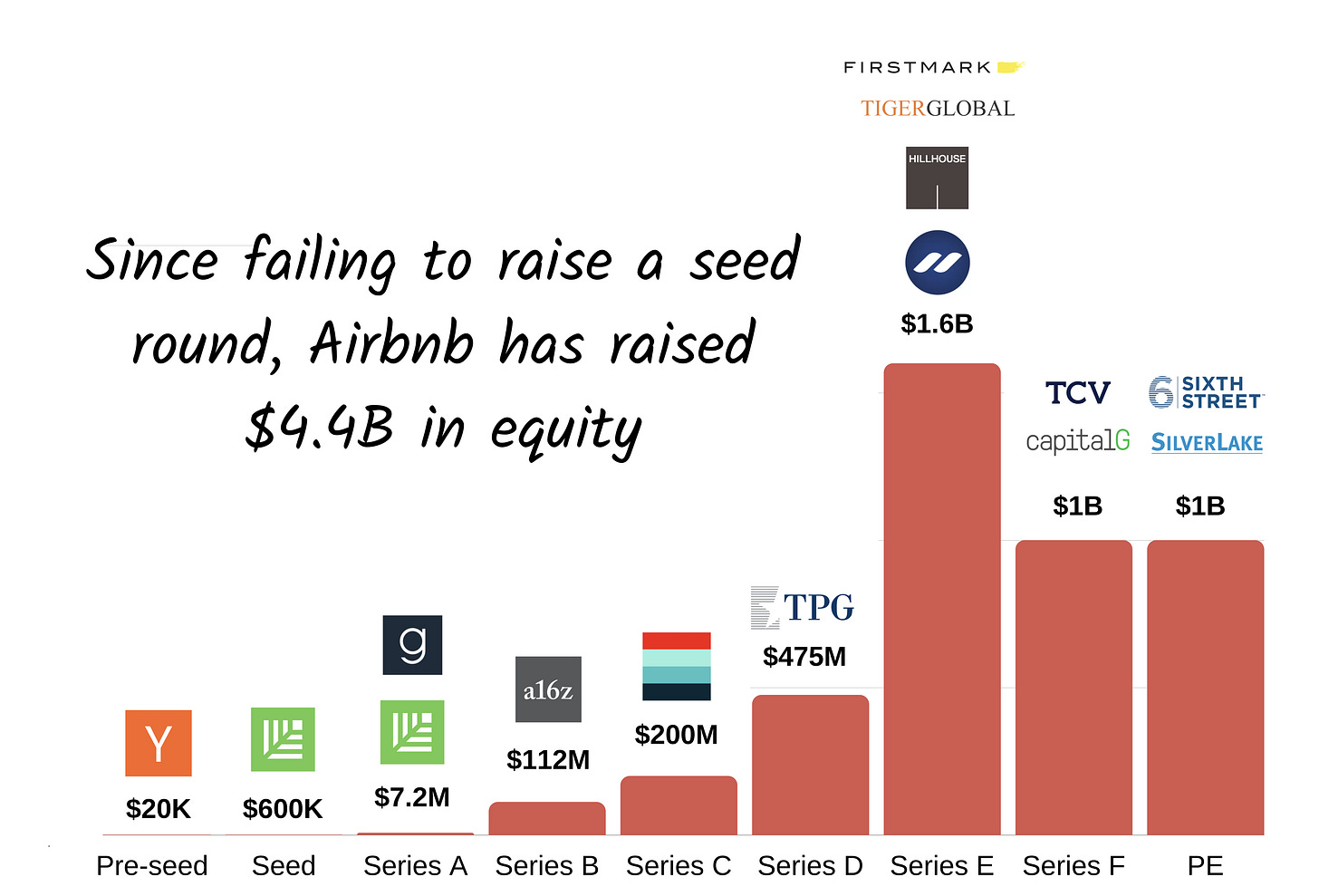

How much money has the company raised?

AirBnB has raised over $6.4 Billion so far to fund the company.

Over $6.4 Billion since founding and over $1B during the IPO

What are the key milestones?

By 2011, Airbnb users had booked a million nights (or 2,739 years) through the platform.

By January 2012, Airbnb hit 5 million cumulative nights booked.

In June 2012, the company hit 10 million.

In November 2016, Airbnb launched Experiences.

How big is the market?

$3.4 trillion. That’s the company’s estimate for their total addressable market (TAM). The reason Airbnb’s opportunity is so enormous is partially because it created a new category.

80% consists of Airbnb’s core business, “short-term stays,” defined as those lasting 28 days or less.

Airbnb expects an expansion in the short-term market from $1.2 trillion to $1.8 trillion. This growth is based on an increasing population and a growing travel market

What is the business model?

Revenue comes from service fees, charged to customers.

In 2019, Airbnb raked in $5.3 billion in service fees on a Gross Booking Value of $38.0 billion – so its service fees accounted for 17% of GBV. That 17% cost is shared, though not equally, by the guests and the hosts.

