Summary

The Ultrasound market is a ~$7B global medical systems opportunity in 2020, growing to over $10B by 2025. The market has been long dominated by expensive cart systems from GE, Siemens and Phillips at expensive price points (>$50K). However newer disruptors in the segment of handheld systems, such as Butterfly Network are using AI and inexpensive handheld hardware ($2K + $500 annual fee) to “democratize” the use of Ultrasound for many new applications and types of users. This segment of handheld is the fastest growing at 25% CAGR.

This creates an opportunity to expand the market and fundamentally changes the landscape for Ultrasound. This is similar to how Southwest Airlines created low cost point-to-point flying, reducing costs, by doing away with many frills, thereby expanding the market and increasing the number of flyers. Or how Uber “expanded” the rides market by taking on incumbents in the taxi and limo markets by creating a market of supply by making “anyone with a car, a driver”.

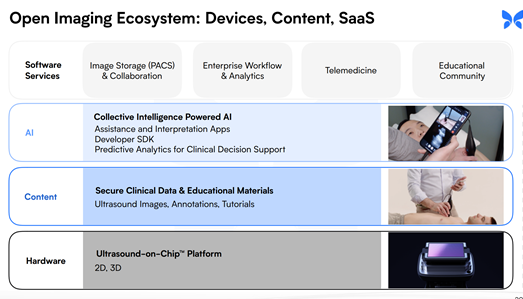

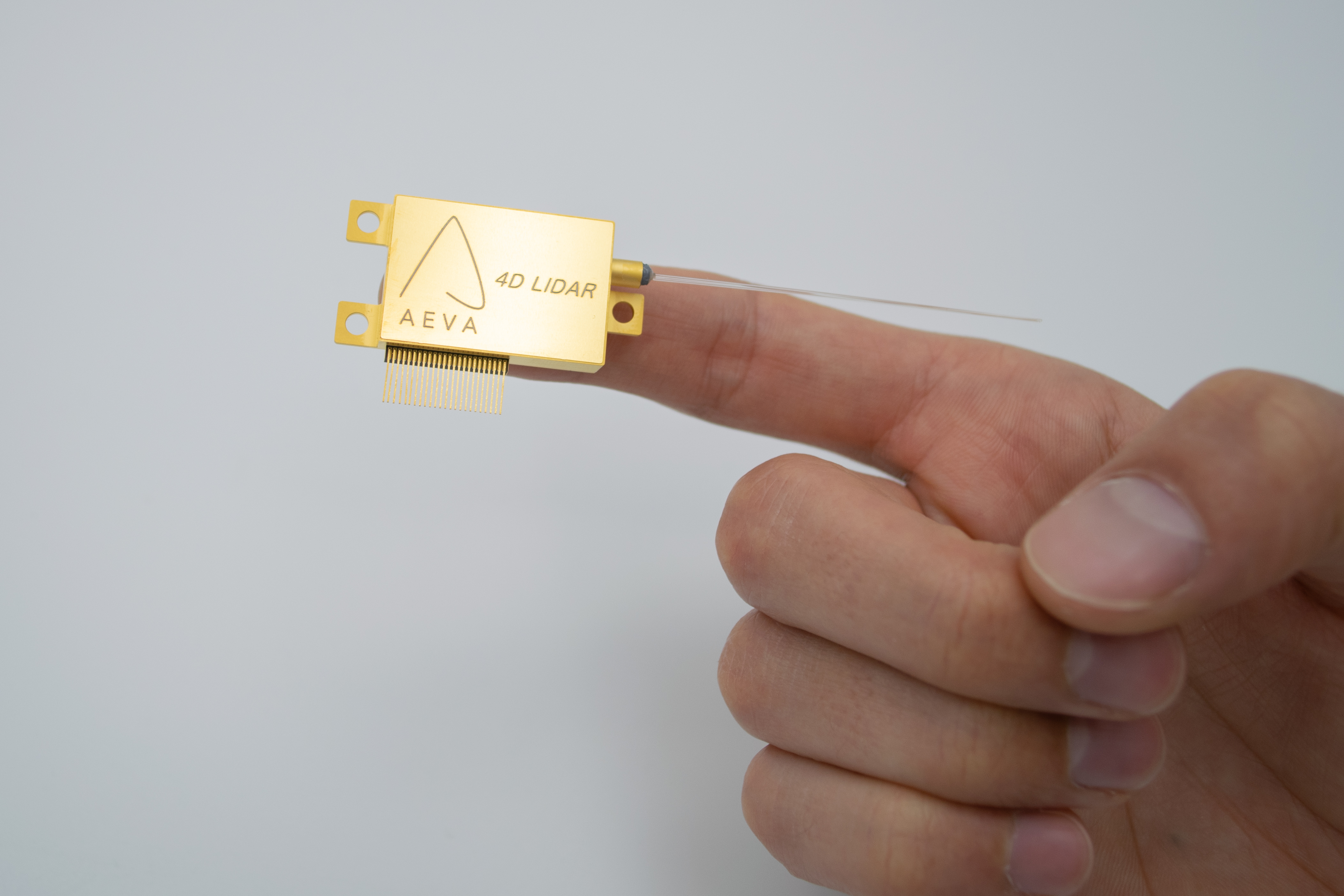

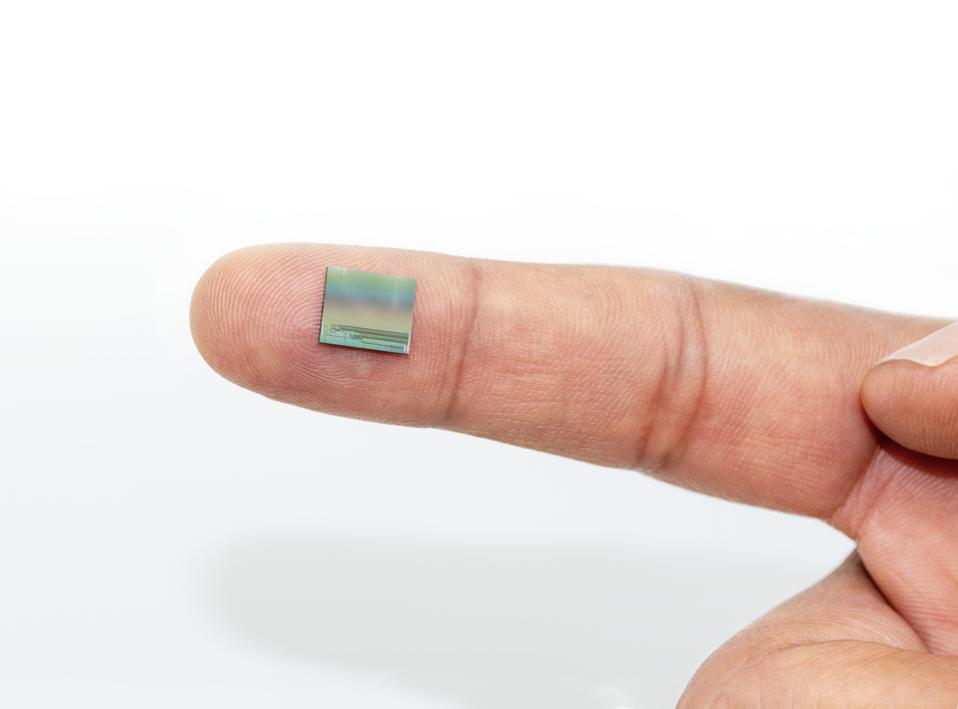

Butterfly Network was founded in 2011, by Jonathan Rothberg, an industry veteran and luminary. The company has raised over $350M from multiple investors including the Bill and Melinda Gates foundation. The company has 3 unique differentiators: a) handheld hardware (ultrasound SoC – System on Chip) with patented capability to provide 3D imaging on depth, b) strong use of Artificial intelligence for imaging analysis and c) a network of experts with content – which can now create less expensive “doctor’s aides” into ultrasound technicians.

