I am watching both Palantir $PLTR and Roblox $RBLX pretty closely to intiate new positions.

$RBLX – Roblox reported a 161% increase in quarterly bookings in the gaming platform company’s first report since going public. Roblox’s gaming activity surged amid the pandemic as more people played games like “Jailbreak” and “MeepCity,” and spent more of the company’s “Robux” digital currency for in-game purchases.

$RBLX

$RBLX posted a $0.46 per share loss on sales of $387M, +140% YoY. Daily active users (DAUs) jumped to 42.1M while users spent 9.7B hours on the platform, up 98% YoY.

$RBLX recorded $652.3 million in bookings, up 161% YoY while the average booking per daily active user was $15.48.

$RBLX managed to launch in China 6-12 months earlier than anticipated.

Roblox

There were some concerns that Roblox’s user growth trajectory would slow meaningfully in early 2021, as kids returned to school, sports, and playdates. That didn’t happen much.

Wall Street analysts believe $RBLX stock is worth roughly $80 today. $RBLX stock is a great long-term investment opportunity to play the “Digi-Everything” megatrend.

What I like about $RBLX is the differentiated segment of users and their increasing engagement (DAU). This company is a cash printing machine.

$PLTR Palantir Technologies – The data analytics company matched Wall Street forecasts with quarterly profit of 4 cents per share, while revenue topped estimates. It also said it expected annual revenue growth of 30% or more through 2025.

$PLTR

$PLTR revenue jumped 49% to $341.2M from $229.3M a year ago, well ahead of analysts’ forecasts of $332.2M.

$PLTR U.S. commercial revenue grew 72% year over year, while U.S. government revenue grew 83%.

$PLTR posted a first-quarter loss of $123.5 million, or 7 cents a share, vs. a loss of $54.3 million, or 10 cents a share, in the comparable year-earlier period.

$PLTR said during its earnings call that it will begin accepting bitcoin as a form of payment, and that it may begin holding the crypto on its balance sheet.

“If you take a look at our balance sheet there’s $2.3 billion in cash at quarter-end including $151 million in cash flow in Q1. So it’s definitely on the table from a treasury perspective as well as other investments as we look across our business and beyond,”

CFO David Glazer

Average revenue per customer grew to $8.1M. In its fourth quarter report, the company said average revenue for 2020 came to $7.9M. As of this past quarter, Palantir has 149 customers.

For Q2 2021 $PLTR expects revenue of $360M, +43% YoY, and adjusted operating margin of 23%. For the full year, it expects adjusted free cash flow “in excess of $150M” and annual revenue growth of 30% or greater for 2021 through 2025.

Valuation-wise $PLTR is expensive. The shares trade at about 130X forward looking earnings and at nearly $35B in Market Capitalization about 28X 2021 revenue.

What I like about $PLTR is revenue growth is increasing, commercial customer growth is better (compared to government). The #BTC on balance sheet is interesting, but not very meaningful to my thesis.

$FIGS (Figs Inc) filed to go public last week. The company sells Medical apparel (Scrubs) to professionals online. It is looking to raise about $100M in the IPO, and seeking a valuation of $3.5B to $4B. The final pricing of the stock and expected valuation will be confirmed by June 2021.

FIGS scrubs

$FIGS was founded in 2013 and has raised $75M+ in funding so far. The company did $263M (+131% YoY) in revenue for 2020, with net income of $49M, compared to $112 the year ago.

The founders saw a chance to innovate a sleepy market by using fabrics that were sleek, lightweight, and breathable and by selling direct to consumer, a model that was popularized by Warby Parker.

Its direct-to-consumer (DTC) strategy enables $FIGS to “engage with the medical community of health care professionals before, during and after purchase.”

FIGS co founders and co-CEOs Trina Spear and Heather Hasson

The founders received Ernst and Young Entrepreneur of the Year Award for the Greater Los Angeles Region in 2018 and $FIGS has been a Fast Company “most innovative” company” award winner for years.

Market

For the over 19M healthcare workers in the U.S. (BLS) as of 2017, $FIGS offers stylish (meaning better fit, not loose or baggy), antimicrobial, odor-free and wrinkle-free designs of apparel (called Scrubs).

