There are 5 companies planning to go IPO that I am tracking closely

1. AirBnB

If there is one company in the travel space that has benefited post Covid it is AirBnB. The company is looking to raise $3B, with an expected valuation at $25B – $30B. It generated $4.8 B in revenue last year with about $400M in losses. It has apparently been growing since May and is close to profitability.

2. Affirm

The company provides short term loans (BNPL – buy now pay later) to consumers for *mostly* online purchases. Metrics are unavailable, but valuation could be in the $2B – $5B range. Another Covid winner, with revenues quadrupled post March.

3. Doordash

The food delivery company filed its S1 last week revealing a 226% increase in revenue during the first 9 months of the year (another winner thanks to Covid).

The company posted $885 million in revenue for 2019, up from $291 million in 2018. For the nine months ended Sept. 30, 2020, DoorDash generated $1.9 billion in revenue, up from $587 million for the same period in 2019.

Meanwhile, the company reported net losses of $667 million for the year 2019 and $149 million for the nine-month period ended Sept. 30, 2020, compared to net losses of $504 million and $203 million, respectively, reported for the same time in 2018 and the same nine-month period in 2019.

The company said, it holds approximately 50 percent of the market share based on total sales, followed by Uber Eats at 26 percent

4. C3.ai

The Tom Siebel founded Enterprise AI company has filed to raise $100 M. It provides AI and data science technology and services. For 12 months ending Jul 2012, the company booked $162 M in revenue and is not profitable.

5. Roblox

A leading online game developer, was founded in 2004. They provide a gaming environment safe for children. They are expected to post $225 M in revenue in 2020, up over 112% from 2019. It raised $150 M in funding (Feb 2020) valuing it at about $4B.

Doordash, Wish, AirBnB, Affirm, C3.ai and Roblox file for IPO

Bonus

1. Wish

The deep discounter (eCommerce marketplace) company / app, has raised over $1.6B over the last decade, with most recent valuation at $11B. It has over 70 Million active users in 100 countries. Wish was estimated to drive $1.9 B in revenue in 2019, a 109% growth over 2018.

I wrote about ANT financial a few weeks ago. It was a much anticipated IPO and would have been the largest ever. Until the Chinese primer decided that was not going to be the case. The WSJ says, ANT has indefinitely postponed its IPO.

Credit: WSJ

Chinese President Xi Jinping personally made the decision to halt the initial public offering of Ant Group, which would have been the world’s biggest, after controlling shareholder Jack Ma infuriated government leaders, according to Chinese officials with knowledge of the matter.

The rebuke was the culmination of years of tense relations between China’s most celebrated entrepreneur and a government uneasy about his influence and the rapid growth of the digital-payments behemoth he controlled.

Mr. Xi, for his part, has displayed a diminishing tolerance for big private businesses that have amassed capital and influence—and are perceived to have challenged both his rule and the stability craved by factions in the country’s newly assertive Communist Party.

In a speech on Oct. 24, days before the financial-technology giant was set to go public, Mr. Ma cited Mr. Xi’s words in what top government officials saw as an effort to burnish his own image and tarnish that of regulators, these people said.

At the event in Shanghai, Mr. Ma, the country’s richest man, quoted Mr. Xi saying, “Success does not have to come from me.” As a result, the tech executive said, he wanted to help solve China’s financial problems through innovation. Mr. Ma bluntly criticized the government’s increasingly tight financial regulation for holding back technology development, part of a long-running battle between Ant and its overseers.

Mr. Xi, who read government reports about the speech, and other senior leaders were furious, according to the officials familiar with the decision-making. Mr. Xi ordered Chinese regulators to investigate and all but shut down Ant’s initial public offering, the officials said, setting in motion a series of events that led to the deal’s suspension on Nov. 3. Investors around the world already had committed to paying more than $34 billion for Ant’s shares. It isn’t clear whether it was Mr. Xi or another government official who first suggested the shutdown.

Chinese regulators have long wanted to rein in Ant, according to the Chinese officials with knowledge of the decision-making. The company owns a mobile payments and lifestyle app, called Alipay, that has disrupted China’s financial system. Alipay is used by roughly 70% of China’s population, has made loans to more than 20 million small businesses and close to half a billion individuals, operates the country’s largest mutual fund and sells scores of other financial products.

Ant largely focused on serving people and companies that traditional banks long ignored, and it has emerged as an important cog in Chinese finance. It has long been spared from the tough regulations and capital requirements that commercial banks have been subject to.

Regulators earlier met with strong resistance to efforts to rein in Ant from the company’s financial backers, reflecting the support Mr. Ma has had from individuals in China’s top political and business echelons, according to a person familiar with the matter. Ant’s shareholders include Boyu Capital, a private-equity fund whose partners include Alvin Jiang, the grandson of former Chinese leader Jiang Zemin. China’s national pension fund, China Development Bank and China International Capital Corp. , the country’s top investment bank, all have large unrealized profits on their investments in Ant.

Mr. Xi sought to tighten financial regulations overall after the 2015 stock-market crash in China that tested the party’s firm hold on the economy. He also came to appreciate the benefits of having firms like Mr. Ma’s, whose payment app and lending operations changed the way the Chinese spend money, provided a reliable source of funding for small businesses, and made Alibaba Group Holding Ltd. BABA -0.50% , the e-commerce giant which Mr. Ma co-founded and used to run, the pride of China.

Tech Titan Shares in Alibaba Group have surged in the years since the e-commerce giant went public, cementing its place as one of the world’s most valuable companies. Alibaba currently owns a third of Ant Group.

Ant’s roots trace back to 2004, when Alipay was started as an escrow service to facilitate payment transactions on Taobao, Alibaba’s online marketplace. Mr. Ma split off Alipay from Alibaba in 2011, a move that sparked an outcry from some of Alibaba’s big foreign investors and later resulted in a settlement with them.

Mr. Ma controls 50.5% of Ant’s voting rights, but he hasn’t ever held an executive or managerial position in the six-year-old company.

In 2008, when he was Alibaba’s CEO, Mr. Ma had lamented at a public forum that traditional banks in China were ignoring businesses that badly needed funding. “If the banks don’t change, we will change the banks,” he said, explaining that he envisioned “a more comprehensive lending system that served the needs of small businesses.”

In 2013, as Alibaba’s chairman, he again took aim at traditional Chinese lenders, saying at a public forum in Shanghai that the country didn’t lack banks or innovative institutions, but a financial institution that could power China’s economic growth in the next decade. “The financial industry needs disrupters” and outsiders to bring about changes, he said.

Around that time, Alipay created an online money-market mutual fund designed to help individuals earn investment returns on spare electronic cash sitting in their Alipay wallets. It was an instant success. Some people moved money out of their bank accounts into the new fund to earn higher returns, drawing complaints from some lenders that Alipay was siphoning their deposits.

In 2014, Alipay, along with Alibaba’s other financial businesses, were folded into Ant Financial Services Group, the company now known as Ant Group.

For years, Mr. Ma largely managed to navigate Mr. Xi’s two seemingly contradictory goals: encouraging financial innovation and open markets to drive growth while keeping a rein on market forces to maintain control.

Ant’s big money-market fund became the world’s largest of its kind, with more than $250 billion under management by 2017. China’s securities regulator became concerned about the systemic risk the fund could create, and pressured it to shrink and lower its returns. Ant changed its strategy, letting rival money managers sell similar funds on Alipay to investors needing places to park their money, and its main fund shrank.

In 2017, China’s leadership revamped the country’s fragmented regulatory regime, which had often involved various regulators acting in isolation. It named Liu He, Mr. Xi’s top economic czar, head of a superregulator of sorts called the Financial Stability and Development Committee. One of its goals was to better coordinate actions by China’s various regulatory agencies.

Ant raised three rounds of private capital. By mid-2018, it was the world’s most valuable startup, worth $150 billion, based on the prices private investors had paid.