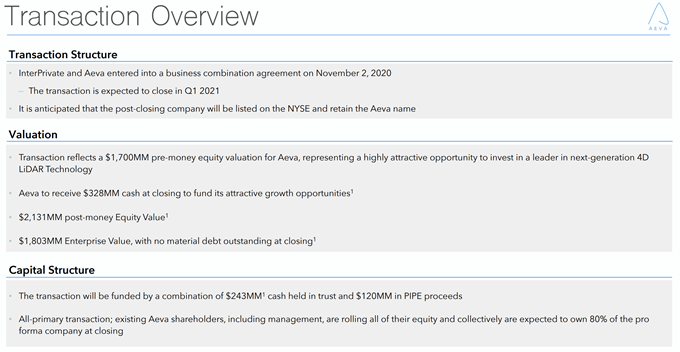

Butterfly Network has chosen to go public on Nov 25th via a SPAC with Longview Capital ($LGVW) providing it with $584 million in cash, and valuing the company at $2B (post money). It currently trades (12/29/20) at $20.5, valuing the company at $4.17B.

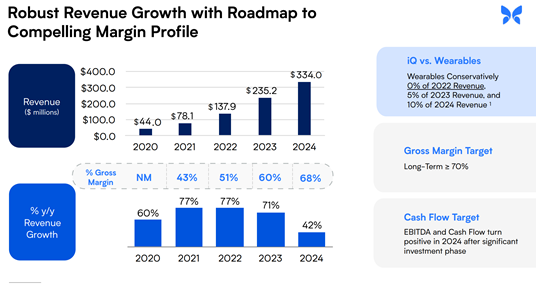

This represents a 94X multiple on 2020 LTM revenue ($44M), 53X NTM revenue ($78M) and, 30X 2020 revenue ($137M). While rich, the reason could be attributed to the expected 70% revenue growth rates for 4 years (2021-2024), strong management team, unique technology, seasoned backers and disruptive market approach which could dramatically increase revenues and growth to over 100% annually for many years.

My recommendation is to initiate a long term position, with an expectation to hold for 4 years, when it will be at $235M in revenue and likely at $10B in market capitalization (42X Revenue), representing a ~139% upside in 4 years (~31% CAGR).

In 2021 I expect it to consolidate and have put a price target of $24.5 by Dec 2021, representing a 29% upside from its current price. It is likely that momentum investors will ignore the stock by Q1 / Q2 when the acquisition is complete and the stock lists as $BFLY, at which point I expect the stock to drop to between $15 – $17 per share. My recommendation is to dollar cost average (DCA) in with 25% sizing initiation by quarter or 10% every 2 weeks.

If the company delivers higher revenues that projected in its first two quarters of being public – expectations are $18 to $20M in Q1 and Q2 2021, then I would expect the stock to further gain in price to be at $30.

The biggest risks for Butterfly Network stock include a) lack of revenue growth due to insufficient trained technicians, b) an incredibly competitive landscape with over 80 other companies in the space (many with larger distribution), c) likelihood of Apple ($APPL) to enter the space with a software solution to partner with any ultrasound hardware (low likelihood), d) the very high valuation getting a significant haircut post the merger due to momentum investors moving to other pastures and e) lack of long public company operating experience making internal controls for finance, reporting and operations a material weakness.

What is Ultrasound?

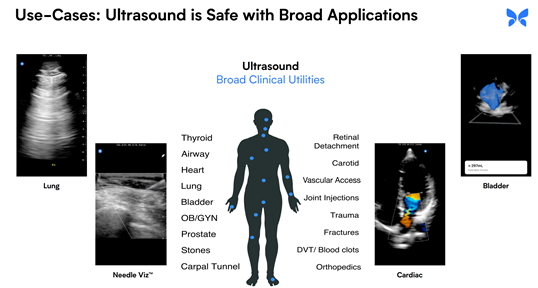

Diagnostic ultrasound, also called sonography or diagnostic medical sonography, is an imaging method that uses high-frequency sound waves to produce images of structures within your body. The images can provide valuable information for diagnosing and treating a variety of diseases and conditions.