FIGS Scrubs

Until the late 1980s, scrubs were a business-to-business industry, when hospitals bought on behalf of their staff. Then, budgets were constrained and the hospitals stopped buying them. Doctors and nurses were left picking up the tab.

Medical apparel is now a $10B industry here in the U.S., and a $60B industry worldwide.

Product

$FIGS introduced its direct-to-consumer model with $60-and-up prices, innovative styles and a Silvadur-treated antimicrobial, wrinkle-resistant and odor-free fabric.

$FIGS scrubs retail for $84 / full set — costing multiple times what typical scrubs do, which range from about $10 to $60. But unlike regular scrubs, they’ll last longer as long as they don’t get stained is the company’s claim.

$FIGS scrubs are made with “proprietary fabric technology, called FIONx, (that) offers four-way stretch, anti-odor, anti-wrinkle and moisture-wicking properties,” along with “easy-to-access zippered pockets” to store stethoscopes, scissors, smartphones or ID badges. Designs, fashion and fit are the differentiators as well as materials the Scrubs are made of.

It also sells lifestyle and professional apparel, such as lab coats, outerwear, activewear, loungewear, compression socks, footwear, masks and face shields.

Go to market

Since $FIGS is DTC, they market and sell directly using advertising & social media (Instagram) as their primary vehicle to attract customers. FIGS has cultivated influencers (called ambassadors) who promote its products on social media.

Figs billboards advertise the scrubs with pithy sayings and images that make doctors and nurses look like fashion models.

Medical professionals are advertised as fashion models by FIGS

The hashtag #wearfigs is a rapidly populating stream of posts, with percentage coming from Figs’ official roster of 200 ambassadors who receive free scrubs.

$FIGS Instagram page has over 500K followers showcasing customers—primarily women, who make up 70% of Figs’s customer base—in brightly lit settings, far from the mayhem of an emergency room.

FIGS Instagram page

In 2019 the company also opened a pop-up store in LA.

Awards

Between 2015 and 2018, FIGS reported 9,948% growth, being recognized as Best for the World B-Corp in 2015, as well as ranked Number 21 on Inc. Magazine’s Inc. 5000 ranking of the U.S. fastest-growing companies in 2018.

Competition

$FIGS competes with Strategic partners, Jaanuu and others in this $10B market.

Strategic Partners (SPI), a company that launched in 1995, has been selling in bulk to brick and mortar stores . It is the largest scrubs maker in the world with 40% of the US market via brands like Dickies and Cherokee.

SPI generates about $900M in sales and controls about 40% of the market.

Jaanuu, sells scrubs that look like they could have just come off a runway. Jaanuu was founded in 2013 by Dr. Neela Sethi Young and her brother, private equity investor Shaan Sethi.

Metrics

Last year, Figs’ community of active consumers grew from 600,000 to about 1.3 million, and about 60% were repeat shoppers.

The company’s sales got a boost from the Covid-19 pandemic, during which more hospitals, medical offices and clinics were requiring staff to wear clean scrubs and other medical apparel daily.

Operations

$FIGS has 202 employees and an embroidery workshop and fulfillment center in California, that is operated by a third-party logistics provider. It sources the majority of the fabrics used in its products from two suppliers in China, while other raw materials, such as content labels, elastics, buttons, clasps and drawcords, come from suppliers located predominantly in the Asia-Pacific region.

The company outsources its garment manufacturing operations to factories in Southeast Asia, China and South America.

Risks

$FIGS has benefited from Covid growth, which may taper off. However, the cost of customer acquisition has come down significantly and time to profitable customer is the 1st order.

$FIGS has been accused by Strategic Partners Inc. (SPI) that its business plan was derived from a 300-page confidential report that co-founder Trina Spear filched when she worked as a marketing associate for Blackstone, the private equity company.

SPI — which manufactures and sells scrubs for brands such as Cherokee, Dickies, Elle and Disney — alleges that Spear accessed the company’s business secrets.

SPI, which is owned by private equity firm New Mountain Capital Group, contends Spear shared that information with business partner Hasson and even bragged about it at an event last year in an interview that was posted on YouTube.