This year, deteriorating relations between the U.S. and China gave Mr. Ma an opportunity to win points with the ruling party. With Washington threatening to delist Chinese companies from U.S. stock markets, Beijing was eager to build up its own exchanges. Its securities regulators saw having a company such as Ant listed in both Shanghai and Hong Kong as a big endorsement of China’s markets.

Ant changed its name in the summer, dropping the words “Financial Services.” Shortly after, it announced plans to go public, right around the first anniversary of China’s Nasdaq-style Science & Technology Innovation Board, better known as the STAR Market. After Ant filed listing documents in Hong Kong and Shanghai, the stock exchanges and Chinese securities regulators moved quickly to green-light its IPO.

But trouble was brewing with banking regulators, who were growing concerned about the risk banks were taking on by lending to Ant’s customers online. Since the summer, a spate of government regulations, guidelines and notices were rolled out to contain potential risks from the growth of digital finance and microlending.

The world’s biggest stock sale proved extremely popular with large and small investors. Privately, however, some Ant employees were worried about potential regulatory changes that could hurt the company’s growth prospects, according to people familiar with the matter.

On Oct. 24, Mr. Ma took the stage at a financial forum in Shanghai attended by top regulators, politicians and bankers. He said Ant’s IPO was “a miracle,” being such a large deal taking place away from New York. Attendees included China’s Vice President Wang Qishan, central bank governor Yi Gang and some senior state-bank executives.

During his 21-minute speech, he criticized Beijing’s campaign to control financial risks. “There is no systemic risk in China’s financial system,” he said. “Chinese finance has no system.”

He also took aim at the regulators, saying they “have only focused on risks and overlooked development.” He accused big Chinese banks of harboring a “pawnshop mentality.” That, Mr. Ma said, has “hurt a lot of entrepreneurs.”

His remarks went viral on Chinese social media, where some users applauded Mr. Ma for daring to speak out. In Beijing, though, senior officials were angry, and officials long calling for tighter financial regulation spoke up.

After Mr. Xi decided that Ant’s IPO needed to be halted, financial regulators led by Mr. Liu, the leader’s economic czar, convened on Oct. 31 and mapped out an action plan to take Mr. Ma to task, according to the government officials familiar with the decision-making.

At a meeting of the Financial Stability and Development Committee headed by Mr. Liu, the group decided to “put all kinds of financial activities under regulation and treating the same businesses in the same way,” according to a government statement.

The decision was aimed squarely at Ant, the government officials said, and cleared the way for the pro-stability members of the group to dust off draft regulations they had been working on for a long time.

Among them was one regulating online microlending. With Mr. Xi’s blessing, the central bank and the banking regulator made the draft rule even tougher than previously conceived, according to the Chinese officials familiar with the decision-making. The new rule had a requirement that didn’t exist in previous drafts: Firms such as Ant would need to fund at least 30% of each loan it makes in conjunction with banks.

Ant’s Alipay platform has facilitated loans to numerous individuals in China. Its activities have recently drawn scrutiny from financial regulators, in part because banks fund many of the loans. The draft rules were published on Nov. 2, the same day Mr. Ma and a couple of his executives at Ant were summoned to a rare joint meeting with the central bank and the regulatory agencies overseeing banking, insurance and securities.

The next day, the Shanghai Stock Exchange suspended the Ant IPO, citing the meeting and changes in the regulatory environment. The China Securities Regulatory Commission, which previously signed off on the listings, now says it was a “responsible move” to protect investors and markets, as the regulation, once implemented, would severely limit Ant’s business scope and profitability.

Ant could try again to go public. Market participants believe it will reorganize its business units, rethink its business model and inform investors of additional risks. All this likely will mean that Ant’s lofty valuation will be cut when it tries to list again, and the company may not be able to raise as much money as it aimed for this round, analysts say.

If you are following eCommerce companies (not Retail Commerce such as Home Depot, Walmart, etc.) there are 11 publicly listed companies that I am following. Of those 8 have reported earnings as of Nov 12th. JD.com reports on Nov 16th, SEA limited reports on Nov 17th and Chewy on Dec 14th.

Click for larger view of EPS, Revenue, Estimates, Market Cap and Growth

Q3 2020 Earnings estimates and analysis

Companies tracked (ranked by market capitalization)

The top 5 takeaways from Q3 2020 earnings that I gathered

Covid has accelerated all eCommerce companies, but some are gaining more share than others.

Revenue growth for ETSY has been the highest so far at 128%, followed by Shopify at 96%. Alibaba has been growing slower, but that’s to be expected because of their large revenue base.

Earnings are growing faster for all

Surprisingly, except 2 companies (Chewy and Wayfair) all others turned a profit and the fastest earnings growth was seen from Pinduoduo (PDD) Etsy (ETSY) and Shopify (SHOP).

Valuations are deservedly rich thanks to EPS and Revenue Growth

The companies with the richest valuations are Pinduoduo (PDD), Mercado Libre (MELI) and Shopify (SHOP). ETSY is relatively cheap at 76 PE.

Stocks I would be adding to my portfolio are ETSY and consider JMIA / FTCH

ETSY’s valuation and growth are terrific. I am going to hold MELI and SHOP, but add to my ETSY holding. I would also keep Jumia (JMIA) and Farfetch (FTCH) in my watch list.

Stocks I would likely not add are Alibaba, Wayfair and Chewy

I think they are good companies, but have limited upside for a 6-12 month horizon given their growth relative to other eCommerce companies.

B Riley (NASDAQ: RILY) is a full financial services firm based in Los Angeles. The company through several subsidiaries helps companies & high net worth individuals, invest, raise money, acquire and sell companies.

I would buy between $27 and $29, hold for 3-6 months on EPS growth long term.

There are five operating segments: (i) Capital Markets, (ii) Auction and Liquidation, (iii) Valuation and Appraisal, (iv) Principal Investments – United Online and magicJack, and (v) Brands.

Capital Markets segment provides a full array of investment banking, corporate finance, consulting, financial advisory, research, securities lending, wealth management and sales and trading services to corporate, institutional and high net worth clients.

Auction and Liquidation segment utilizes our significant industry experience, a scalable network of independent contractors and industry-specific advisors to tailor our services to the specific needs of a multitude of clients, logistical challenges and distressed circumstances.

Valuation and Appraisal segment provides Valuation and Appraisal services to financial institutions, lenders, private equity firms and other providers of capital.

Principal Investments – United Online and magicJack segment consists of businesses which have been acquired primarily for attractive investment return characteristics.

Brands segment consists of our brand investment portfolio that is focused on generating revenue through the licensing of trademarks.

The stock went public on Oct 2019.

They focus principally on five target industries in the investment banking operations: consumer goods, consumer services, defense, industrials and technology.

Fundamentals: Key metrics

Market Cap: $876Million

PE:19

EPS Growth 2019: 41%

Institutional Ownership: 48%

Sales growth Q/Q: 25%

EPS growth Q/Q: 43.9%

52 Week L $12.94 & 52 Week Hi $31.00

Current price: $30.0

Technical Key Metrics:

Support: $27, Resistance: $31

Moving Averages: EMA (50) – $19.91, and EMA (20) – $23.51

I am trying to learn as much as I can about technical analysis and came across a good introductory book on Stock market technical analysis.

First step guide to technical analysis

I would highly recommend you reading this book if you are interested in technical analysis of stock price & volume action. I would give his eBook a 4/5.

Fundamental Analysis

Fundamental analysis focuses on the intrinsic value of the market. If market price is below the intrinsic value, then the market is undervalued and should be bought or vice versa.

The intrinsic value of the business enterprises is estimated as the present value of the assets of these enterprises and the ‑ow of future dividends to be paid by these enterprises to shareholders. The fundamental analysis is good for selection of securities to be invested and not good for catching the timing of buying and selling.

Technical Analysis

Technical analysis concentrates on the study of market supply and demand. Technical analysis focuses on the movement of the prices and the trade volume and tries to forecast the future movement of the prices. Technical analysis concentrates on the change of the prices, and therefore you would know the timing of buying and selling, but not on the intrinsic value, and therefore you would not know whether you were properly investing.