Diagnostic ultrasound is a safe procedure that uses low-power sound waves. Unlike X-Ray which might cause some radiation, Ultrasound is safe.

Ultrasound is used for many reasons, including:

View the uterus and ovaries during pregnancy and monitor the developing baby’s health, Diagnose gallbladder disease, Evaluate blood flow, etc.

How does Ultrasound work?

High-frequency sound waves travel from the probe through the gel into the body. The probe collects the sounds that bounce back. A computer uses those sound waves to create an image. Ultrasound exams do not use radiation (as used in x-rays). Because images are captured in real-time, they can show the structure and movement of the body’s internal organs. They can also show blood flowing through blood vessels.

Conventional ultrasound displays the images in thin, flat sections of the body. Advancements in ultrasound technology include three-dimensional (3-D) ultrasound (Butterfly’s market) that formats the sound wave data into 3-D images.

Ultrasound scanners consist of a computer console, video display screen and an attached transducer. The transducer is a small hand-held device that resembles a microphone. Some exams may use different transducers (with different capabilities) during a single exam. The transducer sends out inaudible, high-frequency sound waves into the body and then listens for the returning echoes.

How big is the Ultrasound market?

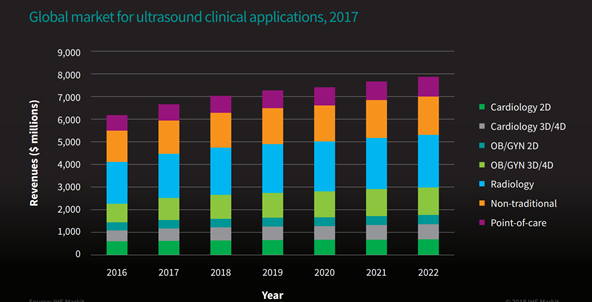

The Ultrasound market is expected to grow to over $10B by 2025.

Global ultrasound unit shipments grew 9% from 2016 to 2017 and totaled 218,767 in 2017. Traditional ultrasound unit shipments totaled 149,013 and accounted for 68% of the total ultrasound market in 2017. Segment growth was driven by strong demand for traditional equipment in China.

Point-of-care ultrasound (Butterfly’s market), which consists of anesthesia, critical care, emergency medicine, musculoskeletal, and primary care applications, was the smallest ultrasound segment in unit shipment terms in 2017. However, point-of-care unit shipments grew 14% from 2016 to 2017— the highest year-over-year growth rate of all three ultrasound segments.

What is handheld Ultrasound?

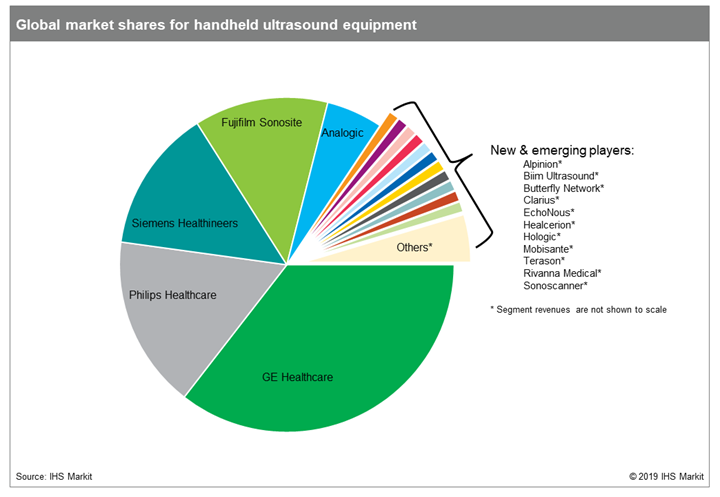

Sales of handheld ultrasound accounted for less than 2% of the $6.9B global markets for ultrasound equipment. The relatively high cost and limited performance of early generation handhelds were limiting factors. Steady product improvements over the years, coupled with fresh innovation from new market entrants (Butterfly), are beginning to unlock the full value of handheld ultrasound, both for experienced and new users alike.