There are multiple class action lawsuits on the marketing of its products as “anti-microbial” as well from individual consumers.

$FIGS has been on the receiving end of a poorly executed Ad campaign which accuse the company of being insensitive and stereotyping medical professionals.

The company targets medical students and recent medical college graduates with significant student loans but does not offer financial compensation for their marketing work, instead giving a free pair of scrubs with a suggestion that modeling for FIGS would result in social media popularity.

After addressing the video, FIGS co-founders Heather Hasson and Trina Spear apologized for publishing the video, which they said was “offensive” and “particularly disparaging” to women in medicine.

FIGS – video ad

Valuation

While DTC (direct-to-consumer) peers such as $HNST (Honest Company), $CSPR (Casper Mattress), $PRPL (Purple Innovation) and $STIC / $BARK (Barkbox) are still trading at low (2.5X to 5X 2021 EV/ Revenue) multiples, $FIGS is expecting a 7X – 10X multiple, which makes it expensive.

With 60%+ gross margins, 100% YoY growth and profitable business, however, it is likely to get enough buyers.

FIGS Comparable Multiples and Valuation

Recommendation

Of the multiple new IPO’s, I like $FIGS, since it is similar to $STIC / $BARK – high 60% margins, good growth and profitable.

I will, however wait for a few months to see their execution as a public company before I initiate a position.

$WDH Waterdrop Inc., the Chinese insurance technology company will IPO on May 13th at $10-$12/share raising about $360M, valuing the company at about $4.5B.

$WDH is backed by Tencent $TCEHY which has also backed SEA Limited $SE, Futu Holdings $FUTU among other companies.

Waterdrop distributes insurance policies online and provides illness crowd-funding.

China’s online insurance market, may grow to as much as 2.5 trillion yuan ($387B) in a decade, growing at 16% CAGR, according to China International Capital Corp.

$WDH insurance crowdfunding has more than 70 million users as of 2019 and paid out almost 2 billion yuan to members.

Waterdrop has 2 units – Waterdrop Insurance Marketplace and Medical Crowdfunding.

The company helps those who face significant medical cost conduct crowdfunding campaigns. More than 340 million people donated 37 billion yuan to 1.7 million-plus patients as of the end of last year.

It lost $169M last year on revenues of $464M (+111% YoY). It had $162.8M in cash before the IPO.

The biggest challenges are pending regulatory changes that could halt key operations to prolonged losses if it spends for expansion. Chinese regulators already attempted to block the listing, according to Reuters.

Goldman Sachs (Asia) LLC, Morgan Stanley & Co. LLC and BofA Securities, Inc. are acting as the representatives of the underwriters.

$WDH was founded in 2016, by founder, Chairman and CEO Peng Shen, who was previously a founding team member of Meituan Waimai, a food delivery service in China.

Founder, Peng Shen

Waterdrop has received $741M in investment from investors including Neptune Max, Image Frame Investment, Boyu Capital, Gaorong Capital, and Swiss Re.

$WDH has 62 insurance carriers offering 200 different types of health and life insurance products on its platform

At 10X LTM (but 100%+ growth) and increasing losses, the valuation is very rich compared to recent IPOs of Insure Tech companies in the US – $LMND Lemonade, $OSCR Oscar Health, $ROOT Root Insurance and $RTPZ Hippo Insurance.

$OG Onion Global is a China based online fashion eCommerce marketplace. The company will list on May 11th selling shares at $7.25/share raising about $67.5M at about $600M Market Cap.

$OG management is headed by founder and CEO Cong (Kenny) Li, who was previously founder of another e-commerce company, Hua Ning, and worked at Procter & Gamble China and Nike China.

$OG has received at least $128M from investors including Li Bai Global, Pingsan Bai, YGC Holdings, and ECSH Xianlv Limited.

$OG fresh, fashionable and future brands, which it refers to as the 3Fs across China and parts of Asia.

$OG has about 500K consumers who are influencers, over 2.1M active buyers on the platform & 15.5M registered consumers. They also have more than 4K brands in 24 product categories.