Overview

Among the various methods of technical analyses, this booklet is following three methods, i.e., Candlestick Charts, Trendlines, and Moving Averages.

Candlestick charts are one of the price recording methods developed in Japan but widely used globally, which indicate the current market situation at all times, though the charts pick up only the figures of the open, the close, the high, and the low.

Trendlines and Moving Averages are the methods used to understand the major tendency of price change, namely, the trend. These methods of analysis are widely known as Trend Analysis. Trend analysis has been used from older times but has become popular only in the last half a century.

Candlestick charts

First, draw the verticalline from the highest price to the lowest during a day.

Then, draw the rectangle shape from the open price to the close price over the above vertical line. And if the close price is higher than the open price, this rectangle shape is shown in white and if the open is higher, it is shown in black.

Candlestick example

This white line is called “the sunny line” and black line “the shadow line”.

The length of the real body tells us the strength of the momentum of both seller and buyer. When the buyers are stronger, they keep buying and the white real body becomes longer, and when the sellers are stronger, they keep selling and the black becomes longer.

The unusual long big real body is appearing occasionally once a month or two months, when the movement becomes 2 to 3% of the price (the usual average movement is around 1%.).

The long real body and the short shadow simply tell us that most of the investors have followed the strong movement of the price and show their momentum.

When both the real body and the shadow are short, it tells us that the momentum of selling and buying is almost equal or investors see the market on the sidelines with no clear direction, or nobody is interested in the current market and leave it as it is.

Trendlines

The word “Trend” means the direction of the price movement when you use this word as technical term for the market. In upward phase it is called “uptrend”. The continuous change to a certain direction is called “long-term trend”. The rapid and big change is called “strong trend”.

You must find out a broader perspective on a direction of the trend by having got rid of the trifle and unnecessary movements. One method to gain such a perspective is to draw a straight line which could suggest a certain trend and thus is called” Trendline”.

Trendlines – uptrend and downtrend

There are two trend lines. One is the uptrend line analyzing the uptrend and another is the downtrend line analyzing the downtrend. The uptrend line is sometimes called support line and the downtrend line is called resistance line.

The uptrend line is the extended line drawn from low milestone price to then the next low milestone price when the market is considered in the uptrend.

The downtrend line is the extended line drawn from high milestone price to the next high milestone price when the market is considered in the downtrend.

And when the actual stock price crosses under the uptrend line or crosses over the downtrend line, either case is considered the signal of the reversal point of the trend price.

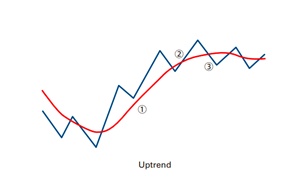

Uptrend

Uptrend

Line 1 drawn from A to B and extended

Line 2 drawn from C to D and extended

Line 3 drawn from D to E and extended

All lines are upward line. You can see the change of the pitch from Line 2 to Line 3 getting faster.

The point where the actual stock price crossed under Line 3 was the turning point of the reversal of uptrend which clearly shows that the 8 -year long rising market came to an end.

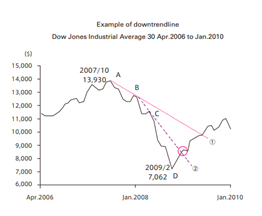

Downtrend

This average recorded the highest of US$13,930 on October 2007 and then came the 2008 financial crisis triggered by the bankruptcy of Lehman Brothers, and fell to US$7,062 on February 2009.

Downtrend

Line 1 drawn from A to B and extended

Line 2 drawn from B to C and extended was added because the pitch of falling became much faster.

The turning point of the stock price was the price just over the Line 2 and after that the price was rising tremendously. Especially, the time when the price crossed over Line 1, the market became more confident on the uptrend.

Trend continuity

The continuing uptrend means that the low price of turning point becomes higher than the low price of the previous turning point and simultaneously, the high price of turning point becomes higher than the high price of the previous turning point. This means that the both the low price and the high price of each turning point are rising.

Moving Averages

One of the methods to extract a trend after eliminating the trifle and meaningless change of the market is called “smoothing out” the unevenness of prices. You can eliminate such small changes by calculating an average of a certain period of the price data. The term moving is used because only the latest prices of specified time span are used in the calculation. This means that the period of price data to be averaged moves forward with each new trading day. And when you draw a line by connecting these averages, this line is, thus, called “Moving Average”. This “Moving Average” is sometimes abbreviated to MA.

While the trendline is basically drawn outside the change of the prices, the moving average is drawn over the change of the prices. The moving average is automatically drawn from the change of price and reflect automatically and successively the movement of the change of the prices without being influenced by drawers’ consideration. The moving average shows the trend of the change of the prices and is regarded as one of the trendlines in a broad sense.

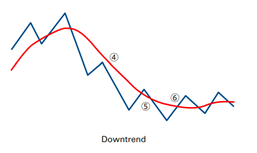

Uptrend

Vice versa, see no.4; if the moving average is falling from top left to bottom right, it means the downward trend.

See no.5; if the price crosses down through the falling moving average, this means the acceleration of paces of falling. See no.6; if the price crosses up through the moving average line, this means the slowing down of paces of falling.

After that, if the moving average line turns to upward-sloping, this means entering the upward trend.

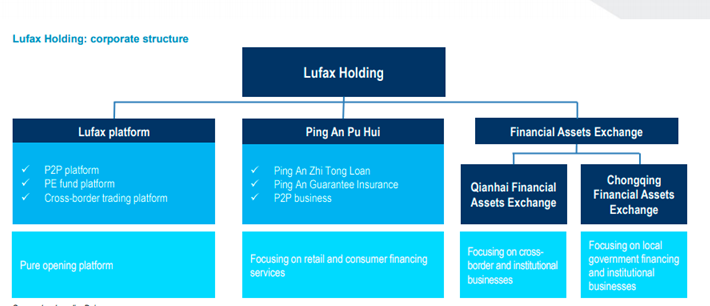

Since I mentioned Ant Financial a week ago, I thought I would take a look at another company in the FinTech space from China that is going public in the US – Lufax. They are looking to raise over $2 Billion with an expected valuation of over $50B. It was last valued at $38B a year ago.

Lufax

Lufax Holding is one of the largest fintech companies in China in terms of AUM. It mainly provides consumer finance and wealth management for individuals, and financial solutions for institutions and governments. Its fully-owned subsidiary, Lufax platform, is one of the largest online wealth management platforms in China.

It is looking to raise over $2.4 Billion and should list before Nov 2020.

Lufax Holding, now mainly comprises 4 business segments, Lufax platform, Ping An Pu Hui (Pu Hui), and the 2 financial asset exchanges, Qianhai (QEX) and Chongqing Financial Assets Exchange (CQFAX).

In their S1 filing there are a few interesting elements worth noticing.

Market

China has the second largest financial system globally, both by retail credit lending volume in 2019 and by the total amount of investable assets as of December 31, 2019. The estimated demand for small business financing in China was RMB89.7 trillion (US$12.7 trillion) in 2019, of which RMB46.6 trillion (US$6.6 trillion) was unmet.

The current outstanding balance of consumer loans in China is estimated to be RMB12.7 trillion (US$1.8 trillion) as of December 31, 2019. As of the same date, China’s personal investable assets reached RMB192 trillion (US$27 trillion), making it the second largest personal wealth management market globally, and only RMB49 trillion (US$7 trillion) or 26% has been placed in wealth management products.

Financials

Lufax Financials

They did about $6.7 Billion in revenue and $1.8B in profit for 2019, growing at -5% (Covid related) in Q2 2020.

Lufax platform is the largest P2P platform in terms of both outstanding balance and transaction volume of P2P loans in China.

Lufax platform had a total of 32.36m registered users, up 27% YoY while the number of active investor users rose by 17% YoY to 7.69m.