Credentialing, data security and quality assurance (both for image capture and interpretation) can be challenging. While handheld ultrasound devices may be ready for mainstream adoption, many institutions lack the IT infrastructure required to provide seamless patient care between the office and hospital settings.

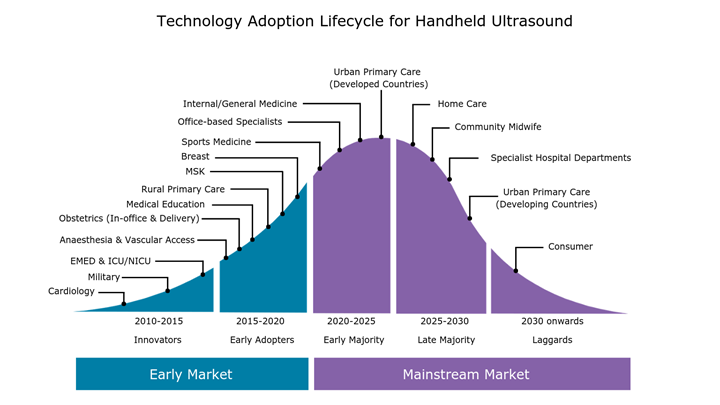

Primary care remains a largely untapped market for handheld ultrasound, and is potentially the largest opportunity, with more than 250,000 primary care physicians in the US alone.

The handheld ultrasound market is growing rapidly, as the latest generation of ultra-portable devices gains acceptance among a diverse range of customer groups, from emergency medicine physicians and internists and office-based specialists, and looking forward, primary care physicians. The expanding customer base, coupled with the increased availability of affordable handheld scanners, is forecast to boost global sales of handheld ultrasound by over 50% in 2019. By 2023, the global market for handheld ultrasound is forecast to exceed $400 million.

Who are the key players?

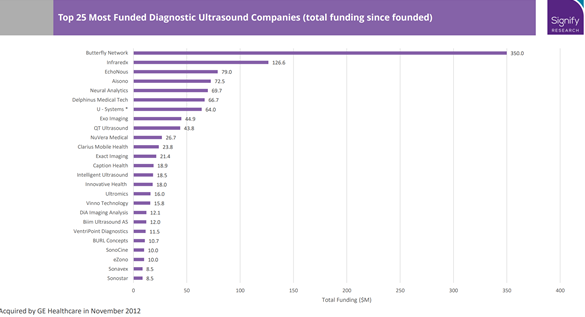

While traditional players such as GE Healthcare, Siemens and Phillips matter, over 50 new companies have been funded in the last 12 years.

Butterfly Network began shipping its Butterfly iQ scanner towards the end of 2018 at the headline price of $1,999 (plus annual subscription of $420). In response, GE Healthcare cut the price of the basic version of Vscan Extend to $2,995 (currently US only).

While the price is becoming less of an issue, many primary care physicians lack formal ultrasound training and reimbursement is not widely available.

To address the lack of skills issue, vendors of handheld scanners are striving to simplify ease-of-use, both in terms of the device itself and integrated tele-ultrasound services that connect novice users with experts at separate locations over two-way audio and video calls.

The latest generation of handheld scanners feature numerous presets for common exam types and artificial intelligence (AI) is being applied to enable physicians with no prior scanning experience to capture high-quality images. AI-guided ultrasound will help users to identify body parts and correctly position the transducer to maximize the image quality for a given exam. Moving forward, AI will also play an increasingly important role in image interpretation, providing physicians with automated measurements, anomaly detection, and diagnostic decision support.

What is the customer problem?