The fashion market they are targeting is a subset of the apparel market focused on influencer-based marketing and is about $18B in Asia Pacific.

$OG had $584M in revenue (+41% YoY) at a Gross Margin of 20%, and grew gross profits 51% YoY to $119M. The operating margin was $39M (+6.7% YoY).

$OG has $40M in cash and will raise another $67M with $6M in Free cash flow for 2020.

At $600M Market cap and $40M in Operating margin they seem reasonably valued, relative to $CPNG, $FTCH and $SE, but $OG has much lower margins.

Recommendation

While I think this is an interesting company with a good brand, I am personally not buying shares at the IPO and have no interest until I see growth in other regions. Fashion as an eCommerce segment has tremendous competition in China as well.

$LYFT $53.48 (-5% on 5/5) slid down after Q1 revenue of $609M (+12% QoQ) and adjusted EBITDA of($73M) – +15% QoQ.

$LYFT believes it can be adjusted EBITDA breakeven by Q2 2021, because of cost cutting measures it adopted post Covid, even with 35% less rides than in 2020.

$LYFT had lower drivers mostly due to Covid vaccinations and federal unemployment benefits, but is seeing ride volume rebound – especially to airports (+65% April relative to Jan).

$LYFT Positives: a) Increased Revenue per active rider (+0.2%) to $45.13 b) Lower costs leading to profitability and c) New offerings in B2B delivery.

$LYFT Negatives: a) Gross margins lower (-4%) thanks to Covid insurance, b) Growth is not as strong as $UBER

Analyst Updates

Deutsche Bank raises PT (Price Target) to $75

Stifel raised PT to $60

Credit Suisse raised PT to $76

Barclays raised PT to $60

Nomura raised PT to $63

Morgan Stanley raised PT to $70

Metrics

Active riders in Q1 went to 13.49M (-36% YoY)

Revenue per active rider in Q1 went to $45.13 (+0.2%)

Recommendation

I dont have a position in $LYFT but see $UBER as a better risk / reward at this point, and will wait until $UBER reports earnings end of day 5/5.

$FLYW Flywire a payment tech company filed to go public privately.

$FLYW Flywire is a global payments company that attracted more than $300M as a startup, most recently raising a $60M in April 2021.

The expected valuation is $3B. $FLYW is looking to raise $100M in its IPO.

The Boston-based company, which was founded in 2011 by Iker focuses on payments in the education, healthcare and travel sectors. The company was initially formed in July 2009 as peerTransfer Corp., but changed its name to Flywire in December 2016.

$FLYW recorded $44.99M in revenue for the three months ended March 31, up from $32.71M in the same period a year ago.

Flywire is working with Goldman Sachs Group Inc and JPMorgan Chase & Co on the listing, which could come as early as July 2021.

$FLYW has processed more than $16B in transactions and employs more than 550 people. Flywire CEO Mike Massaro is focused on growing the company in the education space & travel.

The company processes payments in more than 240 countries and territories worldwide and said it offers over 250 payment methods to its 2,250-plus clients.

2019 calendar year, the company generated revenue of $94.9M and losses of $20.1M.

$FLYW revenue grew to $131.8 million (+39%) with a net loss of $11.1 million (+45%).

Flywire powers more than 50 leading U.S. hospitals and health system & Processes $14 B in patient transactions, representing more than ⅓ of U.S. households.

In Feb 2020, Flywire acquired Simplee, a healthcare technology platform, to optimize the digital payments and patient engagement experience in healthcare and scale its global payments services.

Global payments revenue is expected to grow at a 5.9% CAGR from 2019-2028 to become a $2.5T industry by 2028.

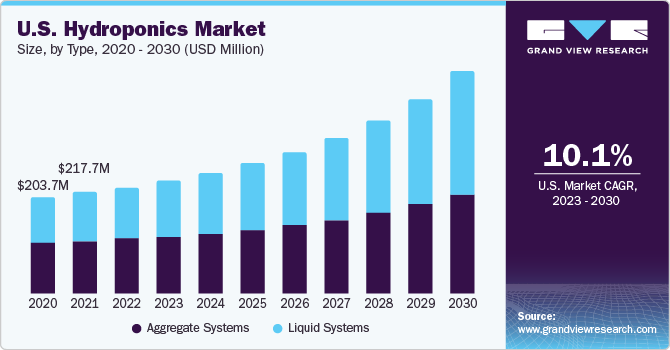

$IPW iPower runs and operates zenhydro.com, an online eCommerce store for Hydroponics equipment and other indoor farming and Agricultural products. They sell their products via $AMZN Amazon, $WM WalMart, $EBAY eBay and other online distribution channels.