Pu Hui focuses on individual consumer financing and SME financing. It has 3 major businesses: Ping An Zhi Tong Loan, Ping An Guarantee, and the P2P business, which was injected into Pu Hui from Lufax platform in 1H15.

Pu Hui granted new loans of CNY257bn, up 130% YoY. The ending balance of loans under management at end-September 2017 rose by 141% YoY or 20% QoQ to CNY269bn. Pu Hui is now pushing ahead with an offline store innovation and online approval system upgrade to better underpin its outlet expansion in lower-tier cities, and optimize cost efficiency and user experience.

QEX and CQFAX mainly provide institutional financial asset trading services. QEX focuses more on cross-border business, while CQFAX focuses more on local government financing business and asset-fund matching among institutions.

I read the book by Nir Eyal to focus on building good discipline and focus. I would give this book a 2/5. It is a good book if you are unable to focus and get distracted all the time because of social media, news feeds, email and other activities.

Here is the summary and notes.

If you are not equipped to manage distraction, your brain will be manipulated by time-wasting diversions. According to the book, in the future, there will be two kinds of people in the world: those who let their attention and lives be controlled and coerced by others and those who proudly call themselves “indistractable.”

The antidote to impulsiveness is forethought. Planning ensures you will follow through.

Living the life, you want, requires not only doing the right things; it also requires we stop doing the wrong things that take us off track. Distractions impede us from making progress toward the life we envision.

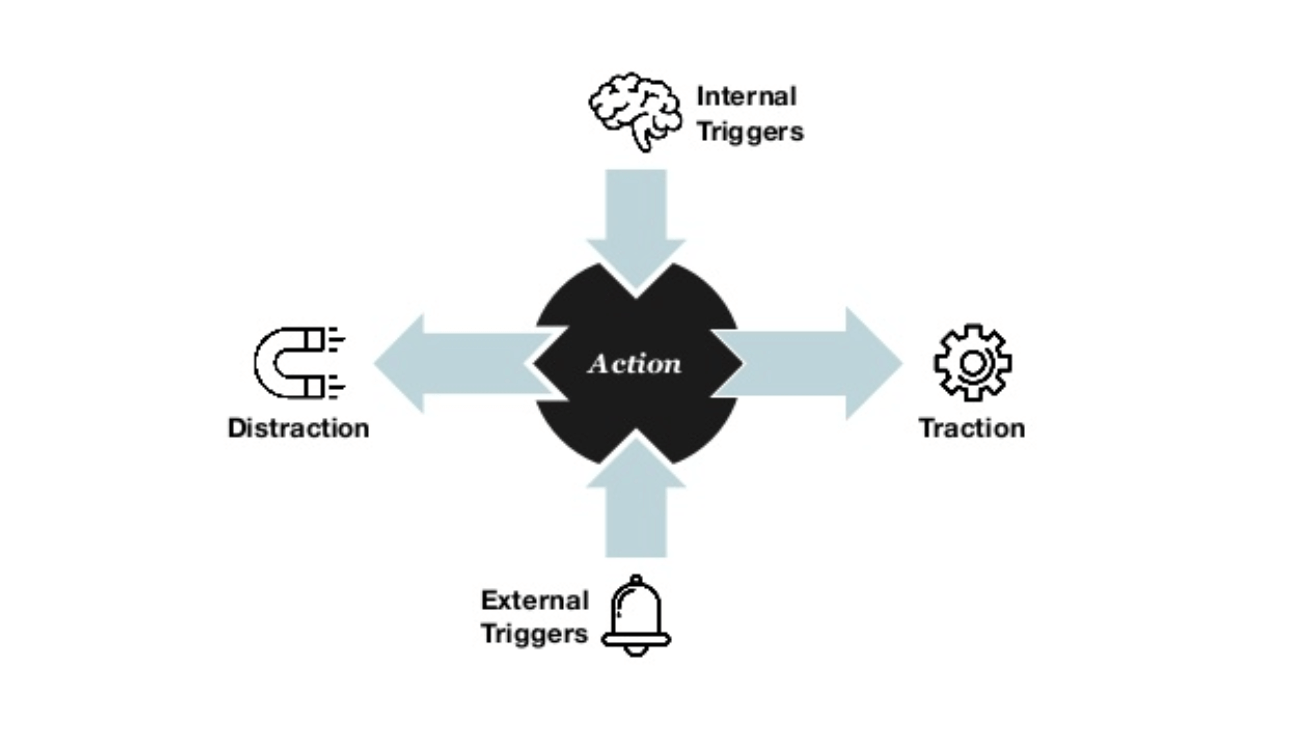

All behaviors, whether they tend toward traction or distraction, are prompted by triggers, internal or external.

Internal triggers cue us from within.

External triggers, on the other hand, are cues in our environment that tell us what to do next, like the pings, dings, and rings that prompt us to check our emails, open a news alert, or answer a phone call.

Being indistractable means striving to do what you say you will do.

Master Internal Triggers

Most people don’t want to acknowledge the uncomfortable truth that distraction is always an unhealthy escape from reality.

Understand the root cause of distraction. Distraction is about more than your devices. Separate proximate causes from the root cause.

• All motivation is a desire to escape discomfort. If a behavior was previously effective at providing relief, we’re likely to continue using it as a tool to escape discomfort.

• Anything that stops discomfort is potentially addictive, but that doesn’t make it irresistible. If you know the drivers of your behavior, you can take steps to manage them.

As is the case with all human behavior, distraction is just another way our brains attempt to deal with pain. If we accept this fact, it makes sense that the only way to handle distraction is by learning to handle discomfort.

Four psychological factors make satisfaction temporary.

Let’s begin with the first factor: boredom.

The second psychological factor driving us to distraction is negativity bias, “a phenomenon in which negative events are more salient and demand attention more powerfully than neutral or positive events.” Studies have found people are more likely to recall unhappy moments in their childhood.

The third factor is rumination, our tendency to keep thinking about bad experiences.

But a fourth factor may be the cruelest of all. Hedonic adaptation, the tendency to quickly return to a baseline level of satisfaction, no matter what happens to us in life, is Mother Nature’s bait and switch.

“Every desirable experience—passionate love, a spiritual high, the pleasure of a new possession, the exhilaration of success—is transitory.”

Dissatisfaction and discomfort dominate our brain’s default state, but we can use them to motivate us instead of defeating us. Dissatisfaction is responsible for our species’ advancements and its faults. It’s good to know that feeling bad isn’t bad; it’s exactly what survival of the fittest intended.

Time management is pain management

Distractions cost us time, and like all actions, they are spurred by the desire to escape discomfort.

• Evolution favored dissatisfaction over contentment. Our tendencies toward boredom, negativity bias, rumination, and hedonic adaptation conspire to make sure we’re never satisfied for long.

• Dissatisfaction is responsible for our species’ advancements as much as its faults. It is an innate power that can be channeled to help us make things better.

If we want to master distraction, we must learn to deal with discomfort. At the heart of the therapy is learning to notice and accept one’s cravings and to handle them healthfully. It turns out mental abstinence can backfire. Well-established techniques are effective at stopping physical dependencies to nicotine and other substances, then they can certainly help us control cravings for distraction.

Without techniques for disarming temptation, mental abstinence can backfire. Resisting an urge can trigger rumination and make the desire grow stronger. • We can manage distractions that originate from within by changing how we think about them. We can reimagine the trigger, the task, and our temperament.

STEP 1: LOOK FOR THE DISCOMFORT THAT PRECEDES THE DISTRACTION, FOCUSING IN ON THE INTERNAL TRIGGER.

STEP 2: WRITE DOWN THE TRIGGER

STEP 3: EXPLORE YOUR SENSATIONS

STEP 4: BEWARE OF LIMINAL MOMENTS

Liminal moments are transitions from one thing to another throughout our days.

A technique I’ve found particularly helpful for dealing with this distraction trap is the “ten-minute rule.” Every time you have a craving, you need to wait just ten minutes.

“Surfing the urge.” When an urge takes hold, noticing the sensations and riding them like a wave—neither pushing them away nor acting on them—helps us cope until the feelings subside.

