The NASSCOM startup survey of state of funding in India was out today. PDF below.

The most important part of the report are the rise in Unicorns, There are 68 startups with over One billion in valuation.

The NASSCOM startup survey of state of funding in India was out today. PDF below.

The most important part of the report are the rise in Unicorns, There are 68 startups with over One billion in valuation.

Ken Wilcox’s The China Business Conundrum: Ensure That “Win-Win” Doesn’t Mean Western Companies Lose Twice offers a firsthand account of the complexities and systemic challenges faced by foreign enterprises operating in China. Drawing from his four-year tenure establishing Silicon Valley Bank’s (SVB) joint venture in Shanghai, Wilcox provides a cautionary narrative that blends personal anecdotes, cultural analysis, and strategic insights. This report synthesizes the book’s core themes, including the Chinese Communist Party’s (CCP) influence, cultural mismatches, regulatory labyrinths, and the paradox of “win-win” partnerships.

At the heart of Wilcox’s account is the concept of One Bed, Two Dreams—a metaphor for the inherent misalignment between Western companies seeking market access and Chinese partners aiming to acquire intellectual property or replicate business models. SVB’s joint venture with Shanghai Pudong Development Bank (SPDB) exemplified this dynamic. Chinese officials initially lauded SVB as more strategically valuable than Goldman Sachs or Morgan Stanley, framing the partnership as critical to China’s innovation ecosystem. However, Wilcox later realized the CCP’s true objective was to dissect SVB’s tech-lending model and transfer its methodologies to state-backed banks.

The CCP’s involvement permeates all business operations. For example, joint ventures must establish Party committees that often function as shadow boards, overriding formal governance structures. Wilcox recounts how SPDB’s chairman—a CCP member—viewed his roles in government, the Party, and the bank as indistinguishable, creating opacity in decision-making. This intertwining of Party and business interests ensures that foreign ventures ultimately serve China’s national objectives, even at the expense of their own profitability.

Cultural misunderstandings frequently derailed SVB’s efforts. A critical misstep arose from SVB’s assumption that corporate titles mirrored Western norms. Wilcox, as president, believed he held operational control, while his Chinese counterpart, the chairman, viewed the role as ceremonial. In reality, the chairman wielded executive authority, leading to clashes over strategic decisions. This disconnect underscores the risks of transplanting Western mental models into China’s distinct hierarchy-driven culture.

Building guanxi (relationship capital) is essential but fraught with ethical dilemmas. SVB faced pressure to offer “special favors”—such as bribes disguised as commissions—to secure deposits from state-owned enterprises18. While Wilcox resisted, he acknowledges that such practices are normalized in China’s relationship-based economy. Similarly, SVB employees often held side jobs at insurance firms, cross-selling products to banking clients—a conflict of interest unacceptable in Western contexts but tacitly accepted in China.

China’s regulatory environment proved Kafkaesque. SVB’s joint venture required over 20 licenses to replicate its U.S. operations, including separate approvals for deposit accounts, loans, and currency exchanges. Despite years of negotiations, critical licenses—such as renminbi (RMB) clearance—remained elusive, crippling the bank’s ability to operate. Wilcox highlights a paradoxical workaround: renting licenses from other banks, a common but legally dubious practice in China.

Regulatory delays often served strategic purposes. For three years, Chinese authorities withheld approval for SVB to use RMB, citing nebulous “policy concerns.” Wilcox argues this stalling tactic allowed domestic banks to study SVB’s methods while limiting its competitive reach. Even after securing licenses, daily reporting requirements and sudden regulatory shifts—such as bans on subletting licenses—hamstrung operations.

Xi Jinping’s ascent in 2012 marked a turning point. His anti-corruption campaign, while popular, intensified Party scrutiny over businesses. SVB’s joint venture faced heightened pressure to align with Xi’s “Chinese Dream” of technological self-reliance. The CCP’s grip extended to staffing: SVB was compelled to hire “sons and daughters of the Party”—relatives of officials—who prioritized political loyalty over merit.