$IPW is going to list on NASDAQ on May 6th 2021. They are looking to raise about $50M, pricing 5M shares at about $10 (mid point of range $9-$11). The issue is being managed by D. A. Davidson.

$IPW – At that price they will be valued at about $220M, giving them a EV/Revenue multiple of 5.25 and EV/EBIDTA of 53 for a company growing at 75% YoY.

iPower sells 26K 3rd party products (via partnerships with 100 suppliers) and its own private label products to indoor farming enthusiasts and professional growers (marijuana, microgreens, etc.)

The company grew revenues 75% in 2020 to $40M with net income of $2M. Revenue in 2019 was $26M and net income was $1M.

The company has its own fulfilment center in California and has been very capital efficient, raising less than $3.5M to date.

$IPW iPower was founded in 2010 by CEO Chenlong (Lawrence) Tan, but only recently (2018) changed its name and legal entity to iPower.

In 2020 $IPW product sales mix includes: Nutrients such as fertilizers, (17%), Ventilation systems (16%), Grow light systems (9%), Air filter devices (8%) and Trimmers (4%) among other products.

They also sell their own private label brands iPower and Deluxe for ventilation and lighting.

What is Hydroponics?

Hydroponics is a method of gardening in which plants are grown in a controlled environment with lighting sources and an optimized mix of nutrients and water, instead of soil.

Roots of the plants are submerged in water giving them direct access to nutrients resulting in efficient growth.

Since hydroponics can be grown indoors, plants are protected from weather, pests and chemicals.

How large is the Hydroponics market?

Hydroponics is largely used to grow micro greens, cannabis & other vegetables. The global hydroponics market is about $9.5B in 2020, growing at 5% CAGR to $18B by 2026.

The growth is driven by indoor growing of year-round hothouse vegetables in small batches, as well at large growth in cannabis.

How well has iPower executed?

$IPW iPower has executed its growth very well, with strong top line revenue growth of 75% during Covid, gross margins of 38%-41% and net income of $1+M.

$IPW Monthly revenue has grown from mostly 3rd party product sales (lower margin) to private-label products (higher margin).

How does $IPW distribute its products?

$IPW operates its own website (zenhydro.com) but also sells on $AMZN (Amazon.com) as a 3rd party seller, as well as listing on Walmart $WMT and eBay $EBAY.

In 2020 $AMZN business grew 87% YoY, with 62 listed products on the Amazon marketplace and 5 best selling SKU.

The manage their own logistics and fulfillment center near Los Angeles, California from where they ship and distribute products.

Why are they growing so quickly?

Covid growth in eCommerce is pushing their short term growth trends. There are 2 customer segments – small residential gardens and small commercial cultivators – who focus on Vertical farming.

They have a good mix of products and growth has been driven by Cannabis sales due to Covid in 2020.

Who are the competitors?

Over 200 hydroponics equipment makers and distributors exist in the US alone, with the large ones being Aerofarms, Freight Farms and LumiGrow.

What are the risks and concerns?

There are 5 major concerns I have:

2020 growth was driven by Covid and movement from offline purchases to online. Will that be sustained?

Of the 170 reviews for the store, their rating is 1.7 / 5, which is very low. Most of the reviews are about poor customer service and delayed product shipments. However their $AMZN store reviews are terrific, so I am not sure why they seem to have issues with direct fulfillment.

There is one employee lawsuit pending in LA court which is still ongoing but not disclosed in the SEC filing.

The company’s sole founder has majority of the Class A stock which have 10:1 voting rights representing 96.53% of voting power.

75% of sales are via 3rd party platforms such as $AMZN and $WMT. If this slows or if the platforms cause issues, revenue is going to drop quickly.