They recondition our minds to seek relief from internal triggers in a reflective rather than a reactive way.

By reimagining an uncomfortable internal trigger, we can disarm it.

• Step 1. Look for the emotion preceding distraction.

• Step 2. Write down the internal trigger.

• Step 3. Explore the negative sensation with curiosity instead of contempt.

• Step 4. Be extra cautious during liminal moments.

“We fail to have fun because we don’t take things seriously enough, not because we take them so seriously that we’d have to cut their bitter taste with sugar. Fun is not a feeling so much as an exhaust produced when an operator can treat something with dignity.”

“The cure for boredom is curiosity. There is no cure for curiosity.” Today, I write for the fun of it. Of course, it’s also my profession, but by finding the fun I’m able to do my work without getting as distracted as I once did.

Fun is looking for the variability in something other people don’t notice. It’s breaking through the boredom and monotony to discover its hidden beauty.

The last step in managing the internal triggers that can lead to distraction is to reimagine our capabilities.

We can master internal triggers by reimagining an otherwise dreary task. Fun and play can be used as tools to keep us focused.

• Play doesn’t have to be pleasurable. It just must hold our attention.

• Deliberateness and novelty can be added to any task to make it fun.

The way we perceive our temperament, which is defined as “a person’s or animal’s nature, especially as it permanently affects their behavior,” has a profound impact on how we behave.

The study claimed that participants who had sipped sugar-sweetened lemonade demonstrated increased self-control and stamina on difficult tasks.

People who did not see willpower as a finite resource did not show signs of ego depletion. Ego depletion is essentially caused by self-defeating thoughts and not by any biological limitation. Willpower is not a finite resource but instead acts like an emotion. Just as we don’t “run out” of joy or anger, willpower ebbs and flows in response to what’s happening to us and how we feel. individuals who believed they were powerless to fight their cravings were much more likely to drink again.

Self-compassion makes people more resilient to letdowns by breaking the vicious cycle of stress that often accompanies failure.

Instead of accepting what the voice says or arguing with it, remind yourself that obstacles are part of the process of growth. We don’t get better without practice, which can be difficult at times. A good rule of thumb is to talk to yourself the way you might talk to a friend.

We can cope with uncomfortable internal triggers by reflecting on, rather than reacting to, our discomfort. We can reimagine the task we’re trying to accomplish by reimagining our temperament to help us manage our internal triggers.

• We don’t run out of willpower. Believing we do makes us less likely to accomplish our goals by providing a rationale to quit when we could otherwise persist. What we say to ourselves matters. Labeling yourself as having poor self-control is self-defeating.

• Practice self-compassion. Talk to yourself the way you’d talk to a friend. People who are more self-compassionate are more resilient.

Traction draws you toward what you want in life, while distraction pulls you away.

The trouble is, we don’t make time for our values.

You can’t call something a distraction unless you know what it’s distracting you from.

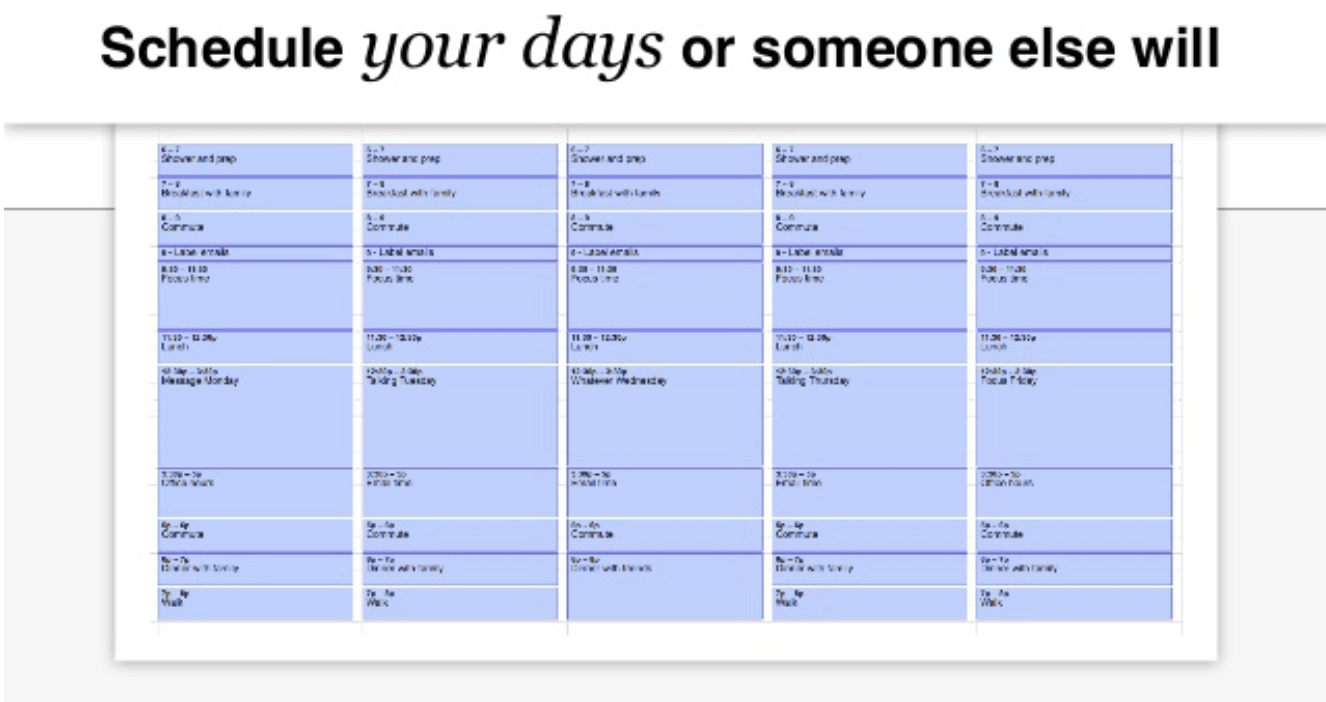

The most effective way to make time for traction is through “timeboxing.”

Is your schedule filled with carefully timeboxed plans, or is it mostly empty? Does it reflect who you are? Are you letting others steal your time or do you guard it as the limited and precious resource it is?

You can’t call something a distraction unless you know what it is distracting you from.

Planning is the only way to know the difference between traction and distraction.

• Does your calendar reflect your values? To be the person you want to be, you must make time to live your values.

• Timebox your day. The three life domains of you, relationships, and work provide a framework for planning how to spend your time.

• Reflect and refine. Revise your schedule regularly, but you must commit to it once it’s set.

The one thing we control is the time we put into a task.

Schedule time for yourself first.

You are at the center of the three life domains. Without allocating time for yourself, the other two domains suffer.

• Show up when you say you will. You can’t always control what you get out of time you spend, but you can control how much time you put into a task.

• Input is much more certain than outcome. When it comes to living the life you want, making sure you allocate time to living your values is the only thing you should focus on.

Family and friends help us live our values of connection, loyalty, and responsibility.

The people we love most should not be content getting whatever time is left over. Everyone benefits when we hold time on our schedule to live up to our values and do our share. This is how friendships die—they starve to death.

The people you love deserve more than getting whatever time is left over. If someone is important to you, make regular time for them on your calendar.

• Go beyond scheduling date days with your significant other. Put domestic chores on your calendar to ensure an equitable split.

• A lack of close friendships may be hazardous to your health. Ensure you maintain important relationships by scheduling time for regular get-togethers.

Using a detailed, timeboxed schedule helps clarify the Keep a central trust pact between employers and employees.

Syncing your schedule with stakeholders at work is critical for making time for traction in your day. Without visibility into how you spend your time, colleagues and managers are more likely to distract you with superfluous tasks. • Sync as frequently as your schedule changes. If your schedule template changes from day to day, have a daily check-in. However, most people find a weekly alignment is sufficient.