For patients who do not want exposure to radiation (X-ray) and need a quick convenient way to view internal organs for issues, Ultrasound is the best solution.

For example, ultrasound is playing an increasingly important role as a screening tool for women with dense breast tissue. In acute care, ultrasound is increasing being used for lung imaging to diagnose conditions such as pleural effusion, pulmonary oedema and pneumothorax. In another example, the use of shear wave elastography is expanding beyond hepatology (e.g. liver fibrosis) to other body areas, including breast, prostate, thyroid and spleen. Musculoskeletal is another relatively untapped market for ultrasound, including orthopedics, rheumatology and sport’s medicine.

Who is Butterfly?

Butterfly Network, Inc. (“Butterfly”) is the inventor / pioneer in semiconductor-based point-of-care ultrasound (“POCUS”) devices

Founded in 2011 by visionary innovator Jonathan Rothberg. Dr. Jonathan Rothberg PhD, Founder and Chairman, has dedicated his career to enabling breakthrough technologies to revolutionize healthcare. He was given several awards including from President Obama to further the cause of better healthcare.

Total investment of over $400 million with first product introduced in 2018, 700+ patents and 2020E revenue of $44 million, projected to grow to $138 million in 2022E.

Longview Acquisition Corp. (“Longview”) is a Special Purpose Acquisition Corporation (“SPAC”). Initially capitalized with $414 million in cash in May 2020.

Butterfly develops a sensor and software to enable handheld Ultrasounds.

400-member team.

What is unique about Butterfly? What is their moat?

There are 3 parts to Butterfly:

- A 3D patent pending rendering sensor with System on Chip

- AI and software to make it easier for diagnosis without significant training.

- Strong content and delivery network to train new specialists and “less expensive” technicians.

Who are the competitors?

As mentioned over 100 companies old and new startups exist in the space. Butterfly is the most funded, the earliest and has the most patents among the smaller upstarts.

Why will Butterfly win over others?

- Funding: Better funded ($400M to date, plus $453M from the SPAC IPO)

- Sensor technology: Proprietary SoC with hundreds of patents on the sensor

- Distribution: Strong distribution framework for new applications

- Software and AI: AI and machine learning software to make it easier for technicians to diagnose problems

- Support: Strong training and support network

- Competitive Price: Superior price point (under $2000) plus annual fees (subscription)

- Talented management team: with CEO who has experience in managing fast growing companies.

Artificial intelligence (AI) will have a transformative impact on the market as it addresses some of the key limitations associated with ultrasound; namely, the shortage of trained sonographers and the relatively steep learning curve, high operator dependency both during image acquisition and interpretation, poor image quality for certain exam types and the relatively lengthy exam time compared with other modalities.

The first wave of ultrasound AI applications are entering the market and are mainly for image optimization (noise reduction) and automation of time consuming and repetitive tasks, such as anomaly detection, image labelling, feature quantification and classification.

However, the greatest impact of AI will be guided ultrasound (ultrasound navigation), which will provide real-time support during image acquisition (i.e. probe placement and anatomy detection). This is what Butterfly does best.

What are the financial projections?

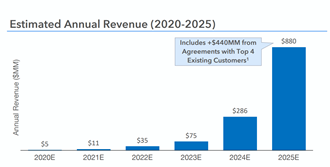

Butterfly is expected to grow at over 60% in 2020 from 2019 and over 77% for the next 2 years to reach $138M in 2022.

Why is the valuation of Butterfly so rich?

Given the rich background, the lack of multiple companies that are public in the space and execution record, Butterfly is very highly priced. It does have strong projections of growth in revenue to back the valuation.

References

https://www.mayoclinic.org/tests-procedures/ultrasound/about/pac-20395177

https://www.radiologyinfo.org/en/info.cfm?pg=genus

https://www.rootsanalysis.com/reports/view_document/handheld-imaging-devices/319.html

https://equityzen.com/company/butterflynetwork/

:no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/13189667/Ped_final.jpg)