What is the recommendation?

$IPW As with all IPO I would watch $IPW for 3-6 months before I take a serious position. The superficial numbers and growth look good and I like the valuation, but Covid growth concerns and poor customer reviews give me pause.

Here are some memorable quotes from the book “The Heart of Buddha’s Teaching” by Thich Nhat Nahn

Transforming Suffering into Peace, Joy and Liberation

The book is terrific and I highly recommend it. I am on a goal to read one book a month on self improvement, philosophy and spirituality. If this summary is helpful, drop me a line on twitter.

When one tree in the garden is sick, you have to care for it. But don’t overlook all the healthy trees. Even while you have pain in your heart, you can enjoy the many wonders of life.

To me this is about being grateful and appreciating things even during the depths of despair. Don’t ignore your suffering, but don’t forget to enjoy the wonders of life, for your sake and for the benefit of many beings.

You cannot choose to be austere alone. You cannot choose to be indulgent alone. The middle way of moderation gives you the balance.

The four noble truths and eight fold path

The First Noble Truth is suffering (dukkha).

We all suffer to some extent. We have to recognize and acknowledge the presence of this suffering and touch it. To do so, we may need the help of a teacher and a Sangha, friends in the practice.

The Second Noble Truth is the origin, roots, nature, creation, or arising (samudaya) of suffering.

After we touch our suffering, we need to look deeply into it to see how it came to be.

The Third Noble Truth is the cessation (nirodha) of creating suffering by refraining from doing the things that make us suffer.

The Third Truth teaches us that healing is possible.

The Fourth Noble Truth is the path (marga) that leads to refraining from doing the things that cause us to suffer.

The 8 fold path

Right View,

Right Thinking,

Right Speech,

Right Action,

Right Livelihood,

Right Diligence,

Right Mindfulness, and

Right Concentration.

Habits to cultivate:

Stopping

Calming

We have to learn the art of stopping the suffering.

We can stop by practicing mindful breathing, mindful walking, mindful smiling, and deep looking in order to understand.

We have to learn the art of breathing in and out, stopping our activities, and calming our emotions.

To calm our body and mind we can adopt the 5 stages.

(1) Recognition — If we are angry, we say, “I know that anger is in me.” (2) Acceptance — When we are angry, we do not deny it. We accept what is present. (3) Embracing — We hold our anger in our two arms like a mother holding her crying baby. Our mindfulness embraces our emotion, and this alone can calm our anger and ourselves. (4) Looking deeply — When we are calm enough, we can look deeply to understand what has brought this anger to be, what is causing it. (5) Insight — The fruit of looking deeply is understanding the many causes and conditions primary and secondary that are causing it.

We have to learn the art of resting, allowing our body and mind to rest. If we have wounds in our body or our mind, we have to rest so they can heal themselves.

Calming allows us to rest, and resting is a precondition for healing.

Meditation does not have to be hard labor. Just allow your body and mind to rest like an animal in the forest. Don’t struggle. There is no need to attain anything.

If we are mindful, we will know whether we are “ingesting” the toxins of fear, hatred, and violence, or eating foods that encourage understanding, compassion, and the determination to help others.

Practicing mindfulness helps us learn to appreciate the well-being that is already there. With mindfulness, we treasure our happiness and can make it last longer.

The greatest miracle is to be alive. We can put an end to our suffering just by realizing that our suffering is not worth suffering for.

$FB Facebook reported Q1 EPS of $3.30 (+95% YoY), $0.93 better than the analyst estimate of $2.37

$FB Revenue for the quarter came in at $26.17B (+47% YoY) versus the consensus estimate of $23.67B.

$FB daily active users (DAUs) – DAUs were 1.88B on average for March 2021, (+8% YoY).

$FB monthly active users (MAUs) – MAUs were 2.85B as of March 2021 (+10% YoY).

$FB Ad rates and pricing rose 30% YoY driving strong revenue gains, which led 4 analysts to raise price targets to $380 – $400.

$FB is currently at $326

$FB is investing in the consumer shopping experience – with ~9% of total MAUs now interacting with merchandise, which can drive universal adoption of Shops and subsequently increase the shopping use case.