It’s time for us to hack back. In tech speak, “to hack” means “to gain unauthorized access to data in a system or computer.” Similarly, our tech devices can gain unauthorized access to our brains by prompting us to distraction.

External triggers often lead to distraction. Cues in our environment like the pings, dings, and rings from devices, as well as interruptions from other people, frequently take us off track.

• External triggers aren’t always harmful. If an external trigger leads us to traction, it serves us. • We must ask ourselves: Is this trigger serving me, or am I serving it? Then we can hack back the external triggers that don’t serve us.

Interruptions lead to mistakes. You can’t do your best work if you’re frequently distracted.

• Open-office floor plans increase distraction. • Defend your focus. Signal when you do not want to be interrupted. Use a screen sign or some other clear cue to let people know you are indistractable.

Book outline and summary of each chapter

Overview

Chapter 1: Living the life you want requires not only doing the right things but also avoiding doing the wrong things.

Chapter 2: Traction moves you toward what you really want while distraction moves you further away. Being indistractable means striving to do what you say you will do.

PART 1: Master Internal Triggers

Chapter 3: Motivation is a desire to escape discomfort. Find the root causes of distraction rather than proximate ones.

Chapter 4: Learn to deal with discomfort rather than attempting to escape it with distraction.

Chapter 5: Stop trying to actively suppress urges—this only makes them stronger. Instead, observe and allow them to dissolve.

Chapter 6: Reimagine the internal trigger. Look for the negative emotion preceding the distraction, write it down, and pay attention to the negative sensation with curiosity rather than contempt.

Chapter 7: Reimagine the task. Turn it into play by paying “foolish, even absurd” attention to it. Deliberately look for novelty.

Chapter 8: Reimagine your temperament. Self-talk matters. Your willpower runs out only if you believe it does. Avoid labeling yourself as “easily distracted” or having an “addictive personality.”

PART 2: Make time for traction

Chapter 9: Turn your values into time. Timebox your day by creating a schedule template.

Chapter 10: Schedule time for yourself. Plan the inputs and the outcome will follow.

Chapter 11: Schedule time for important relationships. Include household responsibilities as well as time for people you love. Put regular time on your schedule for friends.

Chapter 12: Sync your schedule with stakeholders.

PART 3: Hack back external triggers

Chapter 13: Of each external trigger, ask: “Is this trigger serving me, or am I serving it?” Does it lead to traction or distraction?

Chapter 14: Defend your focus. Signal when you do not want to be interrupted.

Chapter 15: To get fewer emails, send fewer emails. When you check email, tag each message with when it needs a reply and respond at a scheduled time.

Chapter 16: When it comes to group chat, get in and out at scheduled times. Only involve who is necessary and don’t use it to think out loud.

Chapter 17: Make it harder to call meetings. No agenda, no meeting. Meetings are for consensus building rather than problem solving. Leave devices outside the conference room except for one laptop.

Chapter 18: Use distracting apps on your desktop rather than your phone. Organize apps and manage notifications. Turn on “Do Not Disturb.”

Chapter 19: Turn off desktop notifications. Remove potential distractions from your workspace.

Chapter 20: Save online articles in Pocket to read or listen to at a scheduled time. Use “multichannel multitasking.”

Chapter 21: Use browser extensions that give you the benefits of social media without all the distractions. Links to other tools are at: NirAndFar.com/ Indistractable.

PART 4: Prevent distraction with pacts

Chapter 22: The antidote to impulsiveness is forethought. Plan for when you’re likely to get distracted.

Chapter 23: Use effort pacts to make unwanted behaviors more difficult.

Chapter 24: Use a price pact to make getting distracted expensive.

Chapter 25: Use identity pacts as a precommitment to a self-image. Call yourself “indistractable.”

PART 5: How to make your workplace indistractable

Chapter 26: An “always on” culture drives people crazy.

Chapter 27: Tech overuse at work is a symptom of dysfunctional company culture. The root cause is a culture lacking “psychological safety.”

Chapter 28: To create a culture that values doing focused work, start small and find ways to facilitate an open dialogue among colleagues about the problem.

PART 6: How to raise indistractable children (and why we all need psychological nutrients)

Chapter 29: Find the root causes of why children get distracted. Teach them the four-part indistractable model.

Chapter 30: Make sure children’s psychological needs are met. All people need to feel a sense of autonomy, competence, and relatedness. If kids don’t get their needs met in the real world, they look to fulfill them online.

Chapter 31: Teach children to timebox their schedule. Let them make time for activities they enjoy, including time online.

Chapter 32: Work with your children to remove unhelpful external triggers. Make sure they know how to turn off distracting triggers, and don’t become a distracting external trigger yourself.

Chapter 33: Help your kids make pacts and make sure they know managing distraction is their responsibility. Teach them that distraction is a solvable problem and that becoming indistractable is a lifelong skill.

PART 7: How to have indistractable relationships

Chapter 34: When someone uses a device in a social setting, ask, “I see you’re on your phone. Is everything OK?”

Chapter 35: Remove devices from your bedroom and have the internet automatically turn off at a specific time.