Under Xi, foreign firms encountered escalating demands to share proprietary data. SVB’s risk-assessment algorithms, a trade secret, were repeatedly requisitioned under the guise of regulatory compliance. Wilcox warns that such practices are systematic: foreign companies are tolerated until their intellectual property is absorbed, after which domestic competitors receive state support to supplant them.

Wilcox dispels the myth of China as a “market economy.” Success requires accepting that the CCP will always prioritize national interests over partnership equity. Contracts, while necessary, hold limited enforceability; MOUs and guanxi often prove more pivotal.

Wilcox’s narrative is a sobering antidote to the “China dream” rhetoric. The CCP’s playbook—luring foreign firms with market access, extracting knowledge, and sidelining them—remains pervasive under Xi. Yet, China’s market size necessitates engagement. The key lies in tempered pragmatism: leveraging China’s ecosystem while safeguarding core IP and diversifying risk.

For Western executives, The China Business Conundrum is indispensable. It transcends SVB’s story, offering a blueprint for resilience in an era of techno-nationalism and strategic rivalry. As Wilcox concludes, “In China, ‘win-win’ demands recognizing that the Party always wins first—your task is to ensure you don’t lose twice”.

The journey of a startup is marked by distinct stages, each with critical milestones and metrics that measure progress and guide decision-making. These stages—early, growth, and late—are defined by specific goals that reflect the startup’s evolution from an idea to a scalable, sustainable business.

The early stage focuses on transforming an idea into a viable product or service. Key milestones include developing a Minimum Viable Product (MVP), launching it to the market, and achieving proof of concept. Metrics like customer acquisition cost (CAC), activation rate, and initial revenue generation are crucial here. For instance, attracting the first 10, 100, or 1,000 customers validates product-market fit and demonstrates demand[1][2][7].

During this phase, startups must also monitor burn rate to ensure they manage limited resources effectively. Achieving early traction through marketing campaigns and customer feedback is essential for refining the product and building credibility with stakeholders[2][3]. Positive customer feedback, Net Promoter Score (NPS), and low churn rates signal that the product addresses real market needs[7].

Once a startup validates its concept, the focus shifts to scaling operations. This stage involves expanding the customer base, increasing revenue, and optimizing financial health. Key milestones include securing Series A funding, hiring additional team members, and entering new markets[5][6]. Metrics like Monthly Recurring Revenue (MRR), user engagement (e.g., Daily Active Users), and conversion rates become critical indicators of growth[3][7].

Startups at this stage should aim to achieve financial stability by breaking even or exceeding their debt service ratio by at least 20%[4]. Efficiently managing cash flow while maintaining a healthy burn rate ensures sustainability. Additionally, building strong customer retention strategies helps maximize Customer Lifetime Value (CLV) and reduces reliance on constant acquisition efforts[3].

In the late stage, startups focus on achieving profitability, optimizing operations, and preparing for potential exit strategies like IPOs or acquisitions. Milestones include reaching significant revenue targets (e.g., $1 million annually), expanding into international markets, or launching complementary products[4][5]. Metrics such as profitability ratios, operational efficiency, and market share growth are essential for evaluating success.

At this stage, balancing growth with profitability becomes paramount. Startups must demonstrate consistent revenue streams while maintaining a manageable burn rate to attract investors for late-stage funding rounds or strategic partnerships[3][6]. Additionally, planning for an exit strategy requires aligning operations with long-term goals and ensuring scalability.

Each stage of a startup’s lifecycle is defined by unique milestones and metrics that reflect its progress toward sustainability. From validating an idea in the early stage to scaling in the growth phase and achieving maturity in the late stage, these checkpoints provide a roadmap for success. By tracking key performance indicators at every step, founders can make informed decisions that align with their vision while adapting to market demands.