$FB disclosed that there 1M active shopping stores, 250M visitors to these stores.

$FB announced another $4B in share buybacks as well, likely raising EPS. $FB has $62B in cash with no debt.

A 12-month price target of $380 seems reasonable based on 24x 2022 GAAP EPS estimate plus cash, and implies ~16.0x ’22E Adjusted EBITDA.

New intiatives

“We have a long way to go to build out a full featured commerce platform across our services, and this is a multiyear journey. But I am very committed to getting there” – Mark Zuckerberg

“We’re looking forward to offering businesses a native way to manage their customer relationships on our platforms” – Mark Zuckerberg

“We’re rebuilding meaningful elements of our ad tech so that our system continues to perform when we have access to less data in the future (Apple IDFA)” — Sheryl Sandberg

$HNST Honest company, founded by Jessica Alba is going public next week on May 5th, expecting to raise $105M in cash at $14-$17 / share valuing the company at $1.4B to $1.8B.

$HNST sells Baby, Skin Care, and Wellness products online and via retail outlets. It was founded in 2012.

The company is a digital native company with a mission to make natural products with a green and clean footprint for the socially conscious consumer.

$HNST develops products in its in-house lab, and is transparent around how its products are made and what ingredients are put inside them.

Market

“Clean and Natural” segment is ~$17B per year in annual spend, and is a rapidly growing segment within a large consumer market for Baby, Skin care, and Wellness products (~$130B per year). 80% of this market is offline retail store. Honest is an omnichannel company with D2C (Direct to Consumer) & 30K store distribution through retail.

$HNST: Multiple changes in management and some challenging years (2017-2018) forced the company to go from a monthly subscription model to a regular à la carte retail model with non-Baby products approaching 40% of sales in 2020.

55% of sales come from online (mobile, web) and remaining from retail.

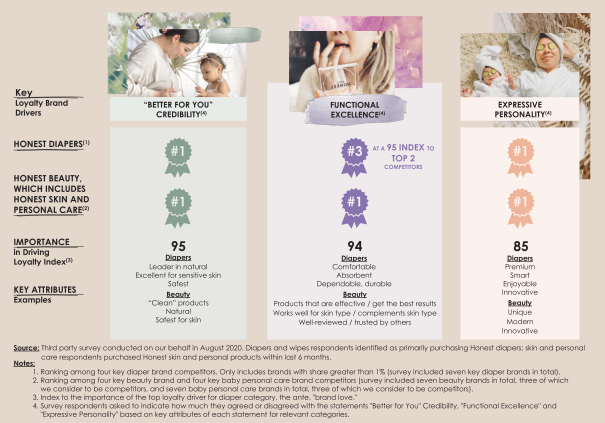

The top three $HNST categories are Diapers and Wipes, Skin and Personal Care, and Household and Wellness, which represented 63%, 26%, and 11% of its 2020 revenue.

$HNST IPO pricing range of $14 to $17 per share implies a market cap ranging from ~$1.4bn to $1.7bn (101M fully diluted shares outstanding).

Pre-IPO investors include IVP, Fidelity, Lightspeed, General Catalyst, ICONIQ, and Dragoneer.

Financials

$HNST revenues increased 27.6% from ~$236M to ~$301M in 2020, with Gross Margins in the 35% range.

$HNST reported positive EBITDA of ~$11mn during 2020 at 4% operating margin.

Competition

$HNST faces competition vs. large retailers and well-established brands such as $AMZN (Amazon), $COST (Costco) and $PG (Procter and Gamble) Pampers and $KMB (Kimberly Clark) Huggies.

Valuation

$HNST could generate revenues ranging from $350M to $375M (2021) and $425M to $450M (2022), implying 17% YoY growth, with gross margin and EBITDA margin approaching ~39% and ~8%, respectively, in 2022.

$HNST valuation implies 3.0x to 3.5x on 22E revenues and 7.5x to 9.0x 22E Gross Profit.

Recommendation

I dont think this company will soar on IPO, but I may be wrong. I do think there is a segment of their consumers who love them and they might buy the stock, but I believe there are better opportunities in other places to generate better returns.