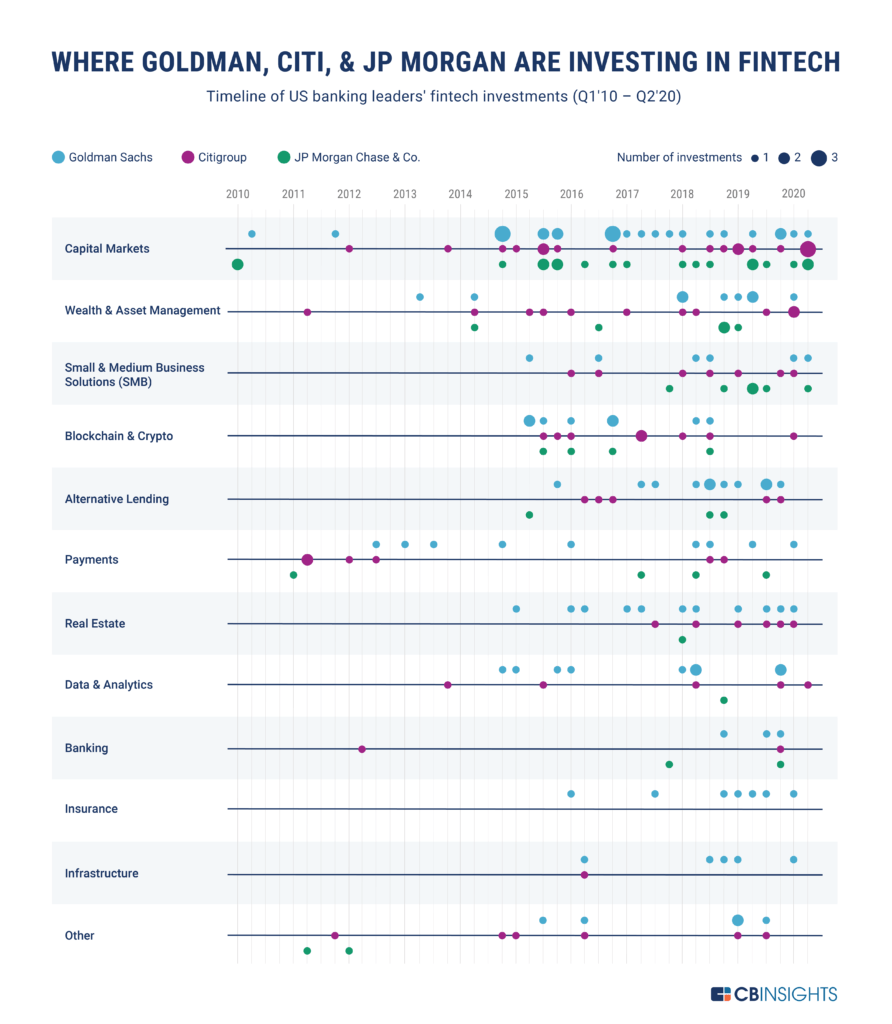

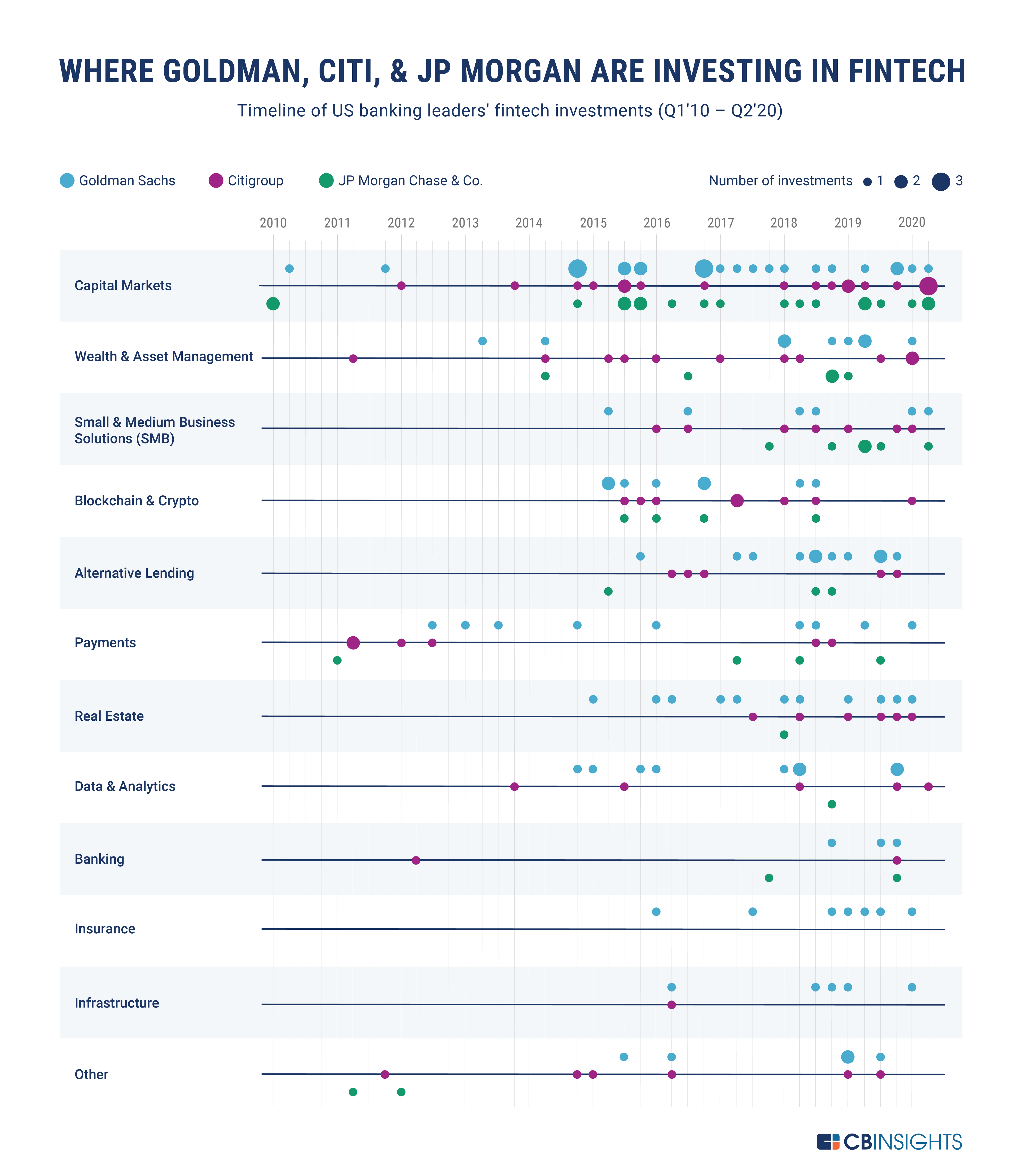

There are over 18,000 companies(2) worldwide in the fintech category. FinTech (or Finance Technology) comprises of startups and companies innovating the business of money. In the last decade, there has been over $250 Billion in investments made in this space. (1)

The subsectors within FinTech

The investments from the big organizations reflect the size o these markets – payments and capital markets are the largest (includes investments, loans, etc.).

Daniel Pink – Drive – what motivates us besides rewards and basic desires

I had a chance to re-read this book. It is about motivation – intrinsic motivation which is the desire to learn, grown and thrive. I would give this book a 3/5. It is pretty good in the theory and outline, but short on specifics.

Scientists then knew that two main drives powered behavior.

The first was the biological drive. Humans and other animals ate to satiate their hunger, drank to quench.

If biological motivations came from within, this second drive came from without— the rewards and punishments the environment delivered for behaving in certain ways.

The performance of the task, provided intrinsic reward. Perhaps this newly discovered drive or “intrinsic motivation”—was real.

When money is used as an external reward for some activity, the subjects lose intrinsic interest for the activity.

Rewards can deliver a short-term boost—just as a jolt of caffeine can keep you cranking for a few more hours. But the effect wears off—and, worse, can reduce a person’s longer-term motivation to continue the project.

Intrinsic Motivation

Human beings, have an “inherent tendency to seek out novelty and challenges, to extend and exercise their capacities, to explore, and to learn.”

One who is interested in developing and enhancing intrinsic motivation in children, employees, students, etc., should not concentrate on external- control systems such as monetary rewards.

Daniel Pink

The book has 3 parts.

Part One will look at the flaws in our reward-and-punishment system and propose a new way to think about motivation.

Part Two will examine the three elements of Type I behavior and show how individuals and organizations are using them to improve performance and deepen satisfaction.

Part Three, the Type I Toolkit, is a comprehensive set of resources to help you create settings in which Type I behavior can flourish. Here you’ll find everything from dozens of exercises to awaken motivation in yourself and others.

Part One – A New Operating System

Enjoyment-based intrinsic motivation, namely how creative a person feels when working on the project, is the strongest and most pervasive driver. Economics was the study of human economic behavior. We leave lucrative jobs to take low-paying ones that provide a clearer sense of purpose.

Work consists mainly of simple, not particularly interesting, tasks. The only way to get people to do them is to incentivize them properly and monitor them carefully.

External rewards and punishments—both carrots and sticks—can work nicely for algorithmic tasks. The best use of money as a motivator is to pay people enough to take the issue of money off the table. In other words, rewards can perform a weird sort of behavioral alchemy: They can transform an interesting task into a drudge. They can turn play into work.

People use rewards expecting to gain the benefit of increasing another person’s motivation and behavior, but in so doing, they often incur the unintentional and hidden cost of undermining that person’s intrinsic motivation toward the activity.

Algorithmic (following a set path) but heuristic. Study of artists over a longer period shows that a concern for outside rewards might hinder eventual success.

Goals that people set for themselves and that are devoted to attaining mastery are usually healthy. But goals imposed by others—sales targets, quarterly returns, standardized test scores, and so on—can sometimes have dangerous side effects.

Like all extrinsic motivators, goals narrow our focus.

The problem with making an extrinsic reward the only destination that matters is that some people will choose the quickest route there, even if it means taking the low road.

Indeed, most of the scandals and misbehavior that have seemed endemic to modern life involve shortcuts.

The Seven Deadly Flaws

1. They can extinguish intrinsic motivation.

2. They can diminish performance.

3. They can crush creativity.

4. They can crowd out good behavior.

5. They can encourage cheating, shortcuts, and unethical behavior.

6. They can become addictive.

7. They can foster short-term thinking.

Carrots and sticks aren’t all bad. If they were, Motivation 2.0 would never have flourished so long or accomplished so much.

The assignment neither inspires deep passion nor requires deep thinking. Offer a rationale for why the task is necessary. Acknowledge that the task is boring. Allow people to complete the task their own way.

Autonomous, self-determined, and connected to one another. And when that drive is liberated, people achieve more and live richer lives.