Sources

[1] Early Stage Startup Revenue Milestones and Metrics – 10k Per Month https://tehcpa.net/early-stage-startup-revenue-milestones-and-metrics-10k-per-month/

[2] Business Milestones that Signify Growth – Mailchimp https://mailchimp.com/resources/business-milestones/

[3] Measuring Progress in Early Stage Startups: Key Metrics for Success https://www.linkedin.com/pulse/measuring-progress-early-stage-startups-key-metrics-success-nqgdf

[4] Financial Milestones That Prepare You for Startup Success https://www.nw.bank/blog-detail/blog/2024/08/13/financial-milestones-that-prepare-you-for-startup-success

[5] What are the three stages of a startup? | Silicon Valley Bank https://www.svb.com/startup-insights/startup-growth/what-are-the-three-stages-of-a-startup/

[6] Beyond Product-Market Fit: The Startup Milestones Every Founder … https://techstartups.com/2024/11/24/beyond-product-market-fit-the-startup-milestones-every-founder-must-know/

[7] Key Performance Indicators (KPIs) Startup Metrics Every Early-Stage … https://www.taxfyle.com/blog/early-stage-startup-metrics

[8] Eight Successful Startup Milestones Every Founder Should … – Forbes https://www.forbes.com/councils/forbesbusinessdevelopmentcouncil/2021/06/25/eight-successful-startup-milestones-every-founder-should-be-striving-toward/

Comprehensive Summary of Chip War: The Fight for the World’s Most Critical Technology by Chris Miller| Published October 4, 2022

Introduction: The Geopolitical Stakes of Semiconductors

Introduction: The Geopolitical Stakes of SemiconductorsChris Miller’s Chip War positions semiconductors—tiny silicon chips that power modern electronics—as the linchpin of global economic and military power. The book argues that control over semiconductor technology defines 21st-century geopolitics, akin to oil in the 20th century. Miller traces the industry’s evolution from its origins in Cold War-era innovation to today’s U.S.-China rivalry, emphasizing how these chips underpin everything from consumer gadgets to advanced weaponry .

The narrative opens with a stark illustration of Taiwan’s centrality: Taiwan Semiconductor Manufacturing Company (TSMC) produces 37% of the world’s computing power, making the island a geopolitical flashpoint. China’s dependence on foreign chips (spending more on imports than oil) and U.S. efforts to restrict China’s access to advanced technology frame the book’s central conflict .

Miller concludes that semiconductors are both a triumph of globalization and its Achilles’ heel. The U.S.-China rivalry will shape the industry’s future, with Taiwan at the epicenter. Key takeaways:

Chip War serves as a cautionary tale: the tiny silicon chip, once a symbol of progress, now holds the power to destabilize economies and ignite conflicts. As Miller writes, “The world’s dependence on Taiwan only deepens”—a reality demanding urgent geopolitical foresight .

Comprehensive Summary of The 5 Types of Wealth

By Sahil Bloom

Sahil Bloom’s The 5 Types of Wealth challenges the societal fixation on financial wealth as the sole measure of success. Drawing from interviews with elderly individuals (collectively representing 1,042 years of lived experience), scientific research, and personal anecdotes, Bloom argues that true wealth encompasses five interconnected dimensions: Time, Social, Mental, Physical, and Financial Wealth . The book’s central thesis is: “Your wealthy life may be enabled by money, but in the end, it will be defined by everything else” .

Bloom’s journey began after the birth of his son, which shifted his perspective on time and legacy. He observed that none of the octogenarians he interviewed mentioned money as a source of lasting fulfillment. Instead, they emphasized love, relationships, health, and presence—themes that form the backbone of the book .

Definition: Control over how you spend your time, prioritizing moments that align with your values.

Key Insights:

Pillars:

Definition: Depth and quality of relationships, fostering connections that provide joy and support.

Key Insights:

Pillars:

Definition: Clarity of purpose, presence, and lifelong learning.

Key Insights:

Pillars:

Definition: Health and vitality through sustainable habits.

Key Insights:

Pillars:

Definition: Achieving “enough” to enable freedom without sacrificing other wealth types.