The bulk of the fees fall on the guest, with “most guests” paying under 14.2%, and “most hosts” paying 3%.

What does the financial picture look like?

The company measures financial performance across a few key metrics.

Gross Booking Value (GBV). This is defined as the dollar value of bookings on the platform

Revenue. This represents the amount brought in by Airbnb through service fees.

In terms of GBV, the company generated $38 billion in 2019, supporting a growth rate of 29% from $29 billion in 2018.

These GBV metrics equate to revenue of $4.8 billion and $3.7 billion in 2019 and 2018, respectively.

The first three quarters of 2020 saw both metrics take a hit, with Airbnb generating just $18 billion in GBV (down 39% YoY) and Revenue of $2.5 billion (down 32% YoY).

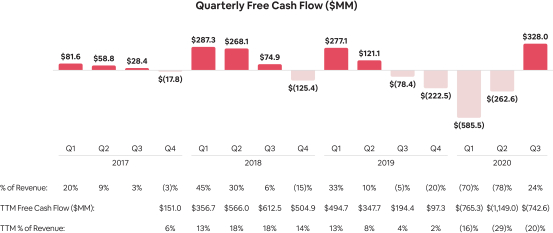

Quarterly revenue growth (or lack of it in 2020)

What are the moats?

Brand recall: Despite slashing Sales & Marketing spend Airbnb’s acquisition remained strong. 91% of all traffic to the site came through direct or unpaid channels, supporting an organic growth story. When it is time to travel (or find a new experience), a large portion of guests instinctively navigates to Airbnb.

On the other side host loyalty is best understood through retention data. Airbnb’s host revenue retention since 2014 sits at or above 88% by cohort.

Airbnb has demonstrated its model’s potential profitability, albeit in fits and starts.

Who are the competitors?

Key competitors are:

OTAs – such as Booking.com, Expedia (Vrbo), and Tujia (China)

Potential competitors from hotel chains such as Marriott, Hilton, etc.

What are the key metrics

4 million hosts

5.6 million active listings

220 countries and regions, 100,000 cities, 55% hosts are women

110 million guests cumulative in 13 years

110 billion host earnings total in 13 years

What are the risks?

Airbnb hasn’t been profitable so far and has incurred net losses every year.

In the S-1, Airbnb reported net losses of $70.0 million, $16.9 million, $674.3 million, and $696.9 million for the years ended December 31, 2017, 2018, and 2019, and nine months ended September 30, 2020, respectively.

Another concern is the liability factor. Some cities have put a ban on single-night rentals to stop the renting of “party houses” for raucous events.

Revenue concentration: While no single city accounted for more than 2.5% of the company’s revenue, in 2019, 11.9% of the company’s revenue came from just 10 cities.

The bear case for Airbnb’s long run operating profit margin is that travel is a category where you’re competing for a consumer’s business each time they book a trip.

Why invest?

In the travel space there are few “great brands” – AirBnB could be one of those, besides Disney. Most airlines are hated, most hotels not loved and all OTA’s just ignored.

“Airbnb” has gone from brand name to a common noun in the same vein as using a “Kleenex” or drinking a “Coke”.

The management team – founder led, AirBnB has passionate committed founders with an ability to keep introducing new offerings to keep their hosts and guests happy is my bet.

It unlocks of a vast supply of new lodging inventory, previously unavailable and gives hosts an opportunity to make money off a latent asset.

Cash float: Airbnb convinced travelers to part with 100% of their booking cost up front and then they pay out the required amount to hosts when the stay actually occurs. Airbnb therefore generates substantially higher free cash flow (FCF) than accounting profit.

Comparable pre tax operating income:

Airbnb -10%

Expedia 8%

Booking Holdings 35%

Hilton 17%

Marriott 9%

What are my return expectations?

As a multiple of revenue, AirBnB is rich. Airbnb’s revenue is expected to rise by 30% to $4.33 billion by 2021. Let’s assume that its revenue rises an average of 30% over each of the next five years from that to 2026. That means sales will be 3.72 times $4.33 billion or $16 billion.

Therefore, if Airbnb stock ends up with a similar valuation as Uber, Square or other well valued marketplaces, its market cap will be 8.33 times $16 billion by 2026. That works out to $133.3 billion, or 59% more than the market cap of $83.89 billion.

#

Ticker

Rev Growth

EV/Rev

EV/EBITDA

1

CVNA

51%

5.3

0

2

RDFN

49%

5.4

0

3

DKNG

46%

21

0

4

Z

44%

6.3

0

5

UBER

42%

6

0

6

TRIP

41%

4.5

59

7

ABNB

37%

21

0

8

LYFT

36%

4.3

0

9

BKNG

34%

9.6

48

10

SHOP

33%

36

35

11

FVRR

29%

27.8

0

12

DMYD

31%

12.53

68

AirBnB is richly valued to 2021 revenues at 21X with 37% growth