Part 2 – The Three Elements

3 elements that drive us – Autonomy, Mastery, Purpose

Autonomy

“The ultimate freedom for creative groups is the freedom to experiment with new ideas. Some skeptics insist that innovation is expensive. In the long run, innovation is cheap. Mediocrity is expensive—and autonomy can be the antidote.”

TOM KELLEY General Manager, IDEO

Type I behavior emerges when people have autonomy over the four T’s: their task, their time, their technique, and their team.

Mastery

“Try to pick a profession in which you enjoy even the most mundane, tedious parts. Then you will always be happy.”

WILL SHORTZ Puzzle guru

Purpose

Nine Strategies for Awakening Your Motivation

Remember that deliberate practice has one objective: to improve performance.

Repeat, repeat, repeat. Repetition matters.

Seek constant, critical feedback

Focus ruthlessly on where you need help.

Prepare for the process to be mentally and physically exhausting.

Praise effort and strategy, not intelligence. As Dweck’s research has shown, children who

Make praise specific.

Praise in private.

Offer praise only when there’s a good reason for

Summary

When it comes to motivation, there’s a gap between what science knows and what business does. Our current business operating system— which is built around external, carrot-and-stick motivators—doesn’t work and often does harm. We need an upgrade. And the science shows the way. This new approach has three essential elements:

(1) Autonomy—the desire to direct our own lives

(2) Mastery—the urge to make progress and get better at something that matters; and

(3) Purpose—the yearning to do what we do in the service of something larger than ourselves.

Ant Financial is a financial services company that was previously a part of Alibaba. Ant recorded about $17B in revenue last year and about $1.7B in profit. In March 2020 alone they profited over $1.3B, a 560% increase over last year. Alibaba owns about 33% of Ant.

Ant Financial

The company is planning to go public in Hong Kong sometime in November 2020. It is expected to raise more than $30B. With a forward price-to-earnings multiple of 40, in line with big global payments companies, Ant could fetch a market capitalization in excess of $300B, more than any bank in the world. There are 4 business lines that Ant makes money from – payments, loans, insurance and asset management (mostly mutual fund investment services).

The company’s latest annual total consisted of RMB 51.9 billion ($7.6B) in digital-payments revenue (Payments) and RMB 41.9 ($6.1B) billion in credit-technology (Loans) revenue. Ant added RMB 8.9 billion ($1.3B) in revenue from insurance technology (Insurance) and RMB 17 billion ($255M) from investment technology (Mutual Funds).

Alipay was rebranded as Ant Group Services on 23 October 2014, and the company changed its name to Ant Group Co., Ltd on 13 July 2020.

Market

There are over 3.4 Billion bank accounts (3.1 B payment, 300 M credit cards) in China. Widespread use of Ant Financial started via QR Codes and on eCommerce marketplaces in China – Taobao, Tmall, JD.com and others.

Products

Alipay (payments, similar to PayPal) was introduced by Alibaba group in 2004. This payment app competes with WeChat payments (owned by Tencent). That is now Ant payments.

Alipay and WeChat own about 84% of the entire third-party payment market in China. Alipay is the largest (51%), WeChat (33%) as of 2016.

The organization has expanded beyond mobile wallet Alipay to include an online lending platform, MyBank, and an investment fund, Yu’e Bao. In June 2018, Ant Financial introduced the world’s first cross-border remittance network based on blockchain.

Yu’e Bao has become the largest money market fund in the world, with over 400M users and $211B assets under management today. Ant claims 116 — nearly all — of China’s mutual fund asset management companies sell products on Ant Fortune to its 180M users.

392M users annually use Ant’s insurance marketplace to find thousands of products sold by over 80 Chinese insurance companies. Like Ant Fortune, Ant’s insurance services also see strong margins, charging insurers tech and service fees to be featured in its marketplace.

Source – Financial Times

Consumers paying with Alipay also start borrowing from it. Alipay arranges small loans to consumers and small businesses and earns a service fee from the lender tied to the loan balance. Last year 500 M customers took a loan from Ant. This business is growing at 80% YoY.

Ant introduced its Yu’E Bao fund in 2013, allowing customers to invest the piles of cash growing in their Alipay accounts.

Source: The Economist

Lending

In lending, Ant offers three major financing services: Ant Micro-Loan: The credit loan service arm of Ant’s private commercial bank, MyBank. The platform provides micro-credit loans to small businesses in China and issued loans to 3M applicants by mid-2016. JieBei: A consumer credit loan service for Ant users with high Sesame Credit scores (600+). JieBei claims to hand out, on average, 3000 yuan (roughly $440 USD) to consumers each month, driving consumption on Alibaba’s shopping marketplaces. Huabei: Ant Check Later, was launched in April 2015 to allow users to buy items with credit with no-interest installment repayment. HuaBei claimed 80M active users at the end of 2016.

Ant has put an emphasis on the impact artificial intelligence has in driving its loan success.

Credit Scoring

Launched in 2015, Sesame Credit (or Zhima Credit) provides a private credit scoring and loyalty program system using data from Alibaba’s services to compile its score. China lacks a reliable credit system like FICO in the US. Sesame provides its consumer and business users with a score from 350 to 950 and may be used in China’s forthcoming social credit system.

In January 2018, Ant was punished for automatically enrolling users into its credit rating system and, a month later, Sesame Credit stopped servicing unlicensed financial businesses, including certain banks, consumer finance companies, and online microlenders.

Today, Sesame is largely used for non-financial purposes, such as credit checks for bike rentals and visa approvals. Ant portfolio company Hellobike, for example, offers a deposit-free bikeshare service in 180+ cities for users with a 650+ Sesame Credit score.

Ant as a fintech platform

One of the key tenets of Ant’s strategy is its focus on providing an open platform for existing financial institutions to leverage Ant’s technology and tap into new users. As it shifts its revenue focus away from primarily financial services, Ant is prioritizing the tech services it provides to banks, asset management companies, and insurers.

Ant doesn’t need to rely on payments for profitability if it can use payments as a gateway into its financial services ecosystem, where it charges financial institutions tech and service fees with high margins.

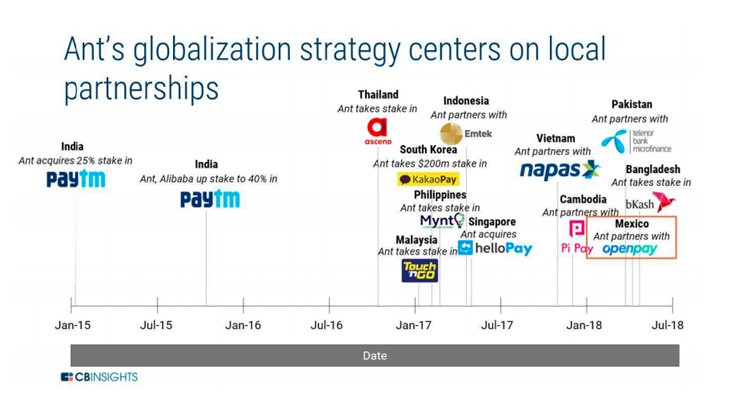

Ant has global ambitions

Looking to the longer term, Ant is focused on expanding its presence globally to drive growth. Ant’s globalization strategy to date has focused on striking partnerships and making minority investments with local partners.

Southeast Asia, in particular, has been a major focus as Ant hopes to link its technology into partners across markets including Thailand, India, Indonesia, and the Philippines and Latin America.

Ant Financial has global ambitions with investments and stakes in multiple regional fintech companies

Investing in Ant Financial

If you want to buy shares in Ant, and you are in the US, you have to open an account with Interactive Brokers or Schwab. All the other brokers do not offer Hong Kong market access.

New Fintech Ecosystems

Source: Goldman Sachs Report on Fintech Ecosystems

The world over, Fintech (Finance technology) has been a segment of growth – from Asia and US to Europe and Africa. New disruptive companies such as Plaid (acquired by VISA) and Robinhood are challenging incumbents such as traditional banks, insurance companies and lenders.

Ant is among the largest and earliest fintech compaines.

{kind=link}