Key Insights:

Pillars:

Each chapter follows a framework designed for introspection and action:

Bloom integrates real-life stories, such as a tech founder’s post-exit emptiness and a retiree’s rediscovery of purpose through volunteering, to illustrate abstract concepts .

The 5 Types of Wealth is not a prescriptive self-help guide but a framework for intentional living. By rejecting society’s narrow definition of wealth, readers are empowered to design lives rich in time, love, health, purpose, and financial freedom. As Bloom writes: “When in doubt, love. The world can always use more love” .

The book’s strength lies in its blend of empathy, research, and practicality, making it a transformative read for anyone seeking holistic fulfillment

According to Einstein

Always write your thesis down. If it takes more than a short paragraph, there is a fundamental problem. If it requires me to fire up Excel, it is a big red flag that strongly suggests that I ought to take a pass.

Mohnish Pabrai

Notes and Quotes from The Dhando Investor – Mohnish Pabrai, published 2007, 209 pages.

There were virtually no Patels in the United States just 35 years ago. Less than one in five hundred Americans is a Patel. Over half of all the motels in the entire country are owned and operated by Patels.

Patels, as a group, today own over $40 billion in motel assets in the United States, pay over $725 million a year in taxes, and employ nearly a million people.

Dhan comes from the Sanskrit root word Dhana meaning wealth. Dhan-dho, literally translated, means “endeavors that create wealth.”

Dhandho is all about the minimization of risk while maximizing the reward.

If an investor can make virtually risk-free bets with outsized rewards, and keep making the bets over and over, the results are stunning.

The first few Patels arrived from Africa in the early 1970s. The reason we end up with concentrations of ethnic groups in certain professions is that role models play a huge role in how humans pick their vocations.

“Few Bets, Big Bets, Infrequent Bets.”

“Heads, I win; tails, I don’t lose much!”

The Dhando approach

We see change as the enemy of investments . . . so we look for the absence of change. We don’t like to lose money. Capitalism is brutal. We look for mundane products that everyone needs.1 —Warren Buffett

Never count on making a good sale. Have the purchase price be so attractive that even a mediocre sale gives reliable results. —Warren Buffett

The entrance strategy is more important than the exit strategy. —Eddie Lampert

Arbitrage is as an attempt to profit by exploiting price differences in identical or similar financial instruments.

Minimize downside risk before ever looking at upside potential.

This is not so much a book review as a summary of key quotes and my notes of the book “The psychology of money” by Morgan Housel

Financial outcomes are driven by luck, independent of intelligence and effort. Financial success is not a hard science. It’s a soft skill, where how you behave is more important than what you know. I call this soft skill the psychology of money. The aim of this book is to use short stories to convince you that soft skills are more important than the technical side of money.

To grasp why people bury themselves in debt you don’t need to study interest rates; you need to study the history of greed, insecurity, and optimism. To get why investors sell out at the bottom of a bear market you don’t need to study the math of expected future returns; you need to think about the agony of looking at your family and wondering if your investments are imperiling their future.

Be careful who you praise and admire. Be careful whom you look down upon and wish to avoid becoming.

Therefore, focus less on specific individuals and case studies and more on broad patterns.

You’ll get closer to actionable takeaways by looking for broad patterns of success and failure. The more common the pattern, the more applicable it might be to your life.

Nothing is as good or as bad as it seems.

The hardest financial skill is getting the goalpost to stop moving.

“Enough” is realizing that the opposite—an insatiable appetite for more— will push you to the point of regret.

There are a million ways to get wealthy, and plenty of books on how to do so. But there’s only one way to stay wealthy: some combination of frugality and paranoia.

Getting money requires taking risks, being optimistic, and putting yourself out there. But keeping money requires the opposite of taking risk. It requires humility, and fear that what you’ve made can be taken away from you just as fast. It requires frugality and an acceptance that at least some of what you’ve made is attributable to luck, so past success can’t be relied upon to repeat indefinitely.

More than I want big returns, I want to be financially unbreakable. And if I’m unbreakable I think I’ll get the biggest returns, because I’ll be able to stick around long enough for compounding to work wonders.

Planning is important, but the most important part of every plan is to plan on the plan not going according to plan.

A barbelled personality—optimistic about the future, but paranoid about what will prevent you from getting to the future—is vital.

“I’ve been banging away at this thing for 30 years. I think the simple math is, some projects work and some don’t. There’s no reason to belabor either one. Just get on to the next.” —Brad Pitt accepting a Screen Actors Guild Award

Anything that is huge, profitable, famous, or influential is the result of a tail event—an outlying one-in-thousands or millions event. And most of our attention goes to things that are huge, profitable, famous, or influential. When most of what we pay attention to is the result of a tail, it’s easy to underestimate how rare and powerful they are.

Money’s greatest intrinsic value—and this can’t be overstated—is its ability to give you control over your time. To obtain, bit by bit, a level of independence and autonomy that comes from unspent assets that give you greater control over what you can do and when you can do it.

Controlling your time is the highest dividend money pays.

Wealth is what you don’t see.

The first idea—simple, but easy to overlook—is that building wealth has little to do with your income or investment returns, and lots to do with your savings rate.

Past a certain level of income, what you need is just what sits below your ego.

Sunk costs—anchoring decisions to past efforts that can’t be refunded—are a devil in a world where people change over time.

“Every job looks easy when you’re not the one doing it” Jeff Immelt

Optimism is a belief that the odds of a good outcome are in your favor over time, even when there will be setbacks along the way.

The more you want something to be true, the more likely you are to believe a story that overestimates the odds of it being true.

Everyone has an incomplete view of the world. But we form a complete narrative to fill in the gaps.

If you want work flexibility you can

1. Work for a small company and get paid less. OR

2. Work for a large company and get paid well. But commute 3-4 days a week.

Notes from my discussions with multiple industry analysts and reading many reports.

There are multiple changes happening with autombiles:

The challenges:

In 2022, electric vehicles (EVs) took 11% global market

share (up from 6.5% in 2021), expecting 20% penetration by 2025

and the most aggressive for 100% by 2030.

Globally, we now expect battery electric vehicles (BEVs) to reach 40% penetration by 2030, and xEVs to reach 80% by 2035.

EV forecast calls for battery capacity to rise from ~600GWh in 2022 to 2,700GWh by end of 2030.

China has seen new energy vehicle (NEV) adoption become increasingly consumer-driven, with the country blowing past NEV penetration targets — the government sought to achieve ~20% penetration by 2025; it saw 23.5% in the first eight months of 2022. Chinese buyers seem to

favor domestic EVs over foreign (German and Japanese) brands though, leaving foreign OEMs potentially playing catch-up with domestic brands.

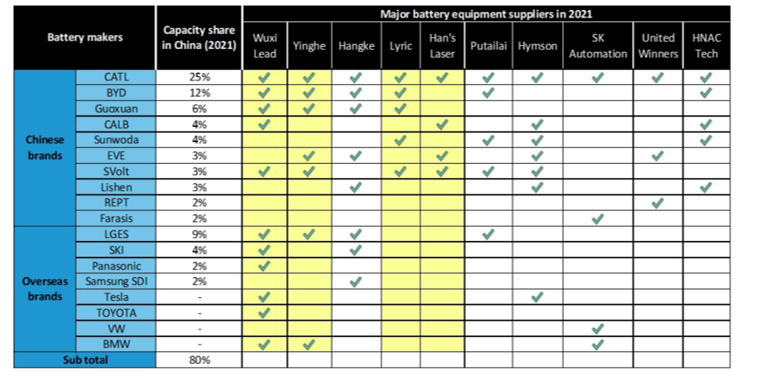

China represented close to 40% of the global battery

equipment market in 2021, up from 10%+ during 2016-19. Explosive growth over the past three years has been driven by sharply increasing investment in new energy industries.

Range anxiety over the switch from ICE to EVs has long been cited as a common impediment to greater EV